Das könnte Ihnen auch gefallen

- Software Associates Case AnalysisDokument8 SeitenSoftware Associates Case AnalysisMuhammad AsifNoch keine Bewertungen

- About The Software Associates CaseDokument7 SeitenAbout The Software Associates CaseNikita GulguleNoch keine Bewertungen

- Software AssociatesDokument6 SeitenSoftware Associatesshshank pandeyNoch keine Bewertungen

- Midwest Ice Cream CompanyDokument5 SeitenMidwest Ice Cream CompanyPG93Noch keine Bewertungen

- Software Associates Venky SolutionDokument9 SeitenSoftware Associates Venky SolutionabcdfNoch keine Bewertungen

- Software AssociatesDokument5 SeitenSoftware AssociatesAgrata Pandey77% (13)

- Case Analysis - Rosemont Hill Health Center - V3Dokument8 SeitenCase Analysis - Rosemont Hill Health Center - V3thearpan100% (2)

- Hallstead JewellersDokument5 SeitenHallstead JewellersZikuz Sar50% (2)

- Precision Motors Division CaseDokument9 SeitenPrecision Motors Division CaseAliza Rizvi50% (2)

- Project - Rosemont Hill Health CenterDokument9 SeitenProject - Rosemont Hill Health CenterDamian G. James100% (3)

- Appex CorporationDokument5 SeitenAppex CorporationNandanaNoch keine Bewertungen

- 16-2 Prestige Telephone CompanyDokument3 Seiten16-2 Prestige Telephone CompanyYJ26126100% (5)

- Case Classic Pen Company Activity Based CostingDokument20 SeitenCase Classic Pen Company Activity Based CostingAlee Di Vaio83% (6)

- Making A Tough Personnel Decision at Nova Waterfront HotelDokument11 SeitenMaking A Tough Personnel Decision at Nova Waterfront HotelSiddharthNoch keine Bewertungen

- Case: Danshui Plant No. 2: Presented By:-Group 9Dokument7 SeitenCase: Danshui Plant No. 2: Presented By:-Group 9LOKESH YADAV100% (2)

- Wilkerson Case SubmissionDokument5 SeitenWilkerson Case Submissiongangster91100% (2)

- PIA Hawaii Emirates Easy Jet: Breakeven AnalysisDokument3 SeitenPIA Hawaii Emirates Easy Jet: Breakeven AnalysissaadsahilNoch keine Bewertungen

- Case Study: Danshui Plant No2Dokument3 SeitenCase Study: Danshui Plant No2Abdelhamid JenzriNoch keine Bewertungen

- Managerial Accounting - Hallstead Jewelers CaseDokument2 SeitenManagerial Accounting - Hallstead Jewelers Casesxzhou23100% (1)

- 21PGDM152 - RACHIT MRINAL - Don't Bother Me, Can't Cope AssignmentDokument6 Seiten21PGDM152 - RACHIT MRINAL - Don't Bother Me, Can't Cope AssignmentRachit Mrinal100% (3)

- Mystic SportsDokument6 SeitenMystic SportsBatista Firangi100% (2)

- Hallstead Jewelers PDFDokument9 SeitenHallstead Jewelers PDFRaghav JainNoch keine Bewertungen

- Millichem Solution XDokument6 SeitenMillichem Solution XMuhammad JunaidNoch keine Bewertungen

- Halstead JewlersDokument8 SeitenHalstead JewlersZeeshan Ali100% (1)

- Running Head: HALLSTEAD JEWELERS 1Dokument12 SeitenRunning Head: HALLSTEAD JEWELERS 1KathGu100% (1)

- E0311 Hallstead JewelersDokument2 SeitenE0311 Hallstead Jewelersaltemurcan kursunlu100% (1)

- Waltham Oil and Lube CentreDokument5 SeitenWaltham Oil and Lube CentreAnirudh Singh0% (2)

- Crystal Meadows of TahoeDokument8 SeitenCrystal Meadows of TahoePrashuk Sethi100% (1)

- Cost Management - Software Associate CaseDokument7 SeitenCost Management - Software Associate CaseVaibhav GuptaNoch keine Bewertungen

- Prestige Telephone Company Case StudyDokument4 SeitenPrestige Telephone Company Case StudyNur Al Ahad92% (12)

- Alberta Gauge Company CaseDokument2 SeitenAlberta Gauge Company Casenidhu291Noch keine Bewertungen

- Mile High CyclesDokument3 SeitenMile High CyclesAmmar Hassan100% (4)

- Case Analysis Rosemont Hill Health Center V3 PDFDokument8 SeitenCase Analysis Rosemont Hill Health Center V3 PDFPoorvi SinghalNoch keine Bewertungen

- Managers We Are Katti With You - PPL - Group-4Dokument11 SeitenManagers We Are Katti With You - PPL - Group-4kjhathiNoch keine Bewertungen

- Rosemont Health Center Rev01Dokument7 SeitenRosemont Health Center Rev01Amit VishwakarmaNoch keine Bewertungen

- Case Study MOPDokument6 SeitenCase Study MOPLorenc BogovikuNoch keine Bewertungen

- Symphony TheatreDokument6 SeitenSymphony TheatrePrakash Iyer50% (2)

- Danshui Plant 2Dokument1 SeiteDanshui Plant 2Ankit VermaNoch keine Bewertungen

- Waltham Oil and Lube WorkingsDokument5 SeitenWaltham Oil and Lube WorkingsGaurav Sahu100% (1)

- Lilac Flour Mills: Managerial Accounting and Control - IIDokument9 SeitenLilac Flour Mills: Managerial Accounting and Control - IISoni Kumari50% (4)

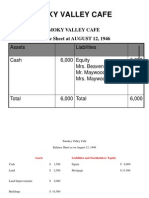

- Smoky Valley CafeDokument3 SeitenSmoky Valley Cafemohit_namanNoch keine Bewertungen

- Danshui Plant 2Dokument13 SeitenDanshui Plant 2Bernard EugineNoch keine Bewertungen

- Group 4 Project 3 (Rev 1)Dokument10 SeitenGroup 4 Project 3 (Rev 1)Ashley Winters100% (1)

- Classic Pen Case CompanyDokument4 SeitenClassic Pen Case CompanymokotoNoch keine Bewertungen

- Crystal Meadows of TahoeDokument5 SeitenCrystal Meadows of TahoeNikitha Andrea Saldanha80% (5)

- About Delwarca: Delwarca Software Solutions Remote Support UnitDokument5 SeitenAbout Delwarca: Delwarca Software Solutions Remote Support UnitRajas ShahadeNoch keine Bewertungen

- Solution Wilkerson CompanyDokument10 SeitenSolution Wilkerson CompanyHIMANSHU AGRAWAL67% (3)

- Hallstead JewelersDokument9 SeitenHallstead Jewelerskaran_w350% (4)

- Case Study Analysis: Delwarca Software Remote Support UnitDokument8 SeitenCase Study Analysis: Delwarca Software Remote Support UnitAkash BhagatNoch keine Bewertungen

- Octane Service StationDokument8 SeitenOctane Service StationKalyan Kumar83% (6)

- Cable Contractor - Aishwarya - Anand - SolankiDokument1 SeiteCable Contractor - Aishwarya - Anand - SolankiAishwarya SolankiNoch keine Bewertungen

- Software Associates-Variance Analysis and Flexible BudgetingDokument4 SeitenSoftware Associates-Variance Analysis and Flexible Budgetingk_Dashy846550% (2)

- Chemalite BDokument12 SeitenChemalite BTatsat Pandey100% (2)

- Software Associate SolutionDokument6 SeitenSoftware Associate SolutionAnupam SinghNoch keine Bewertungen

- Manac Asn3 Software AssociatesDokument6 SeitenManac Asn3 Software AssociatesNikhil JindalNoch keine Bewertungen

- Profit Prior To IncorporationDokument6 SeitenProfit Prior To IncorporationKitty CattyNoch keine Bewertungen

- BLT FINAL Assignment (Feb - June 2020) FINALDokument16 SeitenBLT FINAL Assignment (Feb - June 2020) FINALSalman SajidNoch keine Bewertungen

- Financial Performance Report TemplateDokument2 SeitenFinancial Performance Report TemplateNgọc VânNoch keine Bewertungen

- Amended Tax Credit Certificate 2022: 9371000KA Pps NoDokument2 SeitenAmended Tax Credit Certificate 2022: 9371000KA Pps NoJose ArevaloNoch keine Bewertungen

- Chapter 13 Capital Budgeting Estimating Cash Flow and Analyzing Risk Answers To End of Chapter Questions 13 3 Since The Cost of Capital Includes A Premium For Expected Inflation Failure 1Dokument8 SeitenChapter 13 Capital Budgeting Estimating Cash Flow and Analyzing Risk Answers To End of Chapter Questions 13 3 Since The Cost of Capital Includes A Premium For Expected Inflation Failure 1ghzNoch keine Bewertungen

- FAC Assignment - Section A - Group 9Dokument9 SeitenFAC Assignment - Section A - Group 9Sahil ShethNoch keine Bewertungen

- Indian Financial Systems, Institutions and Markets - NPADokument84 SeitenIndian Financial Systems, Institutions and Markets - NPASahil Sheth100% (1)

- Leadership and SocialisationDokument29 SeitenLeadership and SocialisationSahil ShethNoch keine Bewertungen

- TQM Hyatt PuneDokument15 SeitenTQM Hyatt PuneSahil Sheth0% (2)

- Craig Pinto (3253) Sahil Sheth (3276) Siddharth Kundu (3278) Yusuf Hakim (3288)Dokument7 SeitenCraig Pinto (3253) Sahil Sheth (3276) Siddharth Kundu (3278) Yusuf Hakim (3288)Sahil ShethNoch keine Bewertungen

- Corporate Social Responsibility: Business Ethics ProjectDokument17 SeitenCorporate Social Responsibility: Business Ethics ProjectSahil ShethNoch keine Bewertungen

- Oracle IRecruitment Setup V 1.1Dokument14 SeitenOracle IRecruitment Setup V 1.1Irfan AhmadNoch keine Bewertungen

- A Brief History & Development of Banking in India and Its FutureDokument12 SeitenA Brief History & Development of Banking in India and Its FutureMani KrishNoch keine Bewertungen

- Cmvli DigestsDokument7 SeitenCmvli Digestsbeth_afanNoch keine Bewertungen

- Mass of Christ The Savior by Dan Schutte LyricsDokument1 SeiteMass of Christ The Savior by Dan Schutte LyricsMark Greg FyeFye II33% (3)

- Employee Engagement ReportDokument51 SeitenEmployee Engagement Reportradhika100% (1)

- Change Management and Configuration ManagementDokument5 SeitenChange Management and Configuration ManagementTống Phước HuyNoch keine Bewertungen

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Dokument1 SeiteTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Raj SakariaNoch keine Bewertungen

- Iron Maiden - Can I Play With MadnessDokument9 SeitenIron Maiden - Can I Play With MadnessJuliano Mendes de Oliveira NetoNoch keine Bewertungen

- Company Profile 2018: However, The Cover Is ExcludedDokument16 SeitenCompany Profile 2018: However, The Cover Is ExcludedJimmy R. Mendoza LeguaNoch keine Bewertungen

- File:///d - /... SER/Desktop/LABOR LAW/Cases/G.R. No. 196036, October 23, 2013 - ELIZABETH M..TXT (8/24/2020 9:55:51 PM)Dokument6 SeitenFile:///d - /... SER/Desktop/LABOR LAW/Cases/G.R. No. 196036, October 23, 2013 - ELIZABETH M..TXT (8/24/2020 9:55:51 PM)Russ TuazonNoch keine Bewertungen

- Rothkopf, in Prase of Cultural ImperialismDokument17 SeitenRothkopf, in Prase of Cultural Imperialismmystery1871Noch keine Bewertungen

- BPM at Hindustan Coca Cola Beverages - NMIMS, MumbaiDokument10 SeitenBPM at Hindustan Coca Cola Beverages - NMIMS, MumbaiMojaNoch keine Bewertungen

- MH15 - Street WarsDokument78 SeitenMH15 - Street WarsBrin Bly100% (1)

- Orwell's 1984 & Hegemony in RealityDokument3 SeitenOrwell's 1984 & Hegemony in RealityAlex JosephNoch keine Bewertungen

- Petersen S 4 Wheel Off Road December 2015Dokument248 SeitenPetersen S 4 Wheel Off Road December 20154lexx100% (1)

- Randy C de Lara 2.1Dokument2 SeitenRandy C de Lara 2.1Jane ParaisoNoch keine Bewertungen

- 24 BL-BK SP List (2930130900)Dokument56 Seiten24 BL-BK SP List (2930130900)CapricorniusxxNoch keine Bewertungen

- European Decarb Industry Report ICFDokument52 SeitenEuropean Decarb Industry Report ICFGitan ChopraNoch keine Bewertungen

- Military Aircraft SpecsDokument9 SeitenMilitary Aircraft Specszstratto100% (2)

- HB 76 SummaryDokument4 SeitenHB 76 SummaryJordan SchraderNoch keine Bewertungen

- 520082272054091201Dokument1 Seite520082272054091201Shaikh AdilNoch keine Bewertungen

- My Father's Goes To Cour 12-2Dokument34 SeitenMy Father's Goes To Cour 12-2Marlene Rochelle Joy ViernesNoch keine Bewertungen

- 2018-2019 D7030 Rotaract Plans and Objectives (English) PDFDokument58 Seiten2018-2019 D7030 Rotaract Plans and Objectives (English) PDFDynutha AdonisNoch keine Bewertungen

- Urban Planning PHD Thesis PDFDokument6 SeitenUrban Planning PHD Thesis PDFsandracampbellreno100% (2)

- Debit Card Replacement Kiosk Locations v2Dokument3 SeitenDebit Card Replacement Kiosk Locations v2aiaiyaya33% (3)

- Conditions of The Ahmediya Mohammediya Tijaniya PathDokument12 SeitenConditions of The Ahmediya Mohammediya Tijaniya PathsamghanusNoch keine Bewertungen

- Marxism and Brontë - Revenge As IdeologyDokument8 SeitenMarxism and Brontë - Revenge As IdeologyJonas SaldanhaNoch keine Bewertungen

- Unit 4Dokument8 SeitenUnit 4Gió's ĐôngNoch keine Bewertungen

- Existentialist EthicsDokument6 SeitenExistentialist EthicsCarlos Peconcillo ImperialNoch keine Bewertungen

- Case Digest: Dante O. Casibang vs. Honorable Narciso A. AquinoDokument3 SeitenCase Digest: Dante O. Casibang vs. Honorable Narciso A. AquinoMaria Cherrylen Castor Quijada100% (1)

- Getting to Yes: How to Negotiate Agreement Without Giving InVon EverandGetting to Yes: How to Negotiate Agreement Without Giving InBewertung: 4 von 5 Sternen4/5 (652)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Von EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Bewertung: 4.5 von 5 Sternen4.5/5 (14)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindVon EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindBewertung: 5 von 5 Sternen5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Von EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Bewertung: 4.5 von 5 Sternen4.5/5 (15)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineVon EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNoch keine Bewertungen

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesVon EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNoch keine Bewertungen

- The Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingVon EverandThe Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingBewertung: 4.5 von 5 Sternen4.5/5 (760)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsVon EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNoch keine Bewertungen

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Von EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Bewertung: 4.5 von 5 Sternen4.5/5 (5)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookVon EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookBewertung: 5 von 5 Sternen5/5 (4)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeVon EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeBewertung: 4 von 5 Sternen4/5 (21)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCVon EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCBewertung: 5 von 5 Sternen5/5 (1)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsVon EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsBewertung: 5 von 5 Sternen5/5 (1)

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetVon EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetBewertung: 4.5 von 5 Sternen4.5/5 (14)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessVon EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessBewertung: 4.5 von 5 Sternen4.5/5 (28)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceVon EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceBewertung: 4 von 5 Sternen4/5 (1)

- Beyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!Von EverandBeyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!Bewertung: 4.5 von 5 Sternen4.5/5 (8)

- Project Control Methods and Best Practices: Achieving Project SuccessVon EverandProject Control Methods and Best Practices: Achieving Project SuccessNoch keine Bewertungen

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyVon EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyNoch keine Bewertungen

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Von EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Bewertung: 4 von 5 Sternen4/5 (33)

- Small Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessVon EverandSmall Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessNoch keine Bewertungen

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsVon EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsBewertung: 4 von 5 Sternen4/5 (7)

- Contract Negotiation Handbook: Getting the Most Out of Commercial DealsVon EverandContract Negotiation Handbook: Getting the Most Out of Commercial DealsBewertung: 4.5 von 5 Sternen4.5/5 (2)

- Financial Accounting For Dummies: 2nd EditionVon EverandFinancial Accounting For Dummies: 2nd EditionBewertung: 5 von 5 Sternen5/5 (10)

- Your Amazing Itty Bitty(R) Personal Bookkeeping BookVon EverandYour Amazing Itty Bitty(R) Personal Bookkeeping BookNoch keine Bewertungen