Das könnte Ihnen auch gefallen

- Summary 2Dokument5 SeitenSummary 2Karin NafilaNoch keine Bewertungen

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersVon EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNoch keine Bewertungen

- International Financial Statement Analysis WorkbookVon EverandInternational Financial Statement Analysis WorkbookNoch keine Bewertungen

- Accounting For Non-Profit OrganizationsDokument39 SeitenAccounting For Non-Profit Organizationsrevel_13193% (29)

- Accounting For Public CHAPTER ONE-WPS OfficeDokument14 SeitenAccounting For Public CHAPTER ONE-WPS Officehaymanot gizachewNoch keine Bewertungen

- What is Financial Accounting and BookkeepingVon EverandWhat is Financial Accounting and BookkeepingBewertung: 4 von 5 Sternen4/5 (10)

- Financial Statements: A Simplified Easy Accounting and Business Owner Guide to Understanding and Creating Financial ReportsVon EverandFinancial Statements: A Simplified Easy Accounting and Business Owner Guide to Understanding and Creating Financial ReportsNoch keine Bewertungen

- Accounting Survival Guide: An Introduction to Accounting for BeginnersVon EverandAccounting Survival Guide: An Introduction to Accounting for BeginnersNoch keine Bewertungen

- Submitted To: Submitted By: Dr. Ranjit Singh Kunal Sharma (IMB2018013) Gokul Krishana (IMB2018012)Dokument27 SeitenSubmitted To: Submitted By: Dr. Ranjit Singh Kunal Sharma (IMB2018013) Gokul Krishana (IMB2018012)gokulkNoch keine Bewertungen

- Corporate Financial Mastering: Simple Methods and Strategies to Financial Analysis MasteringVon EverandCorporate Financial Mastering: Simple Methods and Strategies to Financial Analysis MasteringNoch keine Bewertungen

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Von Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Noch keine Bewertungen

- Finance For Non-Finance Executives: The Concept of Responsibility CentresDokument31 SeitenFinance For Non-Finance Executives: The Concept of Responsibility Centressuresh.srinivasnNoch keine Bewertungen

- Ch-1 Acct For P&CSDokument7 SeitenCh-1 Acct For P&CSDawit NegashNoch keine Bewertungen

- Governmental and Not Profit AccountingDokument4 SeitenGovernmental and Not Profit AccountingPahladsingh100% (1)

- Accounts and Audit Project Legal Provision Regarding Annual Accounts of A CompanyDokument24 SeitenAccounts and Audit Project Legal Provision Regarding Annual Accounts of A CompanyAmit KumarNoch keine Bewertungen

- Consolidated Financial StatementsDokument32 SeitenConsolidated Financial StatementsPeetu WadhwaNoch keine Bewertungen

- The Essentials of Finance and Accounting for Nonfinancial ManagersVon EverandThe Essentials of Finance and Accounting for Nonfinancial ManagersBewertung: 5 von 5 Sternen5/5 (1)

- Accounting For Non-Profit OrganizationsDokument38 SeitenAccounting For Non-Profit Organizationsrevel_131100% (1)

- Chapter - 04 Financial Statement For Non Profit Making OrganizationDokument71 SeitenChapter - 04 Financial Statement For Non Profit Making OrganizationAuthor Jyoti Prakash rathNoch keine Bewertungen

- FABM Q3 L2. SLeM - 2S - Q3 - W2 Accounting Concept & PrinciplesDokument16 SeitenFABM Q3 L2. SLeM - 2S - Q3 - W2 Accounting Concept & PrinciplesSophia MagdaraogNoch keine Bewertungen

- Learn Financial ReportsDokument6 SeitenLearn Financial ReportsMai RuizNoch keine Bewertungen

- Government Accountant: Federal Accounting Standards Advisory Board (FASB) - Government Accounting Standards Board (GASB)Dokument5 SeitenGovernment Accountant: Federal Accounting Standards Advisory Board (FASB) - Government Accounting Standards Board (GASB)Glaiza GiganteNoch keine Bewertungen

- Fra Notes (Questions and Answers Format) : Financial Reporting: Meaning, Objectives and Importance UNIT-1Dokument74 SeitenFra Notes (Questions and Answers Format) : Financial Reporting: Meaning, Objectives and Importance UNIT-1paras pant100% (1)

- Fiscal Management ReviewerDokument4 SeitenFiscal Management ReviewerSham Cervantes LopezNoch keine Bewertungen

- Textbook of Urgent Care Management: Chapter 12, Pro Forma Financial StatementsVon EverandTextbook of Urgent Care Management: Chapter 12, Pro Forma Financial StatementsNoch keine Bewertungen

- C213 Study Guide - SolutionDokument23 SeitenC213 Study Guide - Solutiondesouzas.ldsNoch keine Bewertungen

- Finance Leverage Capital Markets Money Management: Importance-And-Limitations/61727Dokument7 SeitenFinance Leverage Capital Markets Money Management: Importance-And-Limitations/61727GUDDUNoch keine Bewertungen

- GK - Gov Act 2019Dokument38 SeitenGK - Gov Act 2019Glenn GalvezNoch keine Bewertungen

- PronouncementDokument23 SeitenPronouncementPhilipa Meilinda PutriNoch keine Bewertungen

- 16 - Not For Profit Organisation - An Introduction (134 KB) PDFDokument14 Seiten16 - Not For Profit Organisation - An Introduction (134 KB) PDFramneekdadwalNoch keine Bewertungen

- Government and NFP Assignment SolutionDokument5 SeitenGovernment and NFP Assignment SolutionHabte DebeleNoch keine Bewertungen

- LRN - Pre U Assignment - Foundation Accounting - FINAL - May 2020Dokument2 SeitenLRN - Pre U Assignment - Foundation Accounting - FINAL - May 2020treasurestrendy8Noch keine Bewertungen

- Fra - Ese Final Notes Feb23Dokument32 SeitenFra - Ese Final Notes Feb23mohdsahil2438Noch keine Bewertungen

- FinMan Module 3 FS, Cash Flow and TaxesDokument10 SeitenFinMan Module 3 FS, Cash Flow and Taxeserickson hernanNoch keine Bewertungen

- Abm Lesson 1aDokument4 SeitenAbm Lesson 1aAgri BasketNoch keine Bewertungen

- Discuss The Users of Financial Information Internal UsersDokument6 SeitenDiscuss The Users of Financial Information Internal UsersStephen Pilar PortilloNoch keine Bewertungen

- AAT Paper 2 FinanceDokument4 SeitenAAT Paper 2 FinanceRay LaiNoch keine Bewertungen

- 2 Branches of AccountingDokument28 Seiten2 Branches of Accountingapi-267023512100% (2)

- Chapter 2 BRANCHES OF ACCOUNTINGDokument20 SeitenChapter 2 BRANCHES OF ACCOUNTINGmarkalvinlagunero1991Noch keine Bewertungen

- Karthika.m.reji Finance Assignment.Dokument12 SeitenKarthika.m.reji Finance Assignment.Rama NathanNoch keine Bewertungen

- Accounting For Non-Profit OrganizationsDokument40 SeitenAccounting For Non-Profit Organizationsrevel_131100% (7)

- Nonprofit AccountingDokument10 SeitenNonprofit AccountingRoschelle MiguelNoch keine Bewertungen

- CH 01 SM 9eDokument10 SeitenCH 01 SM 9eSophia HaJeong KimNoch keine Bewertungen

- Introduction To AccountingDokument5 SeitenIntroduction To AccountingMardy DahuyagNoch keine Bewertungen

- Understanding Financial Statements (Review and Analysis of Straub's Book)Von EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Bewertung: 5 von 5 Sternen5/5 (5)

- Presentation of Finan Cial Statements Ias 1Dokument30 SeitenPresentation of Finan Cial Statements Ias 1Nurul KabirNoch keine Bewertungen

- Writing Unit 1Dokument8 SeitenWriting Unit 1Yulinda SaledaNoch keine Bewertungen

- Financial StatementDokument17 SeitenFinancial StatementNaveen AggarwalNoch keine Bewertungen

- Balance Sheet: What Do You Mean by Corporate Financial Statements?Dokument3 SeitenBalance Sheet: What Do You Mean by Corporate Financial Statements?maabachaNoch keine Bewertungen

- Resume PSA Group 8Dokument4 SeitenResume PSA Group 820312472Noch keine Bewertungen

- M and ADokument5 SeitenM and AChe Tanifor BanksNoch keine Bewertungen

- Case Study on TATA Motors' Acquisition of Jaguar and Land RoverDokument8 SeitenCase Study on TATA Motors' Acquisition of Jaguar and Land RoverChe Tanifor BanksNoch keine Bewertungen

- Financial Project Report On Asian PaintsDokument37 SeitenFinancial Project Report On Asian PaintsChe Tanifor Banks80% (5)

- Financial Project Report On Asian PaintsDokument37 SeitenFinancial Project Report On Asian PaintsChe Tanifor Banks80% (5)

- Lending Norm of An InstitutionDokument4 SeitenLending Norm of An InstitutionChe Tanifor BanksNoch keine Bewertungen

- Marion Chapter One 7bDokument19 SeitenMarion Chapter One 7bChe Tanifor BanksNoch keine Bewertungen

- Heineken Beer CASE STUDYDokument47 SeitenHeineken Beer CASE STUDYSaurabh Chaudhari100% (1)

- Solution Manual For Fundamentals of Advanced Accounting 7th Edition by HoyleDokument44 SeitenSolution Manual For Fundamentals of Advanced Accounting 7th Edition by HoyleJuana Terry100% (32)

- Multiple RibbonDokument5 SeitenMultiple RibbonSuresh Ram RNoch keine Bewertungen

- Bài Tập 2-27 - Nhóm8LớpKN007Dokument6 SeitenBài Tập 2-27 - Nhóm8LớpKN007nguyenhongNoch keine Bewertungen

- 101-Accounting For Buisness DecisionsDokument268 Seiten101-Accounting For Buisness DecisionsAkshay GadeNoch keine Bewertungen

- Bad Debts Structured 2019 PDFDokument16 SeitenBad Debts Structured 2019 PDFArshad ChaudharyNoch keine Bewertungen

- Pengaruh Moderasi Kualitas Audit Terhadap Hubungan Fleksibilitas Akuntansi Dengan Real Earning ManagementDokument23 SeitenPengaruh Moderasi Kualitas Audit Terhadap Hubungan Fleksibilitas Akuntansi Dengan Real Earning ManagementDias 24Noch keine Bewertungen

- Basic Accounting Course ModuleDokument5 SeitenBasic Accounting Course ModuleBlairEmrallafNoch keine Bewertungen

- 001 Unit Three Intangible Assets 2020Dokument11 Seiten001 Unit Three Intangible Assets 2020scoormcxNoch keine Bewertungen

- Acct 2011 Anderson Pty LTD Is An Australian Diversified IndustrialDokument2 SeitenAcct 2011 Anderson Pty LTD Is An Australian Diversified IndustrialCharlotteNoch keine Bewertungen

- Balance Sheet M&MDokument2 SeitenBalance Sheet M&MRitik AggarwalNoch keine Bewertungen

- Break-Even Analysis PDFDokument4 SeitenBreak-Even Analysis PDFirvin5de5los5riosNoch keine Bewertungen

- Jolly's Java and Bakery Bakery Business Plan Executive SummaryDokument28 SeitenJolly's Java and Bakery Bakery Business Plan Executive SummaryAtlasLiuNoch keine Bewertungen

- Assignment AnsDokument6 SeitenAssignment AnsVAIGESWARI A/P MANIAM STUDENTNoch keine Bewertungen

- Financial Management Theory and Practice 15th Edition Brigham Solutions ManualDokument36 SeitenFinancial Management Theory and Practice 15th Edition Brigham Solutions Manualrappelpotherueo100% (29)

- 07 DCF Steel Dynamics AfterDokument2 Seiten07 DCF Steel Dynamics AfterJack JacintoNoch keine Bewertungen

- PMF Unit 5Dokument10 SeitenPMF Unit 5dummy manNoch keine Bewertungen

- Latest Development of IFRS (and HKFRS) : Nelson Lam Nelson Lam 林智遠 林智遠Dokument32 SeitenLatest Development of IFRS (and HKFRS) : Nelson Lam Nelson Lam 林智遠 林智遠ChanNoch keine Bewertungen

- Goal Incongruence and Roi Bleefi Corporation Manufactures FurniDokument1 SeiteGoal Incongruence and Roi Bleefi Corporation Manufactures Furnitrilocksp SinghNoch keine Bewertungen

- UntitledDokument20 SeitenUntitledĐăng Nguyễn HảiNoch keine Bewertungen

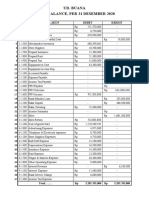

- UD. Buana Trial Balance 2020Dokument10 SeitenUD. Buana Trial Balance 2020HusniBaroqNoch keine Bewertungen

- Operating, Financial & Combined LeverageDokument13 SeitenOperating, Financial & Combined Leveragem_manjari_gNoch keine Bewertungen

- VERTICAL ANALYSIS OF INCOME STATEMENT of Toyota 2022-2021Dokument8 SeitenVERTICAL ANALYSIS OF INCOME STATEMENT of Toyota 2022-2021Touqeer HussainNoch keine Bewertungen

- Hershey Case StudyDokument16 SeitenHershey Case StudyNino50% (2)

- Chapter-7 Pracrice Exercise (Seatwork) Marato, Jedediah SamuelDokument3 SeitenChapter-7 Pracrice Exercise (Seatwork) Marato, Jedediah SamuelJedediah Samuel Marato0% (1)

- Preparing simple consolidated financialsDokument10 SeitenPreparing simple consolidated financialstapia4yeabuNoch keine Bewertungen

- Painting ContractDokument22 SeitenPainting Contractagrvinit123Noch keine Bewertungen

- Module 1 - Financial Statement Analysis - P2Dokument4 SeitenModule 1 - Financial Statement Analysis - P2Jose Eduardo GumafelixNoch keine Bewertungen

- Cfas - Journal EntriesDokument3 SeitenCfas - Journal EntriesJefferson SarmientoNoch keine Bewertungen

- Taguro Trucking FinancialsDokument5 SeitenTaguro Trucking FinancialsDavid GuevarraNoch keine Bewertungen