Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Economics Formula SheetDokument10 SeitenEconomics Formula SheetCratos_Poseidon100% (1)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Tutorial 3 QuestionsDokument4 SeitenTutorial 3 Questionswilliamnyx0% (2)

- Cfa Level 1 Mock Test 1Dokument44 SeitenCfa Level 1 Mock Test 1Jyoti Singh50% (2)

- Cfa Level 1 Mock Test 1Dokument44 SeitenCfa Level 1 Mock Test 1Jyoti Singh50% (2)

- Investor Database MumbaiDokument9 SeitenInvestor Database MumbaiVishal JwellNoch keine Bewertungen

- CFA MindmapDokument98 SeitenCFA MindmapHongjun Yin92% (12)

- Cfa Level 1 Mock TestDokument71 SeitenCfa Level 1 Mock TestJyoti Singh100% (1)

- L 1 Mock V 42016 December Am SolutionsDokument76 SeitenL 1 Mock V 42016 December Am SolutionsCratos_PoseidonNoch keine Bewertungen

- Accounting Theory - Chapter 10 Summary/NotesDokument7 SeitenAccounting Theory - Chapter 10 Summary/NotesloveNoch keine Bewertungen

- CFA Level 1 Review - Quantitative MethodsDokument10 SeitenCFA Level 1 Review - Quantitative MethodsAamirx6450% (2)

- Feasibility RestaurantDokument38 SeitenFeasibility Restaurantlendiibanez56% (9)

- Kyle Bass Presentation Hayman Global Outlook Pitfalls and Opportunities For 2014Dokument20 SeitenKyle Bass Presentation Hayman Global Outlook Pitfalls and Opportunities For 2014ValueWalk100% (1)

- L1ss13los46 PDFDokument6 SeitenL1ss13los46 PDFCratos_Poseidon100% (1)

- L 1 Mockv 42016 DecemberpmquestionsDokument44 SeitenL 1 Mockv 42016 Decemberpmquestionsislamasif0% (1)

- Study Plan Cfa Level I 2017Dokument3 SeitenStudy Plan Cfa Level I 2017Cratos_PoseidonNoch keine Bewertungen

- Benefits FinQuiz Question BankDokument3 SeitenBenefits FinQuiz Question BankCratos_PoseidonNoch keine Bewertungen

- L1ss13los46 PDFDokument6 SeitenL1ss13los46 PDFCratos_Poseidon100% (1)

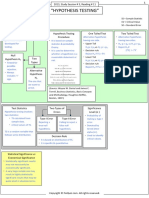

- HypothesisDokument3 SeitenHypothesisCratos_PoseidonNoch keine Bewertungen

- Quantitative Aptitude Formulae SheetDokument15 SeitenQuantitative Aptitude Formulae SheetCratos_Poseidon0% (1)

- FRA Study Session ChartsDokument18 SeitenFRA Study Session ChartsCratos_PoseidonNoch keine Bewertungen

- Sampling & EstimationDokument3 SeitenSampling & EstimationCratos_PoseidonNoch keine Bewertungen

- Net Present Value (NPV) : Orporate InanceDokument27 SeitenNet Present Value (NPV) : Orporate InanceCratos_PoseidonNoch keine Bewertungen

- Probability CompressedDokument2 SeitenProbability CompressedCratos_PoseidonNoch keine Bewertungen

- The Building and Other Constn Workers Rules, A100507Dokument183 SeitenThe Building and Other Constn Workers Rules, A100507Josh Ch100% (1)

- Introduction AccountingDokument103 SeitenIntroduction AccountingSheekuttyNoch keine Bewertungen

- Resolución de Consentimiento Unánime Designando Comité Especial de La Junta para La Investigación de La Deuda de Puerto RicoDokument3 SeitenResolución de Consentimiento Unánime Designando Comité Especial de La Junta para La Investigación de La Deuda de Puerto RicoEmily RamosNoch keine Bewertungen

- Curled Metal Inc.-Engineered Products Division: Case Study AnalysisDokument7 SeitenCurled Metal Inc.-Engineered Products Division: Case Study AnalysisRabia JavaidNoch keine Bewertungen

- Simple and Compound InterestDokument5 SeitenSimple and Compound InterestAnonymous ZVbwfc0% (1)

- Rothstein Studio Spring 2013Dokument4 SeitenRothstein Studio Spring 2013gsappcloudNoch keine Bewertungen

- MCO-05 ENG IgnouDokument51 SeitenMCO-05 ENG Ignousanthi0% (1)

- Alternative Strategies in Financing Working CapitalDokument16 SeitenAlternative Strategies in Financing Working CapitalCharm MendozaNoch keine Bewertungen

- Advanced Financial ManagementDokument201 SeitenAdvanced Financial ManagementNarendra Reddy LokireddyNoch keine Bewertungen

- Entrepreneurship 2nd ExamDokument2 SeitenEntrepreneurship 2nd ExamMerben Almio100% (1)

- The American Taxpayer Relief Act of 2012Dokument2 SeitenThe American Taxpayer Relief Act of 2012Janet BarrNoch keine Bewertungen

- Accounting Framework and ConceptsDokument30 SeitenAccounting Framework and Conceptsyow jing peiNoch keine Bewertungen

- The HP Business Intelligence Maturity Model: Describing The BI JourneyDokument8 SeitenThe HP Business Intelligence Maturity Model: Describing The BI Journeyaiamb4010Noch keine Bewertungen

- Case MapDokument23 SeitenCase MapVidya ChokkalingamNoch keine Bewertungen

- Full Report Ubs Group Ag and Ubs Ag Consolidated 2019 en PDFDokument776 SeitenFull Report Ubs Group Ag and Ubs Ag Consolidated 2019 en PDFMakuna NatsvlishviliNoch keine Bewertungen

- BP010 Business and Process StrategyDokument13 SeitenBP010 Business and Process StrategyparcanjoNoch keine Bewertungen

- FMR Feb08Dokument5 SeitenFMR Feb08Salman ArshadNoch keine Bewertungen

- Rothschilds Inter Alpha GroupDokument3 SeitenRothschilds Inter Alpha Groupradu victor Tapu100% (1)

- ST Telemedia and Tata Communications Complete The Singapore Data Centre Joint Venture Transaction (Company Update)Dokument3 SeitenST Telemedia and Tata Communications Complete The Singapore Data Centre Joint Venture Transaction (Company Update)Shyam SunderNoch keine Bewertungen

- Citigroup Credit Suisse J.P. Morgan Morgan Stanley Standard Chartered BankDokument5 SeitenCitigroup Credit Suisse J.P. Morgan Morgan Stanley Standard Chartered BankhjsfdrNoch keine Bewertungen

- 2009 MFI BenchmarksDokument281 Seiten2009 MFI BenchmarksRogelio CuroNoch keine Bewertungen

- Financial Management I - Chapter 6Dokument34 SeitenFinancial Management I - Chapter 6Mardi UmarNoch keine Bewertungen

- StartUp CompanyDokument7 SeitenStartUp CompanyMiruna Daniela VasileNoch keine Bewertungen

- Taxation Pac Mock s13 PDFDokument3 SeitenTaxation Pac Mock s13 PDFMuhammad Hassan AliNoch keine Bewertungen