Das könnte Ihnen auch gefallen

- Butler Lumber Company: Following Questions Are Answered in This Case Study SolutionDokument3 SeitenButler Lumber Company: Following Questions Are Answered in This Case Study SolutionTalha SiddiquiNoch keine Bewertungen

- Butler Lumber Final First DraftDokument12 SeitenButler Lumber Final First DraftAdit Swarup100% (2)

- Padgett Paper Products Case StudyDokument7 SeitenPadgett Paper Products Case StudyDavey FranciscoNoch keine Bewertungen

- ExamView - Homework CH 4Dokument9 SeitenExamView - Homework CH 4Brooke LevertonNoch keine Bewertungen

- Chapter 6Dokument24 SeitenChapter 6sdfklmjsdlklskfjd100% (2)

- 1) Answer: Interest Expense 0 Solution:: Financial Statement AnalysisDokument9 Seiten1) Answer: Interest Expense 0 Solution:: Financial Statement AnalysisGA ZinNoch keine Bewertungen

- DupontDokument4 SeitenDupontChanathip_Kupr_4289Noch keine Bewertungen

- ch.10 TB 331Dokument12 Seitench.10 TB 331nickvanderv100% (1)

- 245574345-ISMChap014 NewDokument68 Seiten245574345-ISMChap014 NewStephenMcDanielNoch keine Bewertungen

- Security Market Indices ExplainedDokument7 SeitenSecurity Market Indices ExplainedborritaNoch keine Bewertungen

- Hilton 2222Dokument70 SeitenHilton 2222Dianne Garcia RicamaraNoch keine Bewertungen

- 1.2 AudDokument1 Seite1.2 AudLu LacNoch keine Bewertungen

- FIN 500 TEST # 1 (CHAPTER 2-3-4) : Multiple ChoiceDokument11 SeitenFIN 500 TEST # 1 (CHAPTER 2-3-4) : Multiple ChoicemarkomatematikaNoch keine Bewertungen

- Group 4 Home DepotDokument2 SeitenGroup 4 Home DepotnikhilNoch keine Bewertungen

- Titanium Dioxide ExhibitsDokument7 SeitenTitanium Dioxide Exhibitssanjayhk7Noch keine Bewertungen

- Home Depot PresentationfinalDokument42 SeitenHome Depot Presentationfinalpankajkumar631Noch keine Bewertungen

- CarProof Audit Risks MemoDokument1 SeiteCarProof Audit Risks MemojwagambillNoch keine Bewertungen

- Quiz#5 - Wacc-Levrage Student 25q-25ptsDokument4 SeitenQuiz#5 - Wacc-Levrage Student 25q-25ptsVinícius AlvesNoch keine Bewertungen

- Finals Exercise 2 - WC Management InventoryDokument3 SeitenFinals Exercise 2 - WC Management Inventorywin win0% (1)

- Fin 4 WC FinancingDokument2 SeitenFin 4 WC FinancingHumphrey OdchigueNoch keine Bewertungen

- 1Dokument2 Seiten1blankNoch keine Bewertungen

- Industrial Restructuring and Enterpreneurship - H. J. HEINZ Company CaseDokument5 SeitenIndustrial Restructuring and Enterpreneurship - H. J. HEINZ Company CaseFagbola Oluwatobi OmolajaNoch keine Bewertungen

- The Dilemma at Day 21Dokument4 SeitenThe Dilemma at Day 21Christian AndreNoch keine Bewertungen

- Coma Quiz 6 KeyDokument20 SeitenComa Quiz 6 KeyMD TARIQUE NOORNoch keine Bewertungen

- Financial Management 2 - BirminghamDokument21 SeitenFinancial Management 2 - BirminghamsimuragejayanNoch keine Bewertungen

- Clarkson Lumbar CompanyDokument41 SeitenClarkson Lumbar CompanyTheOxyCleanGuyNoch keine Bewertungen

- CHAPTER 11 Without AnswerDokument3 SeitenCHAPTER 11 Without Answerlenaka0% (1)

- CH 07Dokument72 SeitenCH 07Ivhy Cruz Estrella100% (1)

- Chap 010Dokument9 SeitenChap 010siddharth.savlodhiaNoch keine Bewertungen

- Module 5 - Assessment ActivitiesDokument4 SeitenModule 5 - Assessment Activitiesaj dumpNoch keine Bewertungen

- Assignment No. 1Dokument3 SeitenAssignment No. 1ENoch keine Bewertungen

- Can One Size Fit All?Dokument21 SeitenCan One Size Fit All?Abhimanyu ChoudharyNoch keine Bewertungen

- Calculate Equilibrium Stock Price with Declining EarningsDokument12 SeitenCalculate Equilibrium Stock Price with Declining EarningsJenelle ReyesNoch keine Bewertungen

- Acc423 Final Exam 100+ Questions Included 2 ExamsDokument102 SeitenAcc423 Final Exam 100+ Questions Included 2 ExamsMaria Aguilar0% (1)

- Finance Chapter 15Dokument34 SeitenFinance Chapter 15courtdubs100% (1)

- NFJPIA - Mockboard 2011 - MAS PDFDokument7 SeitenNFJPIA - Mockboard 2011 - MAS PDFDanica PelenioNoch keine Bewertungen

- E. Patrick Assignment 4.1Dokument3 SeitenE. Patrick Assignment 4.1Alex100% (2)

- Installment Sales Accounting GuideDokument6 SeitenInstallment Sales Accounting GuideChloe OberlinNoch keine Bewertungen

- ACCO 3026 Final ExamDokument11 SeitenACCO 3026 Final ExamClarisseNoch keine Bewertungen

- 10 Responsibility Accounting Live DiscussionDokument4 Seiten10 Responsibility Accounting Live DiscussionLee SuarezNoch keine Bewertungen

- Butler CaseDokument12 SeitenButler CaseJosh BenjaminNoch keine Bewertungen

- MBA Exam 1 Spring 2009Dokument12 SeitenMBA Exam 1 Spring 2009Kamal AssafNoch keine Bewertungen

- Colegio de La Purisima Concepcion: School of The Archdiocese of Capiz Roxas CityDokument5 SeitenColegio de La Purisima Concepcion: School of The Archdiocese of Capiz Roxas CityJhomel Domingo GalvezNoch keine Bewertungen

- Dividend Policy 1Dokument9 SeitenDividend Policy 1Almira BesoniaNoch keine Bewertungen

- Cost of CapitalDokument10 SeitenCost of CapitalCharmaine ChuNoch keine Bewertungen

- Quiz-01-10-16-20-Class Finacc7 DDokument8 SeitenQuiz-01-10-16-20-Class Finacc7 DKhevin AlvaradoNoch keine Bewertungen

- Hansen Aise Im Ch16Dokument55 SeitenHansen Aise Im Ch16Daniel NababanNoch keine Bewertungen

- 8 Responsibility AccountingDokument8 Seiten8 Responsibility AccountingXyril MañagoNoch keine Bewertungen

- (Fingerprints Group) 2011 CIMA Global Business Challenge ReportDokument23 Seiten(Fingerprints Group) 2011 CIMA Global Business Challenge Reportcrazyfrog1991Noch keine Bewertungen

- Acctg 162 – Material 019 (SHE) True or False & ProblemsDokument4 SeitenAcctg 162 – Material 019 (SHE) True or False & ProblemsAngelli LamiqueNoch keine Bewertungen

- Mayes 8e CH11 Problem SetDokument6 SeitenMayes 8e CH11 Problem SetMd Rasel Uddin ACMA0% (2)

- Current Liabilities ManagementDokument7 SeitenCurrent Liabilities ManagementJack Herer100% (1)

- CMA P3 Finance 4Dokument23 SeitenCMA P3 Finance 4Hamza Lutaf UllahNoch keine Bewertungen

- Butler Lumber CaseDokument4 SeitenButler Lumber CaseLovin SeeNoch keine Bewertungen

- Butler Lumber CompanyDokument4 SeitenButler Lumber Companynickiminaj221421Noch keine Bewertungen

- Butler Lumber Company Financial Analysis Accepting Supplier DiscountDokument4 SeitenButler Lumber Company Financial Analysis Accepting Supplier DiscountPeyman VahdatiNoch keine Bewertungen

- Butler Lumber Company Funding AnalysisDokument2 SeitenButler Lumber Company Funding AnalysisDucNoch keine Bewertungen

- BLDokument4 SeitenBLBBirdMozyNoch keine Bewertungen

- Butler Lumber Company Case Solution CasesolDokument3 SeitenButler Lumber Company Case Solution CasesolTalha SiddiquiNoch keine Bewertungen

- Naturally Cool Water Clay Bottle - 1000ML Self Cooling Handmade Lead FreeDokument1 SeiteNaturally Cool Water Clay Bottle - 1000ML Self Cooling Handmade Lead FreeamanNoch keine Bewertungen

- Approved CAE GuidelineDokument50 SeitenApproved CAE GuidelineamanNoch keine Bewertungen

- Rice Mills of Jharkhand and Their Pollutions Problems by Er. S.K.singhDokument3 SeitenRice Mills of Jharkhand and Their Pollutions Problems by Er. S.K.singhamanNoch keine Bewertungen

- Cost ConceptsDokument33 SeitenCost ConceptsamanNoch keine Bewertungen

- MockExerciseDokument50 SeitenMockExerciseamanNoch keine Bewertungen

- HRM - Sustainability Management - 2016-2018 - PPT I - Introduction and Manpower PlanningDokument90 SeitenHRM - Sustainability Management - 2016-2018 - PPT I - Introduction and Manpower Planningaman0% (1)

- Indian Value System: Ethics. Aristotle in His N.E Part Company WithDokument16 SeitenIndian Value System: Ethics. Aristotle in His N.E Part Company WithamanNoch keine Bewertungen

- Zomatorevenueanalysis 160905035521Dokument16 SeitenZomatorevenueanalysis 160905035521amanNoch keine Bewertungen

- Tech M + MSat Merger Case Study AnalysisDokument21 SeitenTech M + MSat Merger Case Study AnalysisamanNoch keine Bewertungen

- Flexible Budgets and Variance AnalysisDokument46 SeitenFlexible Budgets and Variance AnalysisamanNoch keine Bewertungen

- Stability of The Equilibrium: Reference Material For International Finance Course For Ex-MBA-2016-17Dokument4 SeitenStability of The Equilibrium: Reference Material For International Finance Course For Ex-MBA-2016-17amanNoch keine Bewertungen

- Market Signals & Competitive MovesDokument8 SeitenMarket Signals & Competitive Movesaman100% (1)

- HRM-One Year Full Time Program 2016-2017 - Phase 4-Rewards and CompensationDokument43 SeitenHRM-One Year Full Time Program 2016-2017 - Phase 4-Rewards and CompensationamanNoch keine Bewertungen

- Transfer Pricing Regulations OverviewDokument19 SeitenTransfer Pricing Regulations OverviewamanNoch keine Bewertungen

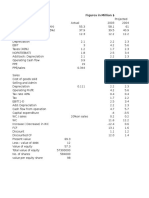

- Monmouth Inc Figures in Million $Dokument3 SeitenMonmouth Inc Figures in Million $amanNoch keine Bewertungen

- Prowess Annual Report Data ComparisonDokument12 SeitenProwess Annual Report Data ComparisonamanNoch keine Bewertungen

- Prowess Annual Report Data ComparisonDokument12 SeitenProwess Annual Report Data ComparisonamanNoch keine Bewertungen

- Market Signals & Competitive MovesDokument8 SeitenMarket Signals & Competitive Movesaman100% (1)

- Prowess Annual Report Data ComparisonDokument12 SeitenProwess Annual Report Data ComparisonamanNoch keine Bewertungen

- PG 367 - Portfolio SelectionDokument2 SeitenPG 367 - Portfolio SelectionamanNoch keine Bewertungen

- 16 - What Are BanksDokument42 Seiten16 - What Are BanksamanNoch keine Bewertungen

- The Marketing Audit Comes of AgeDokument16 SeitenThe Marketing Audit Comes of AgeIsaac AdomNoch keine Bewertungen

- PG406 Advertsising CampaignDokument2 SeitenPG406 Advertsising CampaignamanNoch keine Bewertungen

- 16 Non Performing AssetsDokument80 Seiten16 Non Performing AssetsamanNoch keine Bewertungen

- BLDokument4 SeitenBLamanNoch keine Bewertungen

- Case Analysis High Street 05.01.2017Dokument2 SeitenCase Analysis High Street 05.01.2017amanNoch keine Bewertungen

- Sma EvaDokument15 SeitenSma EvaamanNoch keine Bewertungen

- Ambuja Cement Annual Report 2015 Web Final - PDF 13Dokument170 SeitenAmbuja Cement Annual Report 2015 Web Final - PDF 13amanNoch keine Bewertungen

- Interwar PeriodDokument2 SeitenInterwar PeriodamanNoch keine Bewertungen

- X (No. of Cups) Y (No of Plates) 120 160 Profit $/unit 2 1.5Dokument9 SeitenX (No. of Cups) Y (No of Plates) 120 160 Profit $/unit 2 1.5amanNoch keine Bewertungen

- Doble M4000 User GuideDokument204 SeitenDoble M4000 User GuidePablo Toro Lopez100% (1)

- Cell Membrane TransportDokument37 SeitenCell Membrane TransportMaya AwadNoch keine Bewertungen

- Piping & Instrumentation DiagramDokument6 SeitenPiping & Instrumentation DiagramPruthvi RajaNoch keine Bewertungen

- Ulta Beauty Hiring AgeDokument3 SeitenUlta Beauty Hiring AgeShweta RachaelNoch keine Bewertungen

- Learning Strand I - EnglishDokument19 SeitenLearning Strand I - EnglishMaricel MaapoyNoch keine Bewertungen

- PSY406-MidTerm SolvedbymeDokument6 SeitenPSY406-MidTerm SolvedbymeAhmed RajpootNoch keine Bewertungen

- All India Test Series (2023-24)Dokument22 SeitenAll India Test Series (2023-24)Anil KumarNoch keine Bewertungen

- Sahara ModularDokument12 SeitenSahara ModularDonnarose DiBenedettoNoch keine Bewertungen

- 150W MP3 Car AmplifierDokument5 Seiten150W MP3 Car AmplifiermanosipritirekhaNoch keine Bewertungen

- Biotechnology PDFDokument24 SeitenBiotechnology PDFShyamlaNoch keine Bewertungen

- Rotex Brochure PDFDokument4 SeitenRotex Brochure PDFestramilsolutionNoch keine Bewertungen

- Test Bank For Cultural Diversity in Health and Illness 8th Edition Rachel e SpectorDokument25 SeitenTest Bank For Cultural Diversity in Health and Illness 8th Edition Rachel e SpectorCatherine Smith100% (32)

- FA SSV3013 - Sem 2 2021 - 22Dokument4 SeitenFA SSV3013 - Sem 2 2021 - 22SITI ZUBAIDAH BINTI HALIMNoch keine Bewertungen

- Practice Test Answer Sheets AnswersDokument85 SeitenPractice Test Answer Sheets AnswersDon't Make Me AngryNoch keine Bewertungen

- Notes Micro FinanceDokument9 SeitenNotes Micro Financesofty1980Noch keine Bewertungen

- Environmental Pollution Control (ET ZC362 - WILP Course) : BITS PilaniDokument41 SeitenEnvironmental Pollution Control (ET ZC362 - WILP Course) : BITS Pilanisa_arunkumarNoch keine Bewertungen

- GENBIO2 MOD3 Howlifebeganonearth Forfinalcheck.Dokument26 SeitenGENBIO2 MOD3 Howlifebeganonearth Forfinalcheck.Kris LaglivaNoch keine Bewertungen

- Myth and Folklo-WPS OfficeDokument211 SeitenMyth and Folklo-WPS OfficeAryan A100% (1)

- Fever With Rash in Table Form.Dokument4 SeitenFever With Rash in Table Form.Azizan HannyNoch keine Bewertungen

- Disjointed.S01E03.720p.webrip.x264 STRiFE (Ettv) .SRTDokument32 SeitenDisjointed.S01E03.720p.webrip.x264 STRiFE (Ettv) .SRTArthur CarvalhoNoch keine Bewertungen

- Qhse Induction ModuleDokument20 SeitenQhse Induction Modulerahul kumarNoch keine Bewertungen

- TuflineLinedBallValve 332148 2-07Dokument12 SeitenTuflineLinedBallValve 332148 2-07Marcio NegraoNoch keine Bewertungen

- BiochemistryDokument39 SeitenBiochemistryapi-290667341Noch keine Bewertungen

- Event Details Report - Algoma SteelDokument66 SeitenEvent Details Report - Algoma SteelThe NarwhalNoch keine Bewertungen

- Ch-19 Gas Welding, Gas Cutting & Arc WeldingDokument30 SeitenCh-19 Gas Welding, Gas Cutting & Arc WeldingJAYANT KUMARNoch keine Bewertungen

- Eastern RlyDokument25 SeitenEastern Rlyshivam.jhawar95Noch keine Bewertungen

- Internal Audit Checklist QA Document ReviewDokument5 SeitenInternal Audit Checklist QA Document ReviewThiruMaranAC0% (1)

- Material Safety Data Sheet: Section 1 - Chemical Product and Company IdentificationDokument6 SeitenMaterial Safety Data Sheet: Section 1 - Chemical Product and Company IdentificationHazama HexNoch keine Bewertungen

- Memoir of Glicerio Abad - 2005 - v2Dokument6 SeitenMemoir of Glicerio Abad - 2005 - v2Jane JoveNoch keine Bewertungen