Das könnte Ihnen auch gefallen

- Letter of Reference FormDokument2 SeitenLetter of Reference FormmadoNoch keine Bewertungen

- Prep Expert New Sat Essay Shaan PatelDokument269 SeitenPrep Expert New Sat Essay Shaan PatelTien Thanh Thuy Nguyen100% (5)

- Prep Expert New Sat Essay Shaan PatelDokument269 SeitenPrep Expert New Sat Essay Shaan PatelTien Thanh Thuy Nguyen100% (5)

- AbcdefghijklDokument2 SeitenAbcdefghijklmadoNoch keine Bewertungen

- Power PointDokument5 SeitenPower PointmadoNoch keine Bewertungen

- YoyoDokument1 SeiteYoyomadoNoch keine Bewertungen

- Z 6Dokument2 SeitenZ 6madoNoch keine Bewertungen

- AbcdefghijklDokument2 SeitenAbcdefghijklmadoNoch keine Bewertungen

- AbcdefghijklDokument2 SeitenAbcdefghijklmadoNoch keine Bewertungen

- AbcdefghijklDokument2 SeitenAbcdefghijklmadoNoch keine Bewertungen

- AbcdefghijklDokument2 SeitenAbcdefghijklmadoNoch keine Bewertungen

- AbcdefghijklDokument2 SeitenAbcdefghijklmadoNoch keine Bewertungen

- Power PointDokument5 SeitenPower PointmadoNoch keine Bewertungen

- Power PointDokument5 SeitenPower PointmadoNoch keine Bewertungen

- Z 14Dokument5 SeitenZ 14madoNoch keine Bewertungen

- Z 80Dokument5 SeitenZ 80madoNoch keine Bewertungen

- Power PointDokument5 SeitenPower PointmadoNoch keine Bewertungen

- Z 10Dokument5 SeitenZ 10madoNoch keine Bewertungen

- Z 2Dokument5 SeitenZ 2madoNoch keine Bewertungen

- Practice TestDokument5 SeitenPractice TestmadoNoch keine Bewertungen

- Power PointDokument5 SeitenPower PointmadoNoch keine Bewertungen

- Power PointDokument5 SeitenPower PointmadoNoch keine Bewertungen

- Z 6Dokument5 SeitenZ 6madoNoch keine Bewertungen

- Z 82Dokument5 SeitenZ 82madoNoch keine Bewertungen

- Power PointDokument5 SeitenPower PointmadoNoch keine Bewertungen

- Z 71Dokument5 SeitenZ 71madoNoch keine Bewertungen

- Power PointDokument5 SeitenPower PointmadoNoch keine Bewertungen

- Z 70Dokument5 SeitenZ 70madoNoch keine Bewertungen

- Z 75Dokument5 SeitenZ 75madoNoch keine Bewertungen

- Z 68Dokument5 SeitenZ 68madoNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Third Party Application Presentation v1.1Dokument11 SeitenThird Party Application Presentation v1.1Grahame RoganNoch keine Bewertungen

- Britannia Non Functional Test Plan Ver 1.2Dokument26 SeitenBritannia Non Functional Test Plan Ver 1.2Kelli ReillyNoch keine Bewertungen

- 400 PDFDokument4 Seiten400 PDFmsavoooNoch keine Bewertungen

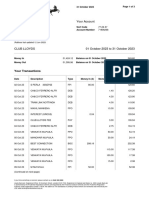

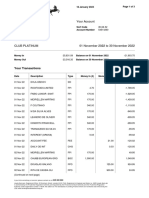

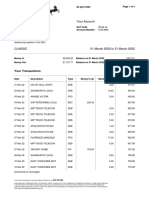

- Statement 10 2023Dokument3 SeitenStatement 10 2023nvmanohar97Noch keine Bewertungen

- O F F E R 2 B MT 103 2way Swift 10+4 Etf 1302 KulDokument2 SeitenO F F E R 2 B MT 103 2way Swift 10+4 Etf 1302 KulPool AtalayaNoch keine Bewertungen

- PreviewdocsDokument2 SeitenPreviewdocsSimon CooperNoch keine Bewertungen

- List of Lease Instruments With Isin No. - Ewyc-Wfc-2012Dokument12 SeitenList of Lease Instruments With Isin No. - Ewyc-Wfc-2012Wajid100% (1)

- Guide On BankingDokument18 SeitenGuide On BankingNathan NakibingeNoch keine Bewertungen

- The Interest Rate On Your Savings Account Is Going Down Soon - 01072020Dokument2 SeitenThe Interest Rate On Your Savings Account Is Going Down Soon - 01072020PawełNoch keine Bewertungen

- 2011-06-10 LLOY UK Consumer Discretionary Sector AnalysisDokument3 Seiten2011-06-10 LLOY UK Consumer Discretionary Sector AnalysiskjlaqiNoch keine Bewertungen

- Naukri SreejaPonduri (5y 6m)Dokument4 SeitenNaukri SreejaPonduri (5y 6m)Rohit BhasinNoch keine Bewertungen

- Lloyds TSB Case Study on Talent Management ProcessDokument16 SeitenLloyds TSB Case Study on Talent Management ProcessNasra MuneerNoch keine Bewertungen

- 2009 Annual ReportDokument273 Seiten2009 Annual ReportFredrik StrömqvistNoch keine Bewertungen

- Statement 2024 FebruaryDokument3 SeitenStatement 2024 Februarycontact.sindicateNoch keine Bewertungen

- Optional: Changes To Customer AddressDokument2 SeitenOptional: Changes To Customer Addressبريجينيف خروتشوفNoch keine Bewertungen

- Business Analyst Payments ExpertDokument4 SeitenBusiness Analyst Payments Expertmgajbhe1Noch keine Bewertungen

- S1.0 MAACS Lloyds TSB Group CS A EN 0 4 2013Dokument19 SeitenS1.0 MAACS Lloyds TSB Group CS A EN 0 4 2013Hongwei ZhangNoch keine Bewertungen

- Rbs Abnamro Project ReportDokument42 SeitenRbs Abnamro Project ReportAbhishek SharmaNoch keine Bewertungen

- Radar Economics - UK Inflation Forecasts - July 2022Dokument3 SeitenRadar Economics - UK Inflation Forecasts - July 2022ThomasNoch keine Bewertungen

- Lloyd Bank 2Dokument12 SeitenLloyd Bank 2jtopuNoch keine Bewertungen

- Case List - Banking LawDokument6 SeitenCase List - Banking LawMarina DragiyskaNoch keine Bewertungen

- Statement 2022 11Dokument3 SeitenStatement 2022 11GustavoNoch keine Bewertungen

- Global StrategyDokument12 SeitenGlobal StrategyBrian Kwaba (Sossy)Noch keine Bewertungen

- Uganda Christian University Faculty of Law Module: Banking and Negotiable Instruments LLB 4Dokument14 SeitenUganda Christian University Faculty of Law Module: Banking and Negotiable Instruments LLB 4Classic Willy Mark AchipuNoch keine Bewertungen

- Lloyds Bank logo historyDokument4 SeitenLloyds Bank logo historyDulo WegnerNoch keine Bewertungen

- Jul Statement FinalDokument3 SeitenJul Statement FinalAbdul HadiNoch keine Bewertungen

- DocumenteDokument5 SeitenDocumentemaxim caldarasanNoch keine Bewertungen

- 99A9EAE4-739B-4884-B42F-3E5FD3C4ABA4Dokument12 Seiten99A9EAE4-739B-4884-B42F-3E5FD3C4ABA4Jakub S.100% (1)

- Gopi Reddy Mainframe Developer ResumeDokument4 SeitenGopi Reddy Mainframe Developer ResumeGopi ReddyNoch keine Bewertungen

- EDEKA - Kaiser's Tengelmann-Prohibition of Merger Overridden by Minister For Economic Affairs in GermanyDokument5 SeitenEDEKA - Kaiser's Tengelmann-Prohibition of Merger Overridden by Minister For Economic Affairs in GermanyKanoknai ThawonphanitNoch keine Bewertungen