Das könnte Ihnen auch gefallen

- CMA Cs Executive Dec-2018 New Syllabus QuestionsDokument12 SeitenCMA Cs Executive Dec-2018 New Syllabus QuestionsSonu KeswaniNoch keine Bewertungen

- Company and Cost ManagementDokument11 SeitenCompany and Cost ManagementPadmambigai Chandra SekaranNoch keine Bewertungen

- Advanced Accounts MTP M21 S2Dokument19 SeitenAdvanced Accounts MTP M21 S2Harshwardhan PatilNoch keine Bewertungen

- Test Series: April, 2021 Mock Test Paper - 2 Intermediate (New) : Group - Ii Paper - 5: Advanced AccountingDokument6 SeitenTest Series: April, 2021 Mock Test Paper - 2 Intermediate (New) : Group - Ii Paper - 5: Advanced AccountingOcto ManNoch keine Bewertungen

- A.M.U. Aligarh Senior Secondary School Certificate Examination Model Question Paper Class XII AccountancyDokument77 SeitenA.M.U. Aligarh Senior Secondary School Certificate Examination Model Question Paper Class XII AccountancyMohammad FarazNoch keine Bewertungen

- BK Prelims ComDokument6 SeitenBK Prelims ComAafreen QureshiNoch keine Bewertungen

- Company Accounts, Cost and Management AccountingDokument10 SeitenCompany Accounts, Cost and Management AccountingmeetwithsanjayNoch keine Bewertungen

- Ca-Ii May 2022Dokument6 SeitenCa-Ii May 2022Gayathri V GNoch keine Bewertungen

- 629 19PCM10 19PCZ09 Mcom Mcom CA 05 02 2022 FNDokument19 Seiten629 19PCM10 19PCZ09 Mcom Mcom CA 05 02 2022 FNMukesh kannan MahiNoch keine Bewertungen

- Valuation of GoodwillDokument15 SeitenValuation of Goodwillbtsa1262013Noch keine Bewertungen

- Academic Session 2022 MAY 2022 Semester: AssignmentDokument6 SeitenAcademic Session 2022 MAY 2022 Semester: AssignmentChristopher KipsangNoch keine Bewertungen

- MTP 17 53 Questions 1710507531Dokument9 SeitenMTP 17 53 Questions 1710507531janasenalogNoch keine Bewertungen

- Company Accounts and Cost & Management Accounting: Part-ADokument9 SeitenCompany Accounts and Cost & Management Accounting: Part-AOm PrakashNoch keine Bewertungen

- 12th Cbse - QPDokument11 Seiten12th Cbse - QPAmirtha MNoch keine Bewertungen

- 13 Financial Accounting - April May 2021 (Freshers CBCS 2020-21 and Onwards)Dokument15 Seiten13 Financial Accounting - April May 2021 (Freshers CBCS 2020-21 and Onwards)Rakesh MaliNoch keine Bewertungen

- Gujarat Technological UniversityDokument3 SeitenGujarat Technological UniversityRenieNoch keine Bewertungen

- PART-B Analysis Test YtDokument8 SeitenPART-B Analysis Test YtRiddhi GuptaNoch keine Bewertungen

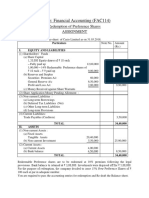

- FAC114 Financial Accounting Redemption of Preference SharesDokument4 SeitenFAC114 Financial Accounting Redemption of Preference SharesDhairya ShahNoch keine Bewertungen

- FM 15-16Dokument3 SeitenFM 15-16BrijmohanNoch keine Bewertungen

- Internal ReconstructionDokument26 SeitenInternal ReconstructionRajesh NangaliaNoch keine Bewertungen

- Accountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Dokument3 SeitenAccountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Kairav KhuranaNoch keine Bewertungen

- BCM 4206 Corporate Finance PDFDokument4 SeitenBCM 4206 Corporate Finance PDFSimon silaNoch keine Bewertungen

- Question PaperDokument3 SeitenQuestion PaperAmbrishNoch keine Bewertungen

- Cma Inter G2 Account & Audit MTP SolutionDokument30 SeitenCma Inter G2 Account & Audit MTP SolutionGeethika KesavarapuNoch keine Bewertungen

- Cma Question PaperDokument4 SeitenCma Question PaperHilary GaureaNoch keine Bewertungen

- Adv Acc - 3 CHDokument21 SeitenAdv Acc - 3 CHhassan nassereddineNoch keine Bewertungen

- B.B.A., Sem.-IV CC-213: Corporate Financial StatementsDokument4 SeitenB.B.A., Sem.-IV CC-213: Corporate Financial StatementsJJ NayakNoch keine Bewertungen

- Accounting concepts and statutory auditDokument4 SeitenAccounting concepts and statutory auditNamrata RamgadeNoch keine Bewertungen

- QP CODE: 22100973: Reg No: NameDokument6 SeitenQP CODE: 22100973: Reg No: NameSajithaNoch keine Bewertungen

- NR 310106 MepaDokument8 SeitenNR 310106 MepaSrinivasa Rao GNoch keine Bewertungen

- Board Exam Question Paper on Secretarial Practice from February 2020Dokument2 SeitenBoard Exam Question Paper on Secretarial Practice from February 2020Ashwini NaleNoch keine Bewertungen

- Secretarial Practical March 2020 STD 12th Commerce HSC Maharashtra Board Question PaperDokument2 SeitenSecretarial Practical March 2020 STD 12th Commerce HSC Maharashtra Board Question PaperShubham ParmarNoch keine Bewertungen

- Secretarial Practical March 2020 STD 12th Commerce HSC Maharashtra Board Question PaperDokument2 SeitenSecretarial Practical March 2020 STD 12th Commerce HSC Maharashtra Board Question PaperShubham ParmarNoch keine Bewertungen

- Book Keeping & Accountancy (50) : AttemptDokument11 SeitenBook Keeping & Accountancy (50) : AttemptRashi thiNoch keine Bewertungen

- CAFM FULL SYLLABUS FREE TEST DEC 23-Executive-RevisionDokument7 SeitenCAFM FULL SYLLABUS FREE TEST DEC 23-Executive-Revisionyogeetha saiNoch keine Bewertungen

- Marks: Compulsory. Questions From CompulsoryDokument20 SeitenMarks: Compulsory. Questions From Compulsorysupercell.mail.helpshift.sharingNoch keine Bewertungen

- Commerce (Regular) Accounting For Specialised Institutions (Group A: Accounting and Finance) Paper - 3.5 (A)Dokument4 SeitenCommerce (Regular) Accounting For Specialised Institutions (Group A: Accounting and Finance) Paper - 3.5 (A)Sanaullah M SultanpurNoch keine Bewertungen

- Accountancy: KeepingDokument11 SeitenAccountancy: KeepingRashi thiNoch keine Bewertungen

- © The Institute of Chartered Accountants of IndiaDokument24 Seiten© The Institute of Chartered Accountants of IndiaAniketNoch keine Bewertungen

- Accs June 16Dokument8 SeitenAccs June 16manasNoch keine Bewertungen

- FABVDokument10 SeitenFABVdivyayella024Noch keine Bewertungen

- PST Fundamentals of Finance 2015 2022Dokument58 SeitenPST Fundamentals of Finance 2015 2022benard owinoNoch keine Bewertungen

- Question No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswerDokument5 SeitenQuestion No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswercdNoch keine Bewertungen

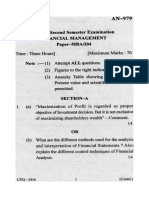

- An 979 MBA Sem II Financial Management14Dokument4 SeitenAn 979 MBA Sem II Financial Management14Riya AgrawalNoch keine Bewertungen

- Cainterseries 2 CompleteDokument70 SeitenCainterseries 2 CompleteNishanthNoch keine Bewertungen

- Adv Accounts MTP M19 S2Dokument22 SeitenAdv Accounts MTP M19 S2Harshwardhan PatilNoch keine Bewertungen

- 03-22-2022 - 121512 Book Keeping and Accountancy Test PaperDokument5 Seiten03-22-2022 - 121512 Book Keeping and Accountancy Test Papertestestestest54Noch keine Bewertungen

- Answer All Questions: (8 Marks)Dokument9 SeitenAnswer All Questions: (8 Marks)manojNoch keine Bewertungen

- CRV - Valuation - ExerciseDokument15 SeitenCRV - Valuation - ExerciseVrutika ShahNoch keine Bewertungen

- Daf1301 Fundamentals of Accounting Ii - Digital AssignmentDokument6 SeitenDaf1301 Fundamentals of Accounting Ii - Digital AssignmentcyrusNoch keine Bewertungen

- Ii Puc AccountsDokument3 SeitenIi Puc AccountsShekarKrishnappaNoch keine Bewertungen

- CA Bcom PH 3rd Sem 2016Dokument7 SeitenCA Bcom PH 3rd Sem 2016Gursirat KaurNoch keine Bewertungen

- Vidya Sagar Career Institute Limited Mobile: 93514 - 68666 Phone: 7821821250 / 51 / 52 / 53 / 54Dokument9 SeitenVidya Sagar Career Institute Limited Mobile: 93514 - 68666 Phone: 7821821250 / 51 / 52 / 53 / 54shrenik bhuratNoch keine Bewertungen

- Board Question Paper: September 2021: Book Keeping & AccountancyDokument5 SeitenBoard Question Paper: September 2021: Book Keeping & AccountancyPriyansh ShahNoch keine Bewertungen

- Roll No. ..................................... : Part-A 1Dokument4 SeitenRoll No. ..................................... : Part-A 1Milan vcNoch keine Bewertungen

- IPS Academy, IBMR Session Jan-June 2020 BBA II Semester: Assignment Of: Financial ManagementDokument6 SeitenIPS Academy, IBMR Session Jan-June 2020 BBA II Semester: Assignment Of: Financial ManagementDrShailesh Singh ThakurNoch keine Bewertungen

- BK - July Board 2023Dokument11 SeitenBK - July Board 2023akshaydevendra09Noch keine Bewertungen

- Cash & Investment Management for Nonprofit OrganizationsVon EverandCash & Investment Management for Nonprofit OrganizationsNoch keine Bewertungen

- Corporate Actions: A Guide to Securities Event ManagementVon EverandCorporate Actions: A Guide to Securities Event ManagementNoch keine Bewertungen

- Handbook of Asset and Liability Management: From Models to Optimal Return StrategiesVon EverandHandbook of Asset and Liability Management: From Models to Optimal Return StrategiesNoch keine Bewertungen

- WL 31 Summary Charts by Swapnil Patni Sir Allied LawsDokument6 SeitenWL 31 Summary Charts by Swapnil Patni Sir Allied LawsSuppy PNoch keine Bewertungen

- Web It CertDokument1 SeiteWeb It CertSuppy PNoch keine Bewertungen

- WL 33 Summary Charts by Swapnil Patni Sir Corporate Laws Part BDokument9 SeitenWL 33 Summary Charts by Swapnil Patni Sir Corporate Laws Part BSuppy PNoch keine Bewertungen

- Clarification on Accounting Standards and Guidance Notes StatusDokument1 SeiteClarification on Accounting Standards and Guidance Notes StatusSuppy PNoch keine Bewertungen

- DT-Amendment by FA 16Dokument196 SeitenDT-Amendment by FA 16Suppy PNoch keine Bewertungen

- E BGM On Customs and FTP Jan19 PDFDokument96 SeitenE BGM On Customs and FTP Jan19 PDFSuppy PNoch keine Bewertungen

- E BGM On Customs and FTP Jan19 PDFDokument96 SeitenE BGM On Customs and FTP Jan19 PDFSuppy PNoch keine Bewertungen

- ICAI - Overview of GST - CA Final PDFDokument34 SeitenICAI - Overview of GST - CA Final PDFsarvjeet_kaushalNoch keine Bewertungen

- SCS 2010 12Dokument35 SeitenSCS 2010 12Suppy PNoch keine Bewertungen

- Scs Nov - Dec 2014Dokument64 SeitenScs Nov - Dec 2014Suppy PNoch keine Bewertungen

- Industrial, Labcs Question PapeDokument20 SeitenIndustrial, Labcs Question PapeRajat GargNoch keine Bewertungen

- SCS 2011 05 PDFDokument34 SeitenSCS 2011 05 PDFSuppy PNoch keine Bewertungen

- Instructions:: Question Paper Booklet CodeDokument20 SeitenInstructions:: Question Paper Booklet CodeSuppy PNoch keine Bewertungen

- MRF - Senior - Chief Manager TaxDokument2 SeitenMRF - Senior - Chief Manager TaxSuppy PNoch keine Bewertungen

- SCS 2007 12Dokument51 SeitenSCS 2007 12Suppy PNoch keine Bewertungen

- SCS 2010 04Dokument51 SeitenSCS 2010 04Suppy PNoch keine Bewertungen

- SCS 2007 03Dokument36 SeitenSCS 2007 03Suppy PNoch keine Bewertungen

- SCS 2007 09Dokument43 SeitenSCS 2007 09Suppy PNoch keine Bewertungen

- SCS 2008 03Dokument44 SeitenSCS 2008 03Suppy PNoch keine Bewertungen

- SCS 2007 10Dokument50 SeitenSCS 2007 10Suppy PNoch keine Bewertungen

- Student Company Secretary: HighlightsDokument39 SeitenStudent Company Secretary: HighlightsSuppy PNoch keine Bewertungen

- SCS 2008 01Dokument43 SeitenSCS 2008 01Suppy PNoch keine Bewertungen

- SCS 2008 03Dokument44 SeitenSCS 2008 03Suppy PNoch keine Bewertungen

- SCS 2008 01Dokument43 SeitenSCS 2008 01Suppy PNoch keine Bewertungen

- SCS 2008 04Dokument52 SeitenSCS 2008 04Suppy PNoch keine Bewertungen

- SCS 2011 05 PDFDokument34 SeitenSCS 2011 05 PDFSuppy PNoch keine Bewertungen

- Student Company Secretary: HighlightsDokument39 SeitenStudent Company Secretary: HighlightsSuppy PNoch keine Bewertungen

- SCS 2006 07Dokument36 SeitenSCS 2006 07Suppy PNoch keine Bewertungen

- SCSMAR2010Dokument51 SeitenSCSMAR2010dogpaaNoch keine Bewertungen

- SCS 2006 01Dokument40 SeitenSCS 2006 01Suppy PNoch keine Bewertungen

- Acct 260 Chapter 10Dokument27 SeitenAcct 260 Chapter 10John Guy100% (1)

- Spanish Colonial Economic Policies in the PhilippinesDokument2 SeitenSpanish Colonial Economic Policies in the Philippinesrichard canlasNoch keine Bewertungen

- 2018 Full Budget ReviewDokument299 Seiten2018 Full Budget ReviewSundayTimesZANoch keine Bewertungen

- Capital Budgeting Techniques and PracticeDokument17 SeitenCapital Budgeting Techniques and PracticeDias Nurliana PutraNoch keine Bewertungen

- L 3 QCF Cnl99 - Unit 2 - BR - Assignment BriefDokument12 SeitenL 3 QCF Cnl99 - Unit 2 - BR - Assignment BriefRajiv VyasNoch keine Bewertungen

- FINANCIAL WOES AT COMMUNITY HOSPITALDokument23 SeitenFINANCIAL WOES AT COMMUNITY HOSPITALSherry Yong PkTianNoch keine Bewertungen

- Federalism Position PaperDokument5 SeitenFederalism Position PaperRheena Gayle Rioflorido EguiaNoch keine Bewertungen

- Managing Financial Resources and DecisionsDokument18 SeitenManaging Financial Resources and DecisionsAbdullahAlNomunNoch keine Bewertungen

- Ifrs Usgaap NotesDokument38 SeitenIfrs Usgaap Notesaum_thai100% (1)

- House Bill 161Dokument8 SeitenHouse Bill 161KevinOhlandtNoch keine Bewertungen

- Money Planner - A5Dokument14 SeitenMoney Planner - A5vicka100% (7)

- Budgeting ProjectDokument17 SeitenBudgeting Projectapi-311074931Noch keine Bewertungen

- TaxationDokument742 SeitenTaxationSrinivasa Rao Bandlamudi83% (6)

- Responsibility CentresDokument25 SeitenResponsibility CentresParamjit Sharma100% (2)

- Coa C2006-003Dokument2 SeitenCoa C2006-003Russel SarachoNoch keine Bewertungen

- Local Fiscal AdministrationDokument20 SeitenLocal Fiscal AdministrationMarie Reyes71% (14)

- Ra 9184Dokument3 SeitenRa 9184Randolf FernandezNoch keine Bewertungen

- Servitech Institute Asia confidential budget projectionsDokument3 SeitenServitech Institute Asia confidential budget projectionsJayMoralesNoch keine Bewertungen

- M.A. Syllabus 2012-13Dokument71 SeitenM.A. Syllabus 2012-13BUNTY KUMARNoch keine Bewertungen

- Lecture 22 Structure of Federal GovtDokument33 SeitenLecture 22 Structure of Federal GovtalikhanNoch keine Bewertungen

- Project 2 COST - ENG ReportDokument3 SeitenProject 2 COST - ENG ReportFreddieNoch keine Bewertungen

- Kanohar Electricals Limited: Ra BillDokument2 SeitenKanohar Electricals Limited: Ra BillAnoop Dikshit100% (1)

- Cost Overrun in The Case of Nib International Bank Headquarters Building ProjectDokument11 SeitenCost Overrun in The Case of Nib International Bank Headquarters Building ProjectEsayas Getachew100% (1)

- New CR Search: Forward Prev Hit Back Homepage Hit List HelpDokument4 SeitenNew CR Search: Forward Prev Hit Back Homepage Hit List HelpJoseph Ford Jr.100% (5)

- Finance Act 2013 Edition IIIDokument72 SeitenFinance Act 2013 Edition IIIAbdul Basit KtkNoch keine Bewertungen

- Notice: Agency Information Collection Activities Proposals, Submissions, and ApprovalsDokument2 SeitenNotice: Agency Information Collection Activities Proposals, Submissions, and ApprovalsJustia.comNoch keine Bewertungen

- Santa Barbara Budget Book 10-11 CompleteDokument716 SeitenSanta Barbara Budget Book 10-11 CompleteGlenn HendrixNoch keine Bewertungen

- Costing Formulas PDFDokument86 SeitenCosting Formulas PDFsubbu100% (3)

- ACCCB - 543 Competency 2 Assessment and Rubric - Acccb543 - v1P3 - Comp - 2 - RubricDokument3 SeitenACCCB - 543 Competency 2 Assessment and Rubric - Acccb543 - v1P3 - Comp - 2 - Rubricledmabaya23Noch keine Bewertungen

- Eric Woon Kim Thak: Education/QualificationDokument1 SeiteEric Woon Kim Thak: Education/Qualificationeric woonNoch keine Bewertungen