Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Deloitte Annual Review of Football Finance (2014)Dokument10 SeitenDeloitte Annual Review of Football Finance (2014)Tifoso BilanciatoNoch keine Bewertungen

- Real Estate Exam Study GuideDokument53 SeitenReal Estate Exam Study Guideitzmsmichelle100% (3)

- COA Construction General ContractorDokument16 SeitenCOA Construction General ContractorLarryMatiasNoch keine Bewertungen

- Literature Review v02Dokument3 SeitenLiterature Review v02Hasan Md ErshadNoch keine Bewertungen

- Delta Beverage - CaseDokument16 SeitenDelta Beverage - CaseHasan Md ErshadNoch keine Bewertungen

- Internship Report PDFDokument50 SeitenInternship Report PDFHasan Md ErshadNoch keine Bewertungen

- Peirson BusinessDokument45 SeitenPeirson BusinessHasan Md ErshadNoch keine Bewertungen

- Empirical Finance Case 1Dokument1 SeiteEmpirical Finance Case 1Hasan Md ErshadNoch keine Bewertungen

- Vii. Securities Transaction Taxes: Should The Legislature Act As Robin Hood?Dokument11 SeitenVii. Securities Transaction Taxes: Should The Legislature Act As Robin Hood?Hasan Md ErshadNoch keine Bewertungen

- Assignment 1 Merrill Case (Updated)Dokument3 SeitenAssignment 1 Merrill Case (Updated)Hasan Md ErshadNoch keine Bewertungen

- PTC and Phillip Morris Financial AnalysisDokument15 SeitenPTC and Phillip Morris Financial AnalysisYasir Saeed100% (1)

- How Open Banking Can Support SME FinanceDokument13 SeitenHow Open Banking Can Support SME FinanceADBI EventsNoch keine Bewertungen

- Report - Vidarbha FarmersDokument15 SeitenReport - Vidarbha Farmersdims16_2006100% (1)

- FM-cash FlowDokument28 SeitenFM-cash FlowParamjit Sharma100% (5)

- Chicago Taxi Medallion ForeclosuresDokument1 SeiteChicago Taxi Medallion ForeclosuresUSA TODAYNoch keine Bewertungen

- 11Dokument16 Seiten11Dennis AleaNoch keine Bewertungen

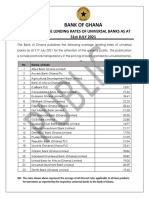

- Average Lending Rates As at July 2021Dokument1 SeiteAverage Lending Rates As at July 2021Fuaad DodooNoch keine Bewertungen

- Curriculum Vitae Personal DetailsDokument4 SeitenCurriculum Vitae Personal DetailsAndrew NkhuwaNoch keine Bewertungen

- Hindu Undivided FamilyDokument4 SeitenHindu Undivided FamilyNandkumar Chinai0% (1)

- BIR Ruling on Tax Implications of Bank's Decrease in Capital Stock and Transfer of Assets to Parent CompanyDokument11 SeitenBIR Ruling on Tax Implications of Bank's Decrease in Capital Stock and Transfer of Assets to Parent CompanyRB BalanayNoch keine Bewertungen

- 1 Tolentino Vs Gonzales, 50 Phil 558Dokument9 Seiten1 Tolentino Vs Gonzales, 50 Phil 558Perry YapNoch keine Bewertungen

- MODULE 5 Interest RateDokument4 SeitenMODULE 5 Interest RateDonna Mae FernandezNoch keine Bewertungen

- Landlord Tenant Handbok Montgomery County MDDokument80 SeitenLandlord Tenant Handbok Montgomery County MDkitty_chan_19Noch keine Bewertungen

- WWW Manilatimes NetDokument3 SeitenWWW Manilatimes NetEarl Mercado CalingacionNoch keine Bewertungen

- DPC PRJCT 9th SemDokument8 SeitenDPC PRJCT 9th SemStuti BaradiaNoch keine Bewertungen

- Model Paper: D (KK D (KK D (KK D (KK D (KK - Ys (KK'KKL Ys (KK'KKL Ys (KK'KKL Ys (KK'KKL Ys (KK'KKLDokument39 SeitenModel Paper: D (KK D (KK D (KK D (KK D (KK - Ys (KK'KKL Ys (KK'KKL Ys (KK'KKL Ys (KK'KKL Ys (KK'KKLTezendra SinghNoch keine Bewertungen

- Contracts Course Outline Revised BQS 112Dokument7 SeitenContracts Course Outline Revised BQS 112MichaelKipronoNoch keine Bewertungen

- Exchange Rates ExercisesDokument8 SeitenExchange Rates Exercisesarupkalita_aecNoch keine Bewertungen

- Causes, Impact and Regional Distribution of Black Money in IndiaDokument6 SeitenCauses, Impact and Regional Distribution of Black Money in IndiaKinnari Sanganee Bhatt100% (1)

- Writing Inequalities From Word ProblemsDokument28 SeitenWriting Inequalities From Word Problemsapi-379755793Noch keine Bewertungen

- Analysis of Altman "ZDokument3 SeitenAnalysis of Altman "ZShruthi JumkaNoch keine Bewertungen

- 10693Dokument6 Seiten10693Joanne FerrerNoch keine Bewertungen

- Kumarmangalam Report On Corporate GovernanceDokument22 SeitenKumarmangalam Report On Corporate Governancepritikopade020% (1)

- Schedule C Instructions 2012Dokument13 SeitenSchedule C Instructions 2012Dunk7Noch keine Bewertungen

- HDFC PDFDokument43 SeitenHDFC PDFAbhijit SahooNoch keine Bewertungen

- Why Tally is best for basic inventory managementDokument10 SeitenWhy Tally is best for basic inventory managementAyush BishtNoch keine Bewertungen

- Motta Design Report-B-Final 1Dokument123 SeitenMotta Design Report-B-Final 1kedir100% (4)