Das könnte Ihnen auch gefallen

- Contract Review Rev2 1208Dokument19 SeitenContract Review Rev2 1208Viswanathan SrkNoch keine Bewertungen

- A 240 - A 240M - 04 - Qti0mc0wnaDokument12 SeitenA 240 - A 240M - 04 - Qti0mc0wnaViswanathan SrkNoch keine Bewertungen

- Passivate Stainless Steel PartsDokument2 SeitenPassivate Stainless Steel PartsViswanathan SrkNoch keine Bewertungen

- Tables of International Standards, A ComparisonDokument22 SeitenTables of International Standards, A ComparisonViswanathan SrkNoch keine Bewertungen

- 316 PDFDokument1 Seite316 PDFViswanathan SrkNoch keine Bewertungen

- Araldite Ay 103 1Dokument1 SeiteAraldite Ay 103 1Viswanathan SrkNoch keine Bewertungen

- Technical Reference Guide Fastenal K Factor and MoreDokument62 SeitenTechnical Reference Guide Fastenal K Factor and Moredlight0Noch keine Bewertungen

- 316 PDFDokument1 Seite316 PDFViswanathan SrkNoch keine Bewertungen

- SW InsightDokument13 SeitenSW InsightViswanathan SrkNoch keine Bewertungen

- Araldite Ay103 1hy991 PDFDokument4 SeitenAraldite Ay103 1hy991 PDFViswanathan SrkNoch keine Bewertungen

- Araldite Ay103 1hy991 PDFDokument4 SeitenAraldite Ay103 1hy991 PDFViswanathan SrkNoch keine Bewertungen

- Araldite Ay103 1hy991 PDFDokument4 SeitenAraldite Ay103 1hy991 PDFViswanathan SrkNoch keine Bewertungen

- SSWWWWDokument6 SeitenSSWWWWViswanathan SrkNoch keine Bewertungen

- SW DailyDokument32 SeitenSW DailyViswanathan SrkNoch keine Bewertungen

- GateDokument6 SeitenGateParveen SwamiNoch keine Bewertungen

- Project1 - Diagram1Dokument1 SeiteProject1 - Diagram1Viswanathan SrkNoch keine Bewertungen

- Antelope 21 December 2015Dokument3 SeitenAntelope 21 December 2015Viswanathan SrkNoch keine Bewertungen

- Moneylife 12 November 2015Dokument68 SeitenMoneylife 12 November 2015Viswanathan SrkNoch keine Bewertungen

- Wi 2015 12Dokument64 SeitenWi 2015 12Viswanathan SrkNoch keine Bewertungen

- Shaper Tool Head AssemblyDokument6 SeitenShaper Tool Head Assemblyjagadeesh01Noch keine Bewertungen

- Ex 3 BDokument1 SeiteEx 3 BViswanathan SrkNoch keine Bewertungen

- Ex 4 BDokument1 SeiteEx 4 BViswanathan SrkNoch keine Bewertungen

- Ex 4 ADokument3 SeitenEx 4 AViswanathan SrkNoch keine Bewertungen

- Ex 3 ADokument2 SeitenEx 3 AViswanathan SrkNoch keine Bewertungen

- Ex 1 BDokument1 SeiteEx 1 BViswanathan SrkNoch keine Bewertungen

- Ex 4 ADokument3 SeitenEx 4 AViswanathan SrkNoch keine Bewertungen

- Ex 2 ADokument2 SeitenEx 2 AViswanathan SrkNoch keine Bewertungen

- For The First Time in India, Electrodes Put in Australian Man's Brain To Curb Depression - The Times of IndiaDokument6 SeitenFor The First Time in India, Electrodes Put in Australian Man's Brain To Curb Depression - The Times of IndiaViswanathan SrkNoch keine Bewertungen

- Ex 1 ADokument2 SeitenEx 1 AViswanathan SrkNoch keine Bewertungen

- Working Mind and The Thinking Mind - Lifestyle Article On SpeakingtreeDokument3 SeitenWorking Mind and The Thinking Mind - Lifestyle Article On SpeakingtreeViswanathan SrkNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Trend Following (Bank Nifty)Dokument13 SeitenTrend Following (Bank Nifty)aliaNoch keine Bewertungen

- 9706 s04 MsDokument20 Seiten9706 s04 Msroukaiya_peerkhanNoch keine Bewertungen

- Bài 12 - Bài tập thực hànhDokument2 SeitenBài 12 - Bài tập thực hànhDuyên BùiNoch keine Bewertungen

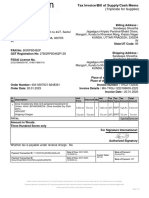

- Invoice DocumentDokument1 SeiteInvoice DocumentrameshNoch keine Bewertungen

- Dissertation Topics in Financial EconomicsDokument5 SeitenDissertation Topics in Financial EconomicsOrderAPaperOnlineUK100% (1)

- Corporate Governance JournalDokument17 SeitenCorporate Governance JournalJoseph LimbongNoch keine Bewertungen

- Unit 4 Dividend DecisionsDokument17 SeitenUnit 4 Dividend Decisionsrahul ramNoch keine Bewertungen

- Fundamentals of Financial Management 15Th Edition Brigham Solutions Manual Full Chapter PDFDokument58 SeitenFundamentals of Financial Management 15Th Edition Brigham Solutions Manual Full Chapter PDFJustinDuartepaej100% (10)

- Soalan Pengambilalihansoalan PengambilalihanDokument1 SeiteSoalan Pengambilalihansoalan PengambilalihanNur FahanaNoch keine Bewertungen

- Pledge Real Mortgage Chattel Mortgage AntichresisDokument12 SeitenPledge Real Mortgage Chattel Mortgage AntichresisKATHERINEMARIE DIMAUNAHANNoch keine Bewertungen

- Internal Control and Cash: Learning ObjectivesDokument75 SeitenInternal Control and Cash: Learning ObjectivesazertyuNoch keine Bewertungen

- Audit of Receivables: Cebu Cpar Center, IncDokument10 SeitenAudit of Receivables: Cebu Cpar Center, IncEvita Ayne TapitNoch keine Bewertungen

- Chapter 17Dokument48 SeitenChapter 17Shiv NarayanNoch keine Bewertungen

- Contemporary Issues Facing The Filipino Entrepreneur: MODULE 10 - Applied EconomicsDokument5 SeitenContemporary Issues Facing The Filipino Entrepreneur: MODULE 10 - Applied EconomicsAstxilNoch keine Bewertungen

- Name of Investors (Bidders) Interest Rate (%) Auction Volume (Billion Dong)Dokument2 SeitenName of Investors (Bidders) Interest Rate (%) Auction Volume (Billion Dong)Trần Phương AnhNoch keine Bewertungen

- International BusinessDokument7 SeitenInternational BusinessAarnav BengeriNoch keine Bewertungen

- MPERS - Section 3 - MASB 1 - MFRS 101 - Financial Statement PresentationDokument8 SeitenMPERS - Section 3 - MASB 1 - MFRS 101 - Financial Statement Presentationckin1609Noch keine Bewertungen

- Private Equity & Venture Capital: in The Middle East & AfricaDokument16 SeitenPrivate Equity & Venture Capital: in The Middle East & AfricaLewoye BantieNoch keine Bewertungen

- UntitledDokument122 SeitenUntitledAdi ShaktiNoch keine Bewertungen

- Post Test AK2Dokument51 SeitenPost Test AK2thalita najellaNoch keine Bewertungen

- Chapter 25 Mergers and AcquisitionsDokument22 SeitenChapter 25 Mergers and Acquisitionsyn customcaseNoch keine Bewertungen

- Cost Accounting FNLDokument13 SeitenCost Accounting FNLImthe OneNoch keine Bewertungen

- SAP FICO Online Training and Placement - Online Training in SAPDokument18 SeitenSAP FICO Online Training and Placement - Online Training in SAPOnline Training in SAPNoch keine Bewertungen

- Auditing Theory QuizzerDokument9 SeitenAuditing Theory QuizzerMilcah Deloso SantosNoch keine Bewertungen

- How To Increase Your Net Worth: (Including Our Investments)Dokument3 SeitenHow To Increase Your Net Worth: (Including Our Investments)Meghal SivanNoch keine Bewertungen

- Analisis Kinerja Keuangan PT - Bank Mandiri Syariah, TBK Periode 2016-2020 Menggunakan Metode Du Pont SystemDokument7 SeitenAnalisis Kinerja Keuangan PT - Bank Mandiri Syariah, TBK Periode 2016-2020 Menggunakan Metode Du Pont SystemJasika Jurnal Sistem Informasi AkuntansiNoch keine Bewertungen

- Tata AIA Life Insurance Smart Sampoorna Raksha TandCDokument31 SeitenTata AIA Life Insurance Smart Sampoorna Raksha TandCAnkit Maheshwari /WealthMitra/Delhi/Dwarka/Noch keine Bewertungen

- A Comparative Study of Home Loan Schemes of Private Sector Banks Public Sector BanksDokument12 SeitenA Comparative Study of Home Loan Schemes of Private Sector Banks Public Sector BanksKapil KumarNoch keine Bewertungen

- FCMB Group PLC 3Q13 (IFRS) Group Results Investors & Analysts PresentationDokument32 SeitenFCMB Group PLC 3Q13 (IFRS) Group Results Investors & Analysts PresentationOladipupo Mayowa PaulNoch keine Bewertungen

- Unit - 1 Introduction To AuditingDokument10 SeitenUnit - 1 Introduction To AuditingDarshan PanditNoch keine Bewertungen