Das könnte Ihnen auch gefallen

- Reaching Zero with Renewables: Biojet FuelsVon EverandReaching Zero with Renewables: Biojet FuelsNoch keine Bewertungen

- PP London Sumatra Indonesia: Equity ResearchDokument6 SeitenPP London Sumatra Indonesia: Equity Researchkrisyanto krisyantoNoch keine Bewertungen

- (Andy Maslen) 100 Great Copywriting Ideas From LeDokument6 Seiten(Andy Maslen) 100 Great Copywriting Ideas From LeRio PrihantoNoch keine Bewertungen

- CMP 69 Rating BUY Target 94 Upside 35%: Key Takeaways: Headwinds PersistDokument5 SeitenCMP 69 Rating BUY Target 94 Upside 35%: Key Takeaways: Headwinds PersistVikrant SadanaNoch keine Bewertungen

- Ki Adro 20190305Dokument6 SeitenKi Adro 20190305krisyanto krisyantoNoch keine Bewertungen

- CMP: INR2,022 TP: INR2,636 (+30%) Stellar Growth, RM Exerts Pressure On MarginDokument10 SeitenCMP: INR2,022 TP: INR2,636 (+30%) Stellar Growth, RM Exerts Pressure On MarginPoonam AggarwalNoch keine Bewertungen

- Vinati Organics LTD: Growth To Pick-Up..Dokument5 SeitenVinati Organics LTD: Growth To Pick-Up..Bhaveek OstwalNoch keine Bewertungen

- Balkrishna Industries: Fair Value Range (INR) 157 170Dokument4 SeitenBalkrishna Industries: Fair Value Range (INR) 157 170Varun KumarNoch keine Bewertungen

- FMCG 20101112 RelgareDokument6 SeitenFMCG 20101112 RelgaremittleNoch keine Bewertungen

- Music BroadcastDokument12 SeitenMusic BroadcastSBNoch keine Bewertungen

- Aurobindo: Weak QuarterDokument8 SeitenAurobindo: Weak QuarterjaimaaganNoch keine Bewertungen

- SpritzerDokument14 SeitenSpritzerLucyChan100% (1)

- Thai Union Food 2010-09Dokument6 SeitenThai Union Food 2010-09Tuck KhoonNoch keine Bewertungen

- Bangkok Chain Hospital: A New Lease of LifeDokument11 SeitenBangkok Chain Hospital: A New Lease of LifebodaiNoch keine Bewertungen

- Weak El Niño Strengthens Chicken Price: UpdateDokument9 SeitenWeak El Niño Strengthens Chicken Price: UpdateekidenNoch keine Bewertungen

- PTBA - Production-Costs-Erode-Profits - 20191104 - NHKS - Company - Report - English 2019Dokument7 SeitenPTBA - Production-Costs-Erode-Profits - 20191104 - NHKS - Company - Report - English 2019yasinta faridaNoch keine Bewertungen

- Ipot DSNG q321Dokument6 SeitenIpot DSNG q321jijokojawaNoch keine Bewertungen

- Company Report - IMPACT - E - 20180219081453Dokument8 SeitenCompany Report - IMPACT - E - 20180219081453bodaiNoch keine Bewertungen

- Deepak Nitrite - Initiation Report Asit Mehta Jan 2017Dokument20 SeitenDeepak Nitrite - Initiation Report Asit Mehta Jan 2017divya chawlaNoch keine Bewertungen

- FOCUS - Indofood Sukses Makmur: Saved by The GreenDokument10 SeitenFOCUS - Indofood Sukses Makmur: Saved by The GreenriskaNoch keine Bewertungen

- Trader's Daily DigestDokument12 SeitenTrader's Daily DigestSudheera IndrajithNoch keine Bewertungen

- AIA Requirement - Intrinsic Value - Index & Non Index Sept. 2017Dokument3 SeitenAIA Requirement - Intrinsic Value - Index & Non Index Sept. 2017Paul Michael AngeloNoch keine Bewertungen

- IME Echnoplast TD: P R - 100 T R .128 BUYDokument9 SeitenIME Echnoplast TD: P R - 100 T R .128 BUYsaran21Noch keine Bewertungen

- The Erawan Group: Book Now, Good Price GuaranteedDokument10 SeitenThe Erawan Group: Book Now, Good Price GuaranteedbodaiNoch keine Bewertungen

- Sun Pharma: CMP: INR574 TP: INR675 (+18%)Dokument10 SeitenSun Pharma: CMP: INR574 TP: INR675 (+18%)rishab agarwalNoch keine Bewertungen

- Ciptadana Sekuritas PTPP - Lower TP Post Weak ResultsDokument6 SeitenCiptadana Sekuritas PTPP - Lower TP Post Weak ResultsKPH BaliNoch keine Bewertungen

- Ciptadana Sekuritas AALI - 1H20 Earnings Beat ExpectationDokument6 SeitenCiptadana Sekuritas AALI - 1H20 Earnings Beat ExpectationHamba AllahNoch keine Bewertungen

- Institutional Equities: Deepak Nitrite LTDDokument6 SeitenInstitutional Equities: Deepak Nitrite LTD4nagNoch keine Bewertungen

- Jasa Marga: Equity ResearchDokument7 SeitenJasa Marga: Equity ResearchKhorbina SiregarNoch keine Bewertungen

- Vinati Organics (VO) : Under PerformerDokument4 SeitenVinati Organics (VO) : Under PerformerBhaveek OstwalNoch keine Bewertungen

- TPMA - All The Right MovesDokument4 SeitenTPMA - All The Right MovesanekalogamkonstruksiNoch keine Bewertungen

- 2QFY19 Aarti Industries ConcallDokument3 Seiten2QFY19 Aarti Industries ConcallResearch AnalystNoch keine Bewertungen

- Aditya Birla Capital: CMP: INR160 TP: INR215 (+34%) BuyDokument10 SeitenAditya Birla Capital: CMP: INR160 TP: INR215 (+34%) BuyShrishail ChaudhariNoch keine Bewertungen

- Jyothy Laboratories LTD Accumulate: Retail Equity ResearchDokument5 SeitenJyothy Laboratories LTD Accumulate: Retail Equity Researchkishor_warthi85Noch keine Bewertungen

- Hau Giang Pharma: Taisho Is Helping DHG To Boost Its CapabilitiesDokument15 SeitenHau Giang Pharma: Taisho Is Helping DHG To Boost Its CapabilitiesNgo TungNoch keine Bewertungen

- Target Price: R273.68: Recommendation: SellDokument5 SeitenTarget Price: R273.68: Recommendation: Sellkatemac2009Noch keine Bewertungen

- Ciptadana Sekuritas KINO - Key Takeaways From MeetingDokument3 SeitenCiptadana Sekuritas KINO - Key Takeaways From Meetingbudi handokoNoch keine Bewertungen

- Reliance IndustriesDokument12 SeitenReliance IndustriesMehul ShahNoch keine Bewertungen

- Systematix - Asahi Songwon - Errclub - Decent Performance, Back To NormalcyDokument6 SeitenSystematix - Asahi Songwon - Errclub - Decent Performance, Back To NormalcyshahavNoch keine Bewertungen

- Investor Digest 23 Oktober 2019Dokument10 SeitenInvestor Digest 23 Oktober 2019Rising PKN STANNoch keine Bewertungen

- Ciptadana Sekuritas SILO - Results Update FY18 - Healthy Operations To Support Long Term GrowthDokument9 SeitenCiptadana Sekuritas SILO - Results Update FY18 - Healthy Operations To Support Long Term GrowthKPH BaliNoch keine Bewertungen

- Coromandel Q1 Result UpdateDokument8 SeitenCoromandel Q1 Result UpdateshrikantbodkeNoch keine Bewertungen

- Asahi Songwon Colors - 3QFY18 RU - 15-02-2018 - SystematixDokument6 SeitenAsahi Songwon Colors - 3QFY18 RU - 15-02-2018 - SystematixshahavNoch keine Bewertungen

- Korea Investment & Sekuritas Indonesia CPIN - The Resilient IntegratorDokument8 SeitenKorea Investment & Sekuritas Indonesia CPIN - The Resilient Integratorgo joNoch keine Bewertungen

- Ciptadana - PT. Astra Agro Lestari TBK AALI - CPO Price Rally Boosts EarningsDokument7 SeitenCiptadana - PT. Astra Agro Lestari TBK AALI - CPO Price Rally Boosts EarningsWira AnindyagunaNoch keine Bewertungen

- RFM 012511Dokument2 SeitenRFM 012511norman_go_1Noch keine Bewertungen

- StarCement Q3FY24ResultReview8Feb24 ResearchDokument9 SeitenStarCement Q3FY24ResultReview8Feb24 Researchvarunkul2337Noch keine Bewertungen

- ICBP PD Upgrade 230511 182209Dokument7 SeitenICBP PD Upgrade 230511 182209michael gorbyNoch keine Bewertungen

- Pcomp Up On Gov't Stimulus Programs: Week in ReviewDokument2 SeitenPcomp Up On Gov't Stimulus Programs: Week in ReviewJervie GacutanNoch keine Bewertungen

- AIA Engineering LTD: Q3FY18 Result UpdateDokument6 SeitenAIA Engineering LTD: Q3FY18 Result Updatesaran21Noch keine Bewertungen

- Unaudited Financial Results Half-Year Ended September 30, 2016Dokument15 SeitenUnaudited Financial Results Half-Year Ended September 30, 2016Puja BhallaNoch keine Bewertungen

- Unaudited Financial Results Half-Year Ended September 30, 2016Dokument15 SeitenUnaudited Financial Results Half-Year Ended September 30, 2016Puja BhallaNoch keine Bewertungen

- 28162192019882apex IC Report PDFDokument9 Seiten28162192019882apex IC Report PDFAshutosh GuptaNoch keine Bewertungen

- TA Securities - Hartalega Holdings Berhad - Making Progress - 13-09-2016Dokument4 SeitenTA Securities - Hartalega Holdings Berhad - Making Progress - 13-09-2016sumathyNoch keine Bewertungen

- Shree Cement: Good Run Limits Upside Downgrade To NeutralDokument14 SeitenShree Cement: Good Run Limits Upside Downgrade To NeutralHardik ShahNoch keine Bewertungen

- KRBL LTD: Q3FY18: Flattish Domestic Performance Due To GST, Iran Resumes ImportsDokument4 SeitenKRBL LTD: Q3FY18: Flattish Domestic Performance Due To GST, Iran Resumes Importssaran21Noch keine Bewertungen

- Stylam IDBI Capital 200516Dokument20 SeitenStylam IDBI Capital 200516Vikas AggarwalNoch keine Bewertungen

- FinolexIndustries Q3FY22ResultReview27Jan22 ResearchDokument10 SeitenFinolexIndustries Q3FY22ResultReview27Jan22 ResearchBISWAJIT DUSADHNoch keine Bewertungen

- Weak Domestic Sales Retail Sales in Line With Expectation: Petrolimex (PLX) Earnings FlashDokument5 SeitenWeak Domestic Sales Retail Sales in Line With Expectation: Petrolimex (PLX) Earnings FlashTung NgoNoch keine Bewertungen

- CCL Products (India) LTD.: Result Update MAY 30, 2019Dokument6 SeitenCCL Products (India) LTD.: Result Update MAY 30, 2019Clandestine AspirantNoch keine Bewertungen

- Mark-To-Actual Revision of Lower Provision, But Headwind Trend RemainsDokument11 SeitenMark-To-Actual Revision of Lower Provision, But Headwind Trend RemainsbodaiNoch keine Bewertungen

- Company Report - IMPACT - E - 20180219081453Dokument8 SeitenCompany Report - IMPACT - E - 20180219081453bodaiNoch keine Bewertungen

- Features: Tracking TechnicalDokument3 SeitenFeatures: Tracking TechnicalbodaiNoch keine Bewertungen

- Sawasdee SET: S-T Retracement, Opportunity To BuyDokument14 SeitenSawasdee SET: S-T Retracement, Opportunity To BuybodaiNoch keine Bewertungen

- Sawasdee: Support: 1575, 1570 Resistance: 1585. 1590 Market StrategyDokument10 SeitenSawasdee: Support: 1575, 1570 Resistance: 1585. 1590 Market StrategybodaiNoch keine Bewertungen

- Time Will PassDokument43 SeitenTime Will PassbodaiNoch keine Bewertungen

- Bangkok Chain Hospital: A New Lease of LifeDokument11 SeitenBangkok Chain Hospital: A New Lease of LifebodaiNoch keine Bewertungen

- Through The Looking Glass #17 - Dream International (1126 HK)Dokument12 SeitenThrough The Looking Glass #17 - Dream International (1126 HK)bodaiNoch keine Bewertungen

- The Erawan Group: Book Now, Good Price GuaranteedDokument10 SeitenThe Erawan Group: Book Now, Good Price GuaranteedbodaiNoch keine Bewertungen

- Sawasdee: Support: 1575, 1565 Resistance: 1580, 1590 MarketDokument10 SeitenSawasdee: Support: 1575, 1565 Resistance: 1580, 1590 MarketbodaiNoch keine Bewertungen

- Tracking Fundamental Momentum: The First Positive Signal in Many WeeksDokument11 SeitenTracking Fundamental Momentum: The First Positive Signal in Many WeeksbodaiNoch keine Bewertungen

- PHS Aot@tb 061615 5557Dokument7 SeitenPHS Aot@tb 061615 5557bodaiNoch keine Bewertungen

- A Leader in Industrial Waste: CT Environmental GroupDokument11 SeitenA Leader in Industrial Waste: CT Environmental GroupbodaiNoch keine Bewertungen

- Aps Irpc@tb 072315 41638Dokument4 SeitenAps Irpc@tb 072315 41638bodaiNoch keine Bewertungen

- Exercises On Hyperinflation and Cost AccountingDokument4 SeitenExercises On Hyperinflation and Cost AccountingMaan CabolesNoch keine Bewertungen

- Solution Manual For Accounting 9th Edition by Charles T Horngren Walter T Harrison JR M Suzanne OliverDokument57 SeitenSolution Manual For Accounting 9th Edition by Charles T Horngren Walter T Harrison JR M Suzanne OliverToddNovakmekfw100% (33)

- IFRS 5 Implementation GuidanceDokument18 SeitenIFRS 5 Implementation GuidanceMariana Mirela0% (1)

- Chapter 2 Separate and Consolidated FS - Date of AcquisitionDokument21 SeitenChapter 2 Separate and Consolidated FS - Date of AcquisitioneiaNoch keine Bewertungen

- SPECIALIZED FABM2 Module 05 Week 05 - Statement of Changes in EquityDokument8 SeitenSPECIALIZED FABM2 Module 05 Week 05 - Statement of Changes in Equitylams.ronaldsunigaNoch keine Bewertungen

- 3rd Assign-Group 3Dokument4 Seiten3rd Assign-Group 3Rika Noviandita100% (1)

- CA 51024 - Module 3-Various ProblemsDokument4 SeitenCA 51024 - Module 3-Various ProblemsNia BranzuelaNoch keine Bewertungen

- Chapter 03 PenDokument27 SeitenChapter 03 PenJeffreyDavidNoch keine Bewertungen

- IAS 38 - Intangible AssetsDokument8 SeitenIAS 38 - Intangible AssetsEric Agyenim-BoatengNoch keine Bewertungen

- Material 1 Partnership Formation and OpeDokument6 SeitenMaterial 1 Partnership Formation and OpeClaire BarbaNoch keine Bewertungen

- Intermediate Accounting 3 Part 1: Cash Flows Objectives of Cash Flow StatementDokument19 SeitenIntermediate Accounting 3 Part 1: Cash Flows Objectives of Cash Flow StatementAG VenturesNoch keine Bewertungen

- Less: Operating ExpensesDokument17 SeitenLess: Operating ExpensesJJ THOMPSONNoch keine Bewertungen

- Financial Statement Analysis 2020Dokument26 SeitenFinancial Statement Analysis 2020Dennis AleaNoch keine Bewertungen

- AFE5008-B Financial Accounting: The Following Information Is Also RelevantDokument2 SeitenAFE5008-B Financial Accounting: The Following Information Is Also RelevantDiana TuckerNoch keine Bewertungen

- Chapter 2 Financial ManagementDokument58 SeitenChapter 2 Financial ManagementCarstene RenggaNoch keine Bewertungen

- This Study Resource WasDokument2 SeitenThis Study Resource WasMaster Nistro0% (1)

- Alibaba IPO Financial Model WallstreetMojoDokument52 SeitenAlibaba IPO Financial Model WallstreetMojoJulian HutabaratNoch keine Bewertungen

- Detailed Lesson Plan - Fabm 1 (Second)Dokument12 SeitenDetailed Lesson Plan - Fabm 1 (Second)Maria Benna Mendiola100% (5)

- How To Read and Analyze An Income StatementDokument5 SeitenHow To Read and Analyze An Income StatementsaketNoch keine Bewertungen

- L4 - ABFA1173 POA (Lecturer)Dokument10 SeitenL4 - ABFA1173 POA (Lecturer)Tan SiewsiewNoch keine Bewertungen

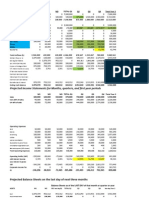

- Projected Income Statements For Months, Quarters, and First Year PeriodsDokument5 SeitenProjected Income Statements For Months, Quarters, and First Year Periodssarakhan0622Noch keine Bewertungen

- 도로설계기준, 2016Dokument332 Seiten도로설계기준, 2016suni soonNoch keine Bewertungen

- Accounting Review Week 2Dokument13 SeitenAccounting Review Week 2Janine IgdalinoNoch keine Bewertungen

- Chapter 5 Assignment Introductory Accounting Name: Nguyen Mai PhuongDokument12 SeitenChapter 5 Assignment Introductory Accounting Name: Nguyen Mai PhuongMai Phương NguyễnNoch keine Bewertungen

- Financial Ratios Case Homeowork 3Dokument17 SeitenFinancial Ratios Case Homeowork 3Edward Lu100% (1)

- Reconstitution of A Partnership Firm - Admission of A PartnerDokument65 SeitenReconstitution of A Partnership Firm - Admission of A PartnerPathan KausarNoch keine Bewertungen

- 25 Question PaperDokument4 Seiten25 Question PaperPacific Tiger0% (1)

- Chapter - 1-Accounting For InventoriesDokument40 SeitenChapter - 1-Accounting For InventoriesWonde BiruNoch keine Bewertungen

- Comprehensive Budgeting Example: © The Mcgraw-Hill Companies, Inc., 2006. All Rights ReservedDokument14 SeitenComprehensive Budgeting Example: © The Mcgraw-Hill Companies, Inc., 2006. All Rights Reservedzelalem kebedeNoch keine Bewertungen

- Financial Analysis & Planning - ICAI Study Material PDFDokument80 SeitenFinancial Analysis & Planning - ICAI Study Material PDFShivani GuptaNoch keine Bewertungen