Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- WSU Electrical Fundamentals Tutorial 2 2017 3Dokument3 SeitenWSU Electrical Fundamentals Tutorial 2 2017 3Alex WuNoch keine Bewertungen

- EF 20167 Tutorial - 1 QuestionsDokument2 SeitenEF 20167 Tutorial - 1 QuestionsAlex WuNoch keine Bewertungen

- ACTL3182 Tutorial Exercises 2018Dokument178 SeitenACTL3182 Tutorial Exercises 2018Alex WuNoch keine Bewertungen

- Gpe and Weight ProblemsDokument4 SeitenGpe and Weight ProblemsAlex WuNoch keine Bewertungen

- Lecture 1 2018Dokument38 SeitenLecture 1 2018Alex WuNoch keine Bewertungen

- Mass of SunDokument1 SeiteMass of SunAlex WuNoch keine Bewertungen

- ACTL3182 2018 Sem 2 Annotated Lecture NotesDokument120 SeitenACTL3182 2018 Sem 2 Annotated Lecture NotesAlex WuNoch keine Bewertungen

- EF 20167 Tutorial - 1 QuestionsDokument2 SeitenEF 20167 Tutorial - 1 QuestionsAlex WuNoch keine Bewertungen

- FINS3637 - 5537 Lecture One Sem1 - 2017 One Slide Per PageDokument57 SeitenFINS3637 - 5537 Lecture One Sem1 - 2017 One Slide Per PageAlex WuNoch keine Bewertungen

- Options and Derivatives Greek Letters MCQDokument6 SeitenOptions and Derivatives Greek Letters MCQKevin Molly KamrathNoch keine Bewertungen

- Completed Assignment 1 - Hedging Data-2018Dokument14 SeitenCompleted Assignment 1 - Hedging Data-2018Alex WuNoch keine Bewertungen

- Fins 3625 - Tutorial 1 HWDokument3 SeitenFins 3625 - Tutorial 1 HWAlex WuNoch keine Bewertungen

- Projectile MotionDokument10 SeitenProjectile MotionAlex WuNoch keine Bewertungen

- FINS 3616 Tutorial Questions-Week 4Dokument6 SeitenFINS 3616 Tutorial Questions-Week 4Alex WuNoch keine Bewertungen

- International Capital Market Equilibrium TutorialDokument2 SeitenInternational Capital Market Equilibrium TutorialAlex WuNoch keine Bewertungen

- FINS 3616 Tutorial Questions-Week 3Dokument5 SeitenFINS 3616 Tutorial Questions-Week 3Alex WuNoch keine Bewertungen

- FINS 3616 Tutorial Questions-Week 2Dokument7 SeitenFINS 3616 Tutorial Questions-Week 2Alex WuNoch keine Bewertungen

- FINS 3616 Tutorial Questions-Week 2Dokument7 SeitenFINS 3616 Tutorial Questions-Week 2Alex WuNoch keine Bewertungen

- FINS 3616 Tutorial Questions-Week 2Dokument7 SeitenFINS 3616 Tutorial Questions-Week 2Alex WuNoch keine Bewertungen

- FINS1612 Tutorial ProgramDokument1 SeiteFINS1612 Tutorial ProgramAlex WuNoch keine Bewertungen

- FINS 3616 Tutorial Questions-Week 1Dokument5 SeitenFINS 3616 Tutorial Questions-Week 1Alex WuNoch keine Bewertungen

- HSC Chemistry - Core Module 2 - The Acidic Environment - Section 2Dokument22 SeitenHSC Chemistry - Core Module 2 - The Acidic Environment - Section 2Alex WuNoch keine Bewertungen

- Global Business TodayDokument23 SeitenGlobal Business TodaysukandeNoch keine Bewertungen

- ACTL2111 Module - 1Dokument101 SeitenACTL2111 Module - 1Alex WuNoch keine Bewertungen

- Topic2 Valuation 6PGDokument14 SeitenTopic2 Valuation 6PGAlex WuNoch keine Bewertungen

- 2017 ACTL2131 ExercisesDokument171 Seiten2017 ACTL2131 ExercisesAlex WuNoch keine Bewertungen

- The Acidic Environment - Section 1Dokument4 SeitenThe Acidic Environment - Section 1Manez WaranNoch keine Bewertungen

- Formulae and Table 2nd EdDokument197 SeitenFormulae and Table 2nd EdAlex WuNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Ar 2010Dokument115 SeitenAr 2010pipiNoch keine Bewertungen

- Causes and Effects of Demutualization of Financial ExchangesDokument49 SeitenCauses and Effects of Demutualization of Financial Exchangesfahd_faux9282Noch keine Bewertungen

- SRC Supplement 1-Registered Debt CompaniesDokument2 SeitenSRC Supplement 1-Registered Debt CompaniesMae Richelle Dizon DacaraNoch keine Bewertungen

- Sakthi Fianance Project ReportDokument61 SeitenSakthi Fianance Project ReportraveenkumarNoch keine Bewertungen

- Keown 23 RP3Dokument24 SeitenKeown 23 RP3ausantNoch keine Bewertungen

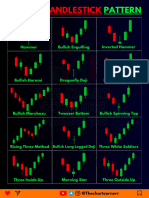

- Chart Pattern Cheat Sheet-1Dokument18 SeitenChart Pattern Cheat Sheet-1YASHANK VISHWAKARMANoch keine Bewertungen

- Ku vs. RCBC SecuritiesDokument16 SeitenKu vs. RCBC SecuritiesEmir Mendoza0% (1)

- English For BusinessDokument40 SeitenEnglish For BusinessSyavina Haidar AlatasNoch keine Bewertungen

- RBL Bank Ltd. BUYDokument7 SeitenRBL Bank Ltd. BUYpajadhavNoch keine Bewertungen

- UnionBank 2018 Annual Report Highlights Key DevelopmentsDokument295 SeitenUnionBank 2018 Annual Report Highlights Key Developmentsnancy delos santosNoch keine Bewertungen

- Dissertation For II Year M .Com StudentsDokument12 SeitenDissertation For II Year M .Com Studentsnischal mathewNoch keine Bewertungen

- ForexCOMBOSystem Guide v5.0 (4in1) NFDokument14 SeitenForexCOMBOSystem Guide v5.0 (4in1) NFMiguel Angel PerezNoch keine Bewertungen

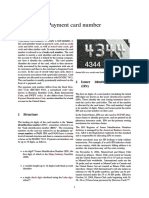

- Payment Card Number Structure and IdentificationDokument4 SeitenPayment Card Number Structure and IdentificationlunwenNoch keine Bewertungen

- Basel Norms in Banking SectorsDokument36 SeitenBasel Norms in Banking SectorsSaikat ChatterjeeNoch keine Bewertungen

- MARKETSTRATEGYDokument6 SeitenMARKETSTRATEGYvikalp123123Noch keine Bewertungen

- Earnest Money, Security Deosit and Retention MoneyDokument8 SeitenEarnest Money, Security Deosit and Retention MoneyRushabh Ajmera100% (3)

- Assignment Risk and ReturnDokument3 SeitenAssignment Risk and ReturnCheong Yu ShuangNoch keine Bewertungen

- ACC501 Solved MCQsDokument6 SeitenACC501 Solved MCQsMuhammad aqeeb qureshiNoch keine Bewertungen

- Benefits of Adverse PossessionDokument3 SeitenBenefits of Adverse PossessionBob Hurt100% (3)

- 2015 Suggested AnswersDokument109 Seiten2015 Suggested Answersnaomi100% (1)

- BU8201 Business Finance Course OverviewDokument2 SeitenBU8201 Business Finance Course OverviewJun WeiNoch keine Bewertungen

- eDokument13 SeitenepeyockNoch keine Bewertungen

- A Study On Working Capital Management in Strides Shasun Limited at CuddaloreDokument75 SeitenA Study On Working Capital Management in Strides Shasun Limited at Cuddaloreashok kumar100% (3)

- Group structure analysisDokument3 SeitenGroup structure analysisKamaruzzaman MohdNoch keine Bewertungen

- Is the contract of pledge binding on third partiesDokument1 SeiteIs the contract of pledge binding on third partiesTeff QuibodNoch keine Bewertungen

- Excel TrainingDokument28 SeitenExcel TrainingNiraj Arun ThakkarNoch keine Bewertungen

- QUANTITATIVE STRATEGIES RESEARCH NOTES GADGETSDokument43 SeitenQUANTITATIVE STRATEGIES RESEARCH NOTES GADGETSHongchul HaNoch keine Bewertungen

- Dep KeyDokument2 SeitenDep Keyanilkg53Noch keine Bewertungen

- Regulatory On Derivatives (1) (From Shodhganga)Dokument70 SeitenRegulatory On Derivatives (1) (From Shodhganga)sharathNoch keine Bewertungen