Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Splunk 8.1 Fundamentals Part 3Dokument304 SeitenSplunk 8.1 Fundamentals Part 3S Lavanyaa100% (4)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Economics Formula SheetDokument10 SeitenEconomics Formula SheetCratos_Poseidon100% (1)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Cfa Level 1 Mock Test 1Dokument44 SeitenCfa Level 1 Mock Test 1Jyoti Singh50% (2)

- Cfa Level 1 Mock Test 1Dokument44 SeitenCfa Level 1 Mock Test 1Jyoti Singh50% (2)

- CFA Ethics and Professional Standards EnforcementDokument98 SeitenCFA Ethics and Professional Standards EnforcementHongjun Yin92% (12)

- L 1 Mock V 42016 December Am SolutionsDokument76 SeitenL 1 Mock V 42016 December Am SolutionsCratos_PoseidonNoch keine Bewertungen

- Cfa Level 1 Mock TestDokument71 SeitenCfa Level 1 Mock TestJyoti Singh100% (1)

- Review Problems ProjectDokument4 SeitenReview Problems Projectpratiksha1091Noch keine Bewertungen

- A Descriptive Study To Assess The Knowledge Regarding IllDokument51 SeitenA Descriptive Study To Assess The Knowledge Regarding Illkiran mahalNoch keine Bewertungen

- Goodness of Fit Tests - Fstats - ch5 PDFDokument26 SeitenGoodness of Fit Tests - Fstats - ch5 PDFchirpychirpy100% (1)

- L1ss13los46 PDFDokument6 SeitenL1ss13los46 PDFCratos_Poseidon100% (1)

- Study Plan Cfa Level I 2017Dokument3 SeitenStudy Plan Cfa Level I 2017Cratos_PoseidonNoch keine Bewertungen

- L 1 Mockv 42016 DecemberpmquestionsDokument44 SeitenL 1 Mockv 42016 Decemberpmquestionsislamasif0% (1)

- L1ss13los46 PDFDokument6 SeitenL1ss13los46 PDFCratos_Poseidon100% (1)

- Benefits FinQuiz Question BankDokument3 SeitenBenefits FinQuiz Question BankCratos_PoseidonNoch keine Bewertungen

- Probability CompressedDokument2 SeitenProbability CompressedCratos_PoseidonNoch keine Bewertungen

- FRA Study Session ChartsDokument18 SeitenFRA Study Session ChartsCratos_PoseidonNoch keine Bewertungen

- Fra Forumula Book PDFDokument19 SeitenFra Forumula Book PDFCratos_PoseidonNoch keine Bewertungen

- Net Present Value (NPV) : Orporate InanceDokument27 SeitenNet Present Value (NPV) : Orporate InanceCratos_PoseidonNoch keine Bewertungen

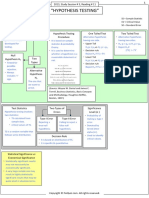

- HypothesisDokument3 SeitenHypothesisCratos_PoseidonNoch keine Bewertungen

- Sampling & EstimationDokument3 SeitenSampling & EstimationCratos_PoseidonNoch keine Bewertungen

- HSCRP Level-0,5Dokument10 SeitenHSCRP Level-0,5Nova SipahutarNoch keine Bewertungen

- Introduction To Probability Tutorial 6 Weeks 7Dokument2 SeitenIntroduction To Probability Tutorial 6 Weeks 7Phan NhưNoch keine Bewertungen

- Sampling Distributions and Hypothesis TestingDokument23 SeitenSampling Distributions and Hypothesis TestingSaurabh Krishna SinghNoch keine Bewertungen

- Document PDFDokument5 SeitenDocument PDFAndre CalmonNoch keine Bewertungen

- Six Sigma Green Belt 3.ANALYSE (IASSC)Dokument99 SeitenSix Sigma Green Belt 3.ANALYSE (IASSC)kachkach zak100% (1)

- 3HE15123AAADTQZZA - V1 - NSP NFM-P 19.11 Statistics Management GuideDokument182 Seiten3HE15123AAADTQZZA - V1 - NSP NFM-P 19.11 Statistics Management GuideEmilioNoch keine Bewertungen

- Statistics for Social Science: DCE5950 Assignment 1 AnalysisDokument3 SeitenStatistics for Social Science: DCE5950 Assignment 1 Analysissnas2206Noch keine Bewertungen

- Electronics For Organoids TumoroidsDokument21 SeitenElectronics For Organoids Tumoroidsarda07Noch keine Bewertungen

- Exercises LU0: Descriptive Statistics: Statistics and Probability DistributionsDokument13 SeitenExercises LU0: Descriptive Statistics: Statistics and Probability DistributionsTiago PaulinoNoch keine Bewertungen

- Notes CH 6Dokument10 SeitenNotes CH 6Charlie RNoch keine Bewertungen

- Effects of Sample Mass On Gravity Recoverable Gold Test Results in Low-Grade OresDokument23 SeitenEffects of Sample Mass On Gravity Recoverable Gold Test Results in Low-Grade Oresjose hernandezNoch keine Bewertungen

- # Constructed Week SamplingDokument17 Seiten# Constructed Week SamplingMei XingNoch keine Bewertungen

- Data Analysis for Physics Laboratory MeasurementsDokument5 SeitenData Analysis for Physics Laboratory Measurementsccouy123Noch keine Bewertungen

- Think StatsDokument142 SeitenThink StatsMichael McClellan100% (2)

- Z Score Calculation in Sri LankaDokument18 SeitenZ Score Calculation in Sri LankaAchala Uthsuka100% (1)

- Landys I Gall 1974 Beauty Is TalentDokument7 SeitenLandys I Gall 1974 Beauty Is TalentSamuel NicholasNoch keine Bewertungen

- A New Algorithm To Reduce and Individualize HRV Recording TimeDokument7 SeitenA New Algorithm To Reduce and Individualize HRV Recording TimeDiego Ricardo Paez ArdilaNoch keine Bewertungen

- Module 1 - INTRODUCTION TO SURVEYINGDokument46 SeitenModule 1 - INTRODUCTION TO SURVEYINGArwen Rae NisperosNoch keine Bewertungen

- Math 142 Co2 2.11Dokument2 SeitenMath 142 Co2 2.11David Keith MauyaoNoch keine Bewertungen

- Analytical Measurement UncertaintyDokument240 SeitenAnalytical Measurement Uncertaintyzilangamba_s4535Noch keine Bewertungen

- Unit-6-Assignment-Discrete Probability Distribution: NUV/SBL/SYBBA/Sem-3/Quantitative Techniques-II/21-22Dokument3 SeitenUnit-6-Assignment-Discrete Probability Distribution: NUV/SBL/SYBBA/Sem-3/Quantitative Techniques-II/21-22Supriya SinghNoch keine Bewertungen

- Engineering Structures: SciencedirectDokument8 SeitenEngineering Structures: SciencedirectFeleki AttilaNoch keine Bewertungen

- Black Belt Body of KnowledgeDokument5 SeitenBlack Belt Body of Knowledgedrsuresh26Noch keine Bewertungen

- Goodness of Fit - SEM PDFDokument52 SeitenGoodness of Fit - SEM PDFAhmad BaihaqiNoch keine Bewertungen

- Presentation Setting Specifications Statistical Considerations Enda Moran Pfizer enDokument16 SeitenPresentation Setting Specifications Statistical Considerations Enda Moran Pfizer enVinay PatelNoch keine Bewertungen

- Measurements - 14 PDFDokument271 SeitenMeasurements - 14 PDFNagesh SarmaNoch keine Bewertungen