Das könnte Ihnen auch gefallen

- L-M349 (L1b1a) Kenézy Ancestral JourneyDokument20 SeitenL-M349 (L1b1a) Kenézy Ancestral JourneyGábor Balogh100% (2)

- Learning Module 4 - BARTENDINGDokument34 SeitenLearning Module 4 - BARTENDINGivy mae flores67% (3)

- Executive Summary RUPTL PLN 2019-2028Dokument12 SeitenExecutive Summary RUPTL PLN 2019-2028Dhama Setra50% (2)

- Fabby Tumiwa - Indonesia FiT Implementation and Improvement ChallengesDokument13 SeitenFabby Tumiwa - Indonesia FiT Implementation and Improvement ChallengesAsia Clean Energy ForumNoch keine Bewertungen

- 12동남아프로젝트심층조사보고서 7 PDFDokument343 Seiten12동남아프로젝트심층조사보고서 7 PDFRdy SimangunsongNoch keine Bewertungen

- China Huadian Corporation: PLTU Sumsel 8Dokument3 SeitenChina Huadian Corporation: PLTU Sumsel 8widyo saptotoNoch keine Bewertungen

- Struktur Organisasi-Jul 2016 A3 PDFDokument2 SeitenStruktur Organisasi-Jul 2016 A3 PDFFahmi ShalasNoch keine Bewertungen

- Mou Take OverDokument3 SeitenMou Take OverElwansyahRismanNoch keine Bewertungen

- Bismillah Interview Lancar - EnI Indonesia - Id.enDokument4 SeitenBismillah Interview Lancar - EnI Indonesia - Id.enAndre SyahputraNoch keine Bewertungen

- Delong Holdings Annual Report 2008Dokument92 SeitenDelong Holdings Annual Report 2008WeR1 Consultants Pte LtdNoch keine Bewertungen

- RFP For PMC JICA PDFDokument85 SeitenRFP For PMC JICA PDFTadaPoornaNoch keine Bewertungen

- The Design of High Efficiency Crossflow Hydro Turbines - A Review and Extension PDFDokument18 SeitenThe Design of High Efficiency Crossflow Hydro Turbines - A Review and Extension PDFDragomirescu AndreiNoch keine Bewertungen

- Makalah Assesment RONIANTODokument5 SeitenMakalah Assesment RONIANTOOperasi Banjarsari100% (1)

- Elwansyah Risman CVDokument16 SeitenElwansyah Risman CVElwansyahRismanNoch keine Bewertungen

- Appendix 7.indonesia Grid Code.27 Jan 09.HAPUA SWG2 SO TORDokument28 SeitenAppendix 7.indonesia Grid Code.27 Jan 09.HAPUA SWG2 SO TORrdwchyNoch keine Bewertungen

- The Indonesia National Clean Development Mechanism Strategy StudyDokument223 SeitenThe Indonesia National Clean Development Mechanism Strategy StudyGedeBudiSuprayogaNoch keine Bewertungen

- Aurelia Micko - USAID Indonesia Clean Energy Development ProgramsDokument18 SeitenAurelia Micko - USAID Indonesia Clean Energy Development ProgramsAsia Clean Energy ForumNoch keine Bewertungen

- Day 2 Solar 2 Developing The First Grid Connected Solar PV in Indonesia Abraham MoseDokument20 SeitenDay 2 Solar 2 Developing The First Grid Connected Solar PV in Indonesia Abraham MoseMuammar ZainuddinNoch keine Bewertungen

- 2012 PGN Annual ReportDokument538 Seiten2012 PGN Annual Reporterwin hpNoch keine Bewertungen

- INDONESIA INDUSTRIAL ESTATES DIRECTORY 2018-2019 (Westpoint) PDFDokument1 SeiteINDONESIA INDUSTRIAL ESTATES DIRECTORY 2018-2019 (Westpoint) PDFGinnyNoch keine Bewertungen

- Brief History Sarulla FieldDokument4 SeitenBrief History Sarulla FieldRidho AsrowiNoch keine Bewertungen

- Indonesia Power Plant ListDokument1 SeiteIndonesia Power Plant Listyulhendri.saputraNoch keine Bewertungen

- Oil and Gas in MyanmarDokument3 SeitenOil and Gas in MyanmarKunwadi ChantaraparnNoch keine Bewertungen

- Coal Investment Thailand enDokument12 SeitenCoal Investment Thailand enKhan Ahmed MuradNoch keine Bewertungen

- Universitas Pamulang Viktor Tangsel 186.2 KWP REC SMA Proposal v0.1Dokument29 SeitenUniversitas Pamulang Viktor Tangsel 186.2 KWP REC SMA Proposal v0.1Zakky Ghifari Arfiansyah100% (1)

- MUARA KARANG GBU (PT. PJB - Generation Business Unit)Dokument3 SeitenMUARA KARANG GBU (PT. PJB - Generation Business Unit)Revi NaldiNoch keine Bewertungen

- Coanda Intake BasicsDokument4 SeitenCoanda Intake BasicsClemente CurnisNoch keine Bewertungen

- Master Listing Jan 13 2018Dokument137 SeitenMaster Listing Jan 13 2018Deden ChandraNoch keine Bewertungen

- Experience List: Pt. Surya Besindo SaktiDokument6 SeitenExperience List: Pt. Surya Besindo Saktiagusnnn100% (1)

- Indonesia IPP ReportDokument41 SeitenIndonesia IPP ReportUranika L WireksoNoch keine Bewertungen

- Vol 141Dokument104 SeitenVol 141Rendi100% (1)

- Eu Gateway Market Study Green Energy Technologies Indonesia PDFDokument261 SeitenEu Gateway Market Study Green Energy Technologies Indonesia PDFkevin sunNoch keine Bewertungen

- Company Profile PT. Nikkatsu Electric WorksDokument17 SeitenCompany Profile PT. Nikkatsu Electric WorksDenny Ilyas Attamimi100% (1)

- INR - Ed-1 Feb 2020Dokument41 SeitenINR - Ed-1 Feb 2020Dirga DanielNoch keine Bewertungen

- Indonesia Oil and GasDokument18 SeitenIndonesia Oil and Gaswhusada100% (1)

- ATW Company ProfileDokument45 SeitenATW Company ProfileHony Fathur RohmanNoch keine Bewertungen

- PO Wartsila - 720001 - SignedDokument2 SeitenPO Wartsila - 720001 - SigneddithopramNoch keine Bewertungen

- Daftar BUMN - Kementerian BUMNDokument4 SeitenDaftar BUMN - Kementerian BUMNAnwar Saleh Al-Yasir Lubis100% (1)

- Renewable Energy in North SulawesiDokument10 SeitenRenewable Energy in North SulawesiSeptian AnggoroNoch keine Bewertungen

- Amberlite IRC120 NaDokument3 SeitenAmberlite IRC120 NaPT Deltapuro Indonesia100% (1)

- PT. Koneksindo Karya Mandiri Company Profile1Dokument24 SeitenPT. Koneksindo Karya Mandiri Company Profile1Fachry Setia AkbarNoch keine Bewertungen

- Format TableDokument405 SeitenFormat TablelebahlistrikNoch keine Bewertungen

- Samindo Resources Annual Report 2014 Company Profile Indonesia Investments MYOH PDFDokument183 SeitenSamindo Resources Annual Report 2014 Company Profile Indonesia Investments MYOH PDFSandykoNoch keine Bewertungen

- Alamat Kantor Pusat Migas IndonesiaDokument23 SeitenAlamat Kantor Pusat Migas IndonesiaKhalify Awaludin AsmawinataNoch keine Bewertungen

- Daftar Kit Jawa BaliDokument8 SeitenDaftar Kit Jawa BaliWidya Ananta Prabawa100% (1)

- Aconex - EHSDokument6 SeitenAconex - EHSOzi RezmiraNoch keine Bewertungen

- List Room PLN 3 - 4 Nov 2022-1-1Dokument7 SeitenList Room PLN 3 - 4 Nov 2022-1-1mohammad imronNoch keine Bewertungen

- The Banki Water TurbineDokument28 SeitenThe Banki Water Turbineamatos4716075% (4)

- New Presentation Jakarta Whell 2017-2Dokument33 SeitenNew Presentation Jakarta Whell 2017-2Wan Zainal Wan Zain0% (1)

- KatulampaDokument23 SeitenKatulampaIman N SoeriaatmadjaNoch keine Bewertungen

- Hear From Government and Top MinersDokument6 SeitenHear From Government and Top MinersRudy StyNoch keine Bewertungen

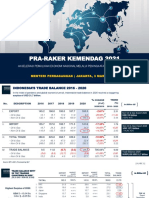

- Pra-Raker Kemendag 2021: Akselerasi Pemulihan Ekonomi Nasional Melalui Peningkatan Peran PerwadagDokument38 SeitenPra-Raker Kemendag 2021: Akselerasi Pemulihan Ekonomi Nasional Melalui Peningkatan Peran PerwadagDedy Lampe PRayaNoch keine Bewertungen

- Daihan Labtech PresentationDokument24 SeitenDaihan Labtech PresentationMuhammad Muzakky AL MaududyNoch keine Bewertungen

- Jakarta Greater Jakarta Industrial Market Update - Q3 2019 - V2 PDFDokument14 SeitenJakarta Greater Jakarta Industrial Market Update - Q3 2019 - V2 PDFEka Esti SusantiNoch keine Bewertungen

- Fire SupressionDokument127 SeitenFire SupressionJen AgabinNoch keine Bewertungen

- Solar PV Rooftoop Application at SPINDODokument23 SeitenSolar PV Rooftoop Application at SPINDOMuhammad Fathoni FikriNoch keine Bewertungen

- 28 Annual Report 2009Dokument421 Seiten28 Annual Report 2009Reza Fachrezy MachtoebNoch keine Bewertungen

- National Renewable Infrastructure Plan Stage 2Dokument46 SeitenNational Renewable Infrastructure Plan Stage 2GreenerLeith0% (1)

- Telephone List Rev Jul 2013 (Extension)Dokument3 SeitenTelephone List Rev Jul 2013 (Extension)fahrain2012Noch keine Bewertungen

- 2018 Forbes IndonesiaDokument4 Seiten2018 Forbes IndonesiaVELO Property OfficialNoch keine Bewertungen

- EGHPP Project Introduction For Business SummitDokument3 SeitenEGHPP Project Introduction For Business SummitUrtaBaasanjargalNoch keine Bewertungen

- Rendev WP3 D8 Bangla April09Dokument55 SeitenRendev WP3 D8 Bangla April09Saqib KhanNoch keine Bewertungen

- PoGo GymDef Cheat SheetDokument1 SeitePoGo GymDef Cheat SheetFerni Panchito VillaNoch keine Bewertungen

- Airplus CDF3 Technical SpecsDokument38 SeitenAirplus CDF3 Technical Specssadik FreelancerNoch keine Bewertungen

- Bearing Capacity of Closed and Open Ended Piles Installed in Loose Sand PDFDokument22 SeitenBearing Capacity of Closed and Open Ended Piles Installed in Loose Sand PDFAnonymous 8KOUFYqNoch keine Bewertungen

- 2017 - Behavioral Emergencies - Geriatric Psychiatric PatientDokument14 Seiten2017 - Behavioral Emergencies - Geriatric Psychiatric PatientAna María Arenas DávilaNoch keine Bewertungen

- Talking SwedishDokument32 SeitenTalking Swedishdiana jimenezNoch keine Bewertungen

- Enzyme Kinetics Principles and MethodsDokument268 SeitenEnzyme Kinetics Principles and MethodsCarlos Carinelli100% (4)

- 35.ravi Gupta Writs (CLE)Dokument22 Seiten35.ravi Gupta Writs (CLE)Ravi GuptaNoch keine Bewertungen

- QAS M001 SLPS Quality Assurance ManualDokument49 SeitenQAS M001 SLPS Quality Assurance ManualMHDNoch keine Bewertungen

- How To Read Research PaperDokument7 SeitenHow To Read Research Papertuigauund100% (1)

- Openstack Deployment Ops Guide PDFDokument197 SeitenOpenstack Deployment Ops Guide PDFBinank PatelNoch keine Bewertungen

- HCT Baniqued P.D.E. Paper1 Version3 FullpaperDokument8 SeitenHCT Baniqued P.D.E. Paper1 Version3 FullpaperJoshua HernandezNoch keine Bewertungen

- 1 SAP HCM Overview - IntroductionDokument32 Seiten1 SAP HCM Overview - IntroductionashwiniNoch keine Bewertungen

- Install NotesDokument6 SeitenInstall NotesSchweinsteiger NguyễnNoch keine Bewertungen

- LEASE CONTRACT Taytay Residentialhouse Kei Inagaki Nena TrusaDokument6 SeitenLEASE CONTRACT Taytay Residentialhouse Kei Inagaki Nena TrusaJaime GonzalesNoch keine Bewertungen

- 1.2 Introduction To PHP - PHP KeywordsDokument12 Seiten1.2 Introduction To PHP - PHP KeywordsOvie Nur FaizahNoch keine Bewertungen

- DSC User GuidelinesDokument64 SeitenDSC User Guidelineslinus200Noch keine Bewertungen

- Buyer Behavior ModelDokument1 SeiteBuyer Behavior ModelraihanulhasanNoch keine Bewertungen

- Sample Paper For Professional Ethics in Accounting and FinanceDokument6 SeitenSample Paper For Professional Ethics in Accounting and FinanceWinnieOngNoch keine Bewertungen

- Agmt - Spa Schedule HDokument20 SeitenAgmt - Spa Schedule Hapi-340431954Noch keine Bewertungen

- ReflectionDokument2 SeitenReflectionBảo HàNoch keine Bewertungen

- Fellowship 2nd Edition Book 2 - Inverse Fellowship (Playbooks)Dokument44 SeitenFellowship 2nd Edition Book 2 - Inverse Fellowship (Playbooks)AleNoch keine Bewertungen

- CodeDokument47 SeitenCodeNadia KhurshidNoch keine Bewertungen

- J2 P IntroductionDokument9 SeitenJ2 P IntroductionnitinvnjNoch keine Bewertungen

- Students List - All SectionsDokument8 SeitenStudents List - All SectionsChristian RiveraNoch keine Bewertungen

- Determining The Value of The Acceleration Due To Gravity: President Ramon Magsaysay State UniversityDokument12 SeitenDetermining The Value of The Acceleration Due To Gravity: President Ramon Magsaysay State UniversityKristian Anthony BautistaNoch keine Bewertungen

- Errors Affecting The Trial BalanceDokument3 SeitenErrors Affecting The Trial BalanceDarwin Lopez100% (1)

- Activity 9 Let's Check and Let's AnalyzeDokument3 SeitenActivity 9 Let's Check and Let's AnalyzeJean Tronco100% (5)

- Gurdan Saini: From Wikipedia, The Free EncyclopediaDokument6 SeitenGurdan Saini: From Wikipedia, The Free EncyclopediaRanjeet SinghNoch keine Bewertungen