Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Schedule of Review ProgramDokument3 SeitenSchedule of Review ProgramErma CaseñasNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- TB, JE, Etc Sunrise Dec 2021Dokument11 SeitenTB, JE, Etc Sunrise Dec 2021Erma CaseñasNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Sample ProductsDokument3 SeitenSample ProductsErma CaseñasNoch keine Bewertungen

- Unit I, Strategic Leadership Management Course Learning Outcomes For Unit IDokument7 SeitenUnit I, Strategic Leadership Management Course Learning Outcomes For Unit IErma CaseñasNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Student Grades FormatDokument1 SeiteStudent Grades FormatErma CaseñasNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- DTR DarDokument2 SeitenDTR DarErma CaseñasNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Duplicate Technical Problems: Mcgraw-Hill EducationDokument3 SeitenDuplicate Technical Problems: Mcgraw-Hill EducationErma CaseñasNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Annex C Boa Application Accounting Teacher 1Dokument2 SeitenAnnex C Boa Application Accounting Teacher 1Erma CaseñasNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Framework and Research Design PDFDokument55 SeitenFramework and Research Design PDFErma CaseñasNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- 2nd Quiz Midterm Acctg12Dokument3 Seiten2nd Quiz Midterm Acctg12Erma Caseñas50% (2)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Envelop CoverDokument1 SeiteEnvelop CoverErma CaseñasNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- FMI10e IM ch01Dokument10 SeitenFMI10e IM ch01Erma CaseñasNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- CH 1 Quiz Fin 11Dokument2 SeitenCH 1 Quiz Fin 11Erma CaseñasNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- MAS Preweek QuizzerDokument36 SeitenMAS Preweek QuizzerErma CaseñasNoch keine Bewertungen

- Ramon Magsaysay Memorial Colleges General Santos City Table of Specification Prelim Examination - 1 Semester 2016-2017Dokument1 SeiteRamon Magsaysay Memorial Colleges General Santos City Table of Specification Prelim Examination - 1 Semester 2016-2017Erma CaseñasNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Mejos BoardingpassDokument1 SeiteMejos BoardingpassErma CaseñasNoch keine Bewertungen

- ScratchDokument3 SeitenScratchErma CaseñasNoch keine Bewertungen

- GovtDokument1 SeiteGovtErma CaseñasNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Coa WPDokument63 SeitenCoa WPErma CaseñasNoch keine Bewertungen

- Post TestDokument1 SeitePost TestErma CaseñasNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Acctg 21 Remedial Class (July 23, 2016) Attendance SheetDokument4 SeitenAcctg 21 Remedial Class (July 23, 2016) Attendance SheetErma CaseñasNoch keine Bewertungen

- Date Allotment Received Obligation Incu BalanceDokument1 SeiteDate Allotment Received Obligation Incu BalanceErma CaseñasNoch keine Bewertungen

- Journalizing and PostingDokument6 SeitenJournalizing and PostingErma CaseñasNoch keine Bewertungen

- Mis207 ShostaDokument29 SeitenMis207 ShostaRafid ChyNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

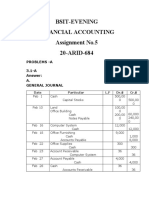

- Assignment No.5 AccountingDokument6 SeitenAssignment No.5 Accountingibrar ghaniNoch keine Bewertungen

- New AFU 07407 CF Slides 2022Dokument73 SeitenNew AFU 07407 CF Slides 2022janeth pallangyoNoch keine Bewertungen

- CXC 20171003Dokument15 SeitenCXC 20171003Angel Lawson100% (1)

- Private Equity and Fund RaisingDokument4 SeitenPrivate Equity and Fund RaisingKedar ParabNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Voltas 1Dokument85 SeitenVoltas 1Kuldeep Batra100% (1)

- Bhel Ratio AnalysisDokument5 SeitenBhel Ratio AnalysisPuja AryaNoch keine Bewertungen

- Nobles Acctg10 PPT 01Dokument61 SeitenNobles Acctg10 PPT 01Tayar ElieNoch keine Bewertungen

- Maybank Annual Report 2020 - Financial Statements (English)Dokument269 SeitenMaybank Annual Report 2020 - Financial Statements (English)YikHau NgNoch keine Bewertungen

- Introduction To PartnershipDokument21 SeitenIntroduction To PartnershipRejean Dela CruzNoch keine Bewertungen

- Blaine Kitchenware CalculationDokument11 SeitenBlaine Kitchenware CalculationAjeeth71% (7)

- Deloitte Valuations WorkshopDokument45 SeitenDeloitte Valuations Workshopdextro590100% (2)

- Cotton YarnDokument29 SeitenCotton YarnThomas MNoch keine Bewertungen

- India Post Conference Notes Day 1 Feb 12 EDELDokument104 SeitenIndia Post Conference Notes Day 1 Feb 12 EDELjayantsharma04Noch keine Bewertungen

- Balance Sheet & P&LDokument66 SeitenBalance Sheet & P&LAnish GhoshNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Financial Forecasting LastDokument40 SeitenFinancial Forecasting LastronnelNoch keine Bewertungen

- Solution Far410 Jun 2019Dokument9 SeitenSolution Far410 Jun 2019Nabilah NorddinNoch keine Bewertungen

- FX Blue Personal Trade Copier PDFDokument35 SeitenFX Blue Personal Trade Copier PDFKhairul Azizan Cucunaga0% (1)

- Peachtree GuideDokument36 SeitenPeachtree GuideGUDATA ABARANoch keine Bewertungen

- X Accounting 2Dokument419 SeitenX Accounting 2Amaury Guillermo Baez100% (2)

- Module 1, Part I - AmalgamationDokument14 SeitenModule 1, Part I - AmalgamationAbdullahNoch keine Bewertungen

- Financial Ratios TableDokument2 SeitenFinancial Ratios TableWiSeVirGoNoch keine Bewertungen

- Chapter 003 Financial Analysis: True / False QuestionsDokument54 SeitenChapter 003 Financial Analysis: True / False QuestionsWinnie GiveraNoch keine Bewertungen

- Case 3Dokument3 SeitenCase 3Alison WangNoch keine Bewertungen

- Accounting For Investments in AssociatesDokument90 SeitenAccounting For Investments in AssociatesJay-L TanNoch keine Bewertungen

- 18 007004 PDFDokument206 Seiten18 007004 PDFBrenda HerringNoch keine Bewertungen

- Long-Term Financial Planning and GrowthDokument30 SeitenLong-Term Financial Planning and GrowthSpatiha PathmanabanNoch keine Bewertungen

- Partnership Liquidation: Answers To Questions 1Dokument28 SeitenPartnership Liquidation: Answers To Questions 1El Carl Sontellinosa0% (1)

- Apollo Tyres Final)Dokument65 SeitenApollo Tyres Final)Mitisha GaurNoch keine Bewertungen

- Proforma Entries:: NPO (Nonprofit Organization)Dokument3 SeitenProforma Entries:: NPO (Nonprofit Organization)Marie GarpiaNoch keine Bewertungen

- Getting to Yes: How to Negotiate Agreement Without Giving InVon EverandGetting to Yes: How to Negotiate Agreement Without Giving InBewertung: 4 von 5 Sternen4/5 (652)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Von EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Bewertung: 4.5 von 5 Sternen4.5/5 (14)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsVon EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsBewertung: 5 von 5 Sternen5/5 (1)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Von EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Bewertung: 4.5 von 5 Sternen4.5/5 (14)