Das könnte Ihnen auch gefallen

- The Role of National Bank For Agriculture and Rural Development (Nabard) in Agriculture and Rural DevelopmentDokument1 SeiteThe Role of National Bank For Agriculture and Rural Development (Nabard) in Agriculture and Rural DevelopmentGreatway ServicesNoch keine Bewertungen

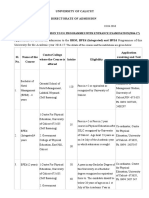

- Recgnized Courses On23Nov2015Dokument7 SeitenRecgnized Courses On23Nov2015Greatway ServicesNoch keine Bewertungen

- Phone:-Director Office FAX WWW - Kerala.gov - in 0471-2305230 0471-2305193 0471-2301740Dokument2 SeitenPhone:-Director Office FAX WWW - Kerala.gov - in 0471-2305230 0471-2305193 0471-2301740Greatway ServicesNoch keine Bewertungen

- Co - Operative BankDokument31 SeitenCo - Operative BankGreatway ServicesNoch keine Bewertungen

- ProfileDokument1 SeiteProfileGreatway ServicesNoch keine Bewertungen

- 12 Chapter 4Dokument45 Seiten12 Chapter 4Greatway ServicesNoch keine Bewertungen

- 2 - Steps For Kiosk Banking SolutionDokument1 Seite2 - Steps For Kiosk Banking SolutionGreatway ServicesNoch keine Bewertungen

- P!Vhil®Ifim111Nitm S@D ©if N&Ib&Irb) : Chapter-VDokument26 SeitenP!Vhil®Ifim111Nitm S@D ©if N&Ib&Irb) : Chapter-VGreatway ServicesNoch keine Bewertungen

- Fast Track ReportDokument29 SeitenFast Track ReportGreatway ServicesNoch keine Bewertungen

- Fast Track ReportDokument29 SeitenFast Track ReportGreatway ServicesNoch keine Bewertungen

- Evening Brach in Co Operative BankDokument28 SeitenEvening Brach in Co Operative BankGreatway ServicesNoch keine Bewertungen

- A Study On Fishermen Co-Operative Society in KeralaDokument24 SeitenA Study On Fishermen Co-Operative Society in KeralaGreatway Services0% (1)

- Co - Operative Banks in Kerala - An OverviewDokument27 SeitenCo - Operative Banks in Kerala - An Overviewmalayali100100% (1)

- Chapter-2 Review of Literature: Bhatia (1978), in His Study Titled, "Banking Structure and Performance A CaseDokument28 SeitenChapter-2 Review of Literature: Bhatia (1978), in His Study Titled, "Banking Structure and Performance A CaseApoorvaNoch keine Bewertungen

- Norka PDFDokument1 SeiteNorka PDFGreatway ServicesNoch keine Bewertungen

- Multi State Co-Operatives Bill PDFDokument29 SeitenMulti State Co-Operatives Bill PDFGreatway ServicesNoch keine Bewertungen

- Ug Ent NotifDokument3 SeitenUg Ent NotifGreatway ServicesNoch keine Bewertungen

- A Study of Financial Perfomence of Salisbury Tea Factory, GudalurDokument27 SeitenA Study of Financial Perfomence of Salisbury Tea Factory, GudalurGreatway Services50% (2)

- Compensation ManagementDokument11 SeitenCompensation ManagementGreatway ServicesNoch keine Bewertungen

- El Guadual Children Center - ColumbiaDokument14 SeitenEl Guadual Children Center - ColumbiaGreatway ServicesNoch keine Bewertungen

- 03 Principles of Programming and Problem Solving - HssliveDokument5 Seiten03 Principles of Programming and Problem Solving - HssliveGreatway ServicesNoch keine Bewertungen

- Haj Committee of India: Haj Application Form For Haj - 1438 (H) - 2017 (Ce)Dokument4 SeitenHaj Committee of India: Haj Application Form For Haj - 1438 (H) - 2017 (Ce)Greatway ServicesNoch keine Bewertungen

- NORKADokument1 SeiteNORKAGreatway ServicesNoch keine Bewertungen

- Kasturirangan Report 2013Dokument175 SeitenKasturirangan Report 2013prijucpNoch keine Bewertungen

- WES ApplicationDokument5 SeitenWES ApplicationGreatway ServicesNoch keine Bewertungen

- 02 Components of The Computer System - HssliveDokument10 Seiten02 Components of The Computer System - HssliveGreatway ServicesNoch keine Bewertungen

- Etreasury ManualDokument14 SeitenEtreasury ManualGreatway ServicesNoch keine Bewertungen

- ONLINE User Manual SocietyDokument21 SeitenONLINE User Manual Societylotus@79Noch keine Bewertungen

- Tiruchirappalli District Co-Operative Milk Producers Union LimitedDokument27 SeitenTiruchirappalli District Co-Operative Milk Producers Union LimitedGreatway ServicesNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Industry and Community Project: Jacobs - Creating A Smart Systems Approach To Future Cities Project OutlineDokument14 SeitenIndustry and Community Project: Jacobs - Creating A Smart Systems Approach To Future Cities Project OutlineCalebNoch keine Bewertungen

- Case Study Analysis - WeWorkDokument8 SeitenCase Study Analysis - WeWorkHervé Kubwimana50% (2)

- 1ST Term J1 Fine Art-1Dokument22 Seiten1ST Term J1 Fine Art-1Peter Omovigho Dugbo100% (1)

- A Vision System For Surface Roughness Characterization Using The Gray Level Co-Occurrence MatrixDokument12 SeitenA Vision System For Surface Roughness Characterization Using The Gray Level Co-Occurrence MatrixPraveen KumarNoch keine Bewertungen

- Manuscript PDFDokument50 SeitenManuscript PDFMartina Mae Benig GinoNoch keine Bewertungen

- Previous Year Questions Tnusrb S. I - 2010: Part - A': General KnowledgeDokument21 SeitenPrevious Year Questions Tnusrb S. I - 2010: Part - A': General Knowledgemohamed AzathNoch keine Bewertungen

- AREMA Shoring GuidelinesDokument25 SeitenAREMA Shoring GuidelinesKCHESTER367% (3)

- 120 Câu Tìm Từ Đồng Nghĩa-Trái Nghĩa-Dap AnDokument9 Seiten120 Câu Tìm Từ Đồng Nghĩa-Trái Nghĩa-Dap AnAlex TranNoch keine Bewertungen

- FT FocusDokument19 SeitenFT Focusobi1kenobyNoch keine Bewertungen

- Zkp8006 Posperu Inc SacDokument2 SeitenZkp8006 Posperu Inc SacANDREA BRUNO SOLANONoch keine Bewertungen

- Final Matatag Epp Tle CG 2023 Grades 4 10Dokument184 SeitenFinal Matatag Epp Tle CG 2023 Grades 4 10DIVINE GRACE CABAHUGNoch keine Bewertungen

- Sungbo's Eredo, Southern Nigeria: Nyame Akuma NoDokument7 SeitenSungbo's Eredo, Southern Nigeria: Nyame Akuma NosalatudeNoch keine Bewertungen

- Tso C197Dokument6 SeitenTso C197rdpereirNoch keine Bewertungen

- Activity Sheet Housekeeping Week - 8 - Grades 9-10Dokument5 SeitenActivity Sheet Housekeeping Week - 8 - Grades 9-10Anne AlejandrinoNoch keine Bewertungen

- T Rex PumpDokument4 SeitenT Rex PumpWong DaNoch keine Bewertungen

- O Repensar Da Fonoaudiologia Na Epistemologia CienDokument5 SeitenO Repensar Da Fonoaudiologia Na Epistemologia CienClaudilla L.Noch keine Bewertungen

- Cash Budget Sharpe Corporation S Projected Sales First 8 Month oDokument1 SeiteCash Budget Sharpe Corporation S Projected Sales First 8 Month oAmit PandeyNoch keine Bewertungen

- CCTV Guidelines - Commission Letter Dated 27.08.2022Dokument2 SeitenCCTV Guidelines - Commission Letter Dated 27.08.2022Sumeet TripathiNoch keine Bewertungen

- Malampaya Case StudyDokument15 SeitenMalampaya Case StudyMark Kenneth ValerioNoch keine Bewertungen

- Choosing An Effective Visual ToolDokument9 SeitenChoosing An Effective Visual ToolAdil Bin KhalidNoch keine Bewertungen

- Discover It For StudentsDokument1 SeiteDiscover It For StudentsVinod ChintalapudiNoch keine Bewertungen

- Menara PMB Assessment Criteria Score SummaryDokument2 SeitenMenara PMB Assessment Criteria Score SummarySyerifaizal Hj. MustaphaNoch keine Bewertungen

- STRUNK V THE STATE OF CALIFORNIA Etal. NYND 16-cv-1496 (BKS / DJS) OSC WITH TRO Filed 12-15-2016 For 3 Judge Court Electoral College ChallengeDokument1.683 SeitenSTRUNK V THE STATE OF CALIFORNIA Etal. NYND 16-cv-1496 (BKS / DJS) OSC WITH TRO Filed 12-15-2016 For 3 Judge Court Electoral College ChallengeChristopher Earl Strunk100% (1)

- NSTP SlabDokument2 SeitenNSTP SlabCherine Fates MangulabnanNoch keine Bewertungen

- Acc 106 Account ReceivablesDokument40 SeitenAcc 106 Account ReceivablesAmirah NordinNoch keine Bewertungen

- Research Paper On Marketing PlanDokument4 SeitenResearch Paper On Marketing Planfvhacvjd100% (1)

- T10 - PointersDokument3 SeitenT10 - PointersGlory of Billy's Empire Jorton KnightNoch keine Bewertungen

- Intraoperative RecordDokument2 SeitenIntraoperative Recordademaala06100% (1)

- Alem Ketema Proposal NewDokument25 SeitenAlem Ketema Proposal NewLeulNoch keine Bewertungen

- Resolution: Owner/Operator, DocketedDokument4 SeitenResolution: Owner/Operator, DocketedDonna Grace Guyo100% (1)