Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Togaf 9 1 Cheat Sheet v0 2Dokument13 SeitenTogaf 9 1 Cheat Sheet v0 2Arghya Mukherjee67% (3)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Business Blueprint TemplateDokument36 SeitenBusiness Blueprint TemplateUmesh SambareNoch keine Bewertungen

- Digital TransformationDokument26 SeitenDigital TransformationArghya Mukherjee100% (1)

- Fit-Up & Welding Visual Inspection ReportDokument11 SeitenFit-Up & Welding Visual Inspection ReportRachel Flores71% (7)

- Certificate: Ebm-Papst Mulfingen GMBH & Co. KGDokument5 SeitenCertificate: Ebm-Papst Mulfingen GMBH & Co. KGDANNYNoch keine Bewertungen

- E-Readiness QuestionnaireDokument6 SeitenE-Readiness QuestionnaireArghya MukherjeeNoch keine Bewertungen

- Employment Application: (Newgen Software Technologies LTD, D-162 Okhla Phase I, New Delhi - 110020) PersonalDokument5 SeitenEmployment Application: (Newgen Software Technologies LTD, D-162 Okhla Phase I, New Delhi - 110020) PersonalArghya MukherjeeNoch keine Bewertungen

- SAP For Managers: An Overview: Friday, February 27, 2015 1Dokument58 SeitenSAP For Managers: An Overview: Friday, February 27, 2015 1Arghya MukherjeeNoch keine Bewertungen

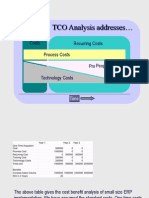

- TCO Analysis Addresses : One-Time Acquisition Costs Process CostsDokument3 SeitenTCO Analysis Addresses : One-Time Acquisition Costs Process CostsArghya MukherjeeNoch keine Bewertungen

- Case Study SevenDokument3 SeitenCase Study SevenArghya MukherjeeNoch keine Bewertungen

- Quality Management - QMTG14-4: Session 08 Inspection (Continued) + VSM (Continued)Dokument8 SeitenQuality Management - QMTG14-4: Session 08 Inspection (Continued) + VSM (Continued)Arghya MukherjeeNoch keine Bewertungen

- Chapter-8 Rationalization of SKU: Certificate in Strategic Retail ManagementDokument12 SeitenChapter-8 Rationalization of SKU: Certificate in Strategic Retail ManagementArghya MukherjeeNoch keine Bewertungen

- Chapter-6 Customer Centric Assortment Planning: Certificate in Strategic Retail ManagementDokument15 SeitenChapter-6 Customer Centric Assortment Planning: Certificate in Strategic Retail ManagementArghya MukherjeeNoch keine Bewertungen

- United Nations Literacy Decade: Effective PracticeDokument3 SeitenUnited Nations Literacy Decade: Effective PracticeArghya MukherjeeNoch keine Bewertungen

- Village Report - SEEDSDokument8 SeitenVillage Report - SEEDSArghya MukherjeeNoch keine Bewertungen

- DIORODEIL PRINTING COMPANY EditedDokument25 SeitenDIORODEIL PRINTING COMPANY EditedJustine Milante's PalasNoch keine Bewertungen

- Delegating Full Responsibility of The Product Project Management To ChassiscoDokument2 SeitenDelegating Full Responsibility of The Product Project Management To Chassiscoseff ongcaNoch keine Bewertungen

- PPC Unit 1Dokument10 SeitenPPC Unit 1saiNoch keine Bewertungen

- Business Model CanvasDokument2 SeitenBusiness Model CanvasKorir BrianNoch keine Bewertungen

- New Minor Project Report Haldiram'sDokument136 SeitenNew Minor Project Report Haldiram'smayank yadavNoch keine Bewertungen

- Oracle® Receivables: Implementation Guide Release 12.2Dokument346 SeitenOracle® Receivables: Implementation Guide Release 12.2Irina BolbasNoch keine Bewertungen

- Walastic: "Paper Packaging Using Banana Peel and Egg Shells"Dokument5 SeitenWalastic: "Paper Packaging Using Banana Peel and Egg Shells"Charles ManggaNoch keine Bewertungen

- Lux Vs Godrej No.1 (By Ayush Patel)Dokument30 SeitenLux Vs Godrej No.1 (By Ayush Patel)Ayush PatelNoch keine Bewertungen

- Iim BDokument2 SeitenIim BDhruv JainNoch keine Bewertungen

- ITSM Training Module FinalDokument45 SeitenITSM Training Module FinalBushra AlbalushiaNoch keine Bewertungen

- Rekap Finger Bulan Juni 2019Dokument6 SeitenRekap Finger Bulan Juni 2019Tahir TayoNoch keine Bewertungen

- Ex Squeeze MeDokument16 SeitenEx Squeeze MeFreeNet CodesNoch keine Bewertungen

- #08b Implementation of The Continuous Auditing System in The ERP Based EnvirontmentDokument36 Seiten#08b Implementation of The Continuous Auditing System in The ERP Based EnvirontmentnicophranceNoch keine Bewertungen

- Logistics ConceptsDokument24 SeitenLogistics ConceptsAbhishek NayakNoch keine Bewertungen

- Growth Strategies in BusinessDokument3 SeitenGrowth Strategies in BusinessSubrata BakshiNoch keine Bewertungen

- Manufacturing Event GuidelinesDokument3 SeitenManufacturing Event GuidelinesTinu MawaleNoch keine Bewertungen

- WAM PresentationDokument10 SeitenWAM PresentationAlicia BakerNoch keine Bewertungen

- Bigbazaar Case AnalysisDokument30 SeitenBigbazaar Case AnalysisPushpa Prakash100% (1)

- Eliminating Defects Through Equipment ReliabilityDokument6 SeitenEliminating Defects Through Equipment ReliabilityAriefNoch keine Bewertungen

- Sap 5Dokument6 SeitenSap 5isi londonNoch keine Bewertungen

- HR Champions Prex MaterialsDokument59 SeitenHR Champions Prex MaterialsIshakAnugrahNoch keine Bewertungen

- Cambridge IGCSE (9-1) : 0986/21 Business StudiesDokument4 SeitenCambridge IGCSE (9-1) : 0986/21 Business StudiesOmar BilalNoch keine Bewertungen

- Information Gathering Techniques-Chapter 07Dokument25 SeitenInformation Gathering Techniques-Chapter 07api-375996983% (6)

- Case Study IKEADokument9 SeitenCase Study IKEAVenkatkrishna Pichara100% (1)

- Project Report On Railway Reservation SystemDokument45 SeitenProject Report On Railway Reservation SystemChetan RajuNoch keine Bewertungen

- ERP Implementation4Dokument43 SeitenERP Implementation4Senthil KumarNoch keine Bewertungen

- Dokumen EksporDokument4 SeitenDokumen EksporDicky AditiyaNoch keine Bewertungen