Das könnte Ihnen auch gefallen

- IL&FS Letter To LIC Chairman 1 Oct 2018Dokument3 SeitenIL&FS Letter To LIC Chairman 1 Oct 2018Moneylife FoundationNoch keine Bewertungen

- IL&FS Letter To SBI Chairman 1 Oct 2018Dokument3 SeitenIL&FS Letter To SBI Chairman 1 Oct 2018Moneylife FoundationNoch keine Bewertungen

- Rail Ministry Reply On Moneylife Foundation Memorandum-2018!05!12Dokument10 SeitenRail Ministry Reply On Moneylife Foundation Memorandum-2018!05!12Moneylife FoundationNoch keine Bewertungen

- IRDAI Memorandum Jeevan Saral Final DraftDokument4 SeitenIRDAI Memorandum Jeevan Saral Final DraftMoneylife FoundationNoch keine Bewertungen

- NSE List of Expelled Brokers 19 Oct 2021Dokument7 SeitenNSE List of Expelled Brokers 19 Oct 2021Moneylife FoundationNoch keine Bewertungen

- Memorandum To ECIDokument6 SeitenMemorandum To ECIINC India100% (1)

- BMC JE Result PDFDokument850 SeitenBMC JE Result PDFsumeet andureNoch keine Bewertungen

- WP (C) 259of2017Dokument119 SeitenWP (C) 259of2017mnscorpsNoch keine Bewertungen

- BB0019-IncomeTax Valuation PerquisitesDokument314 SeitenBB0019-IncomeTax Valuation PerquisitesMohammed Abu ObaidahNoch keine Bewertungen

- Water Security STD 9th Textbook by Techy BagDokument86 SeitenWater Security STD 9th Textbook by Techy Bagpooja TiwariNoch keine Bewertungen

- Syllabus For PS Group BDokument6 SeitenSyllabus For PS Group Brakesh kumarNoch keine Bewertungen

- CDR Master Circular 2012Dokument72 SeitenCDR Master Circular 2012Gaurav KukrejaNoch keine Bewertungen

- Agreement - HindiDokument3 SeitenAgreement - HindidhruvdiatmNoch keine Bewertungen

- Memorandum Submitted To ECI - Amit Shah AffidavitDokument5 SeitenMemorandum Submitted To ECI - Amit Shah AffidavitINC India100% (1)

- 30-Dec-2020-Memorandum To Sebi and Justice BN AgrawalDokument17 Seiten30-Dec-2020-Memorandum To Sebi and Justice BN AgrawalMoneylife FoundationNoch keine Bewertungen

- CHAPTER TV-Maior Events in The Indian Stock Market: 4.1 ObjectiveDokument13 SeitenCHAPTER TV-Maior Events in The Indian Stock Market: 4.1 ObjectiveAnkit SinghNoch keine Bewertungen

- RBI Issues SARFAESI Act 2002 Guidelines and Directions As Amendment Upto 30th June 2015Dokument26 SeitenRBI Issues SARFAESI Act 2002 Guidelines and Directions As Amendment Upto 30th June 2015Kapil Dev SaggiNoch keine Bewertungen

- 10 Main Features of Indian Tax StructureDokument16 Seiten10 Main Features of Indian Tax Structurerahul chauhanNoch keine Bewertungen

- MSME HelpDokument10 SeitenMSME HelpAjay MehtaNoch keine Bewertungen

- Slump Sale and Slump Exchange ExplainedDokument36 SeitenSlump Sale and Slump Exchange ExplainedVicky Murthy0% (1)

- Phadke Complaint To RBIDokument6 SeitenPhadke Complaint To RBIMoneylife FoundationNoch keine Bewertungen

- 45 NBFCDokument109 Seiten45 NBFCViji RangaNoch keine Bewertungen

- ServletDokument498 SeitenServletankit-malhotra-3456100% (1)

- Handbook On Recovery of Arrears of Revenue PDFDokument196 SeitenHandbook On Recovery of Arrears of Revenue PDFRajula Gurva Reddy67% (3)

- Note On GST Input Tax Credit CA Yashwant KasarDokument32 SeitenNote On GST Input Tax Credit CA Yashwant KasarGiri SukumarNoch keine Bewertungen

- RTI Sample Application FormDokument1 SeiteRTI Sample Application FormpiccoloashNoch keine Bewertungen

- Combined Annexures v1Dokument31 SeitenCombined Annexures v1Vaibhav Badjatya100% (2)

- DisciplineDokument92 SeitenDisciplineaipeup4odisha odishaNoch keine Bewertungen

- Judgement of The Armed Forces Appellate Tribunal Pertaining To An Officer Involved in Kargil OperationsDokument12 SeitenJudgement of The Armed Forces Appellate Tribunal Pertaining To An Officer Involved in Kargil OperationsSampath BulusuNoch keine Bewertungen

- Handbook of RTIDokument61 SeitenHandbook of RTIAniket PrakashNoch keine Bewertungen

- Allotment of AgentsDokument4 SeitenAllotment of AgentstsrajanNoch keine Bewertungen

- UFCE FEDAI FormatDokument2 SeitenUFCE FEDAI FormatPRAVALLIKA NNoch keine Bewertungen

- Cash Reserve RatioDokument6 SeitenCash Reserve RatioAmitesh RoyNoch keine Bewertungen

- Home Loan - Master BCC BR 106 380Dokument158 SeitenHome Loan - Master BCC BR 106 380binalamitNoch keine Bewertungen

- Pradhanmantri Jeevan Jyoti Bima YojnaDokument3 SeitenPradhanmantri Jeevan Jyoti Bima YojnaArvind Kumar75% (4)

- CCD IssuingDokument4 SeitenCCD Issuingvandana guptaNoch keine Bewertungen

- Vikas 2018 SBLC BhubaneswarDokument320 SeitenVikas 2018 SBLC BhubaneswarTejaswiNoch keine Bewertungen

- Written Submissions (EPF Penalty Waiver)Dokument86 SeitenWritten Submissions (EPF Penalty Waiver)abhiGT40Noch keine Bewertungen

- O.A. No. 255 of 2012 Brig NK MehtaDokument93 SeitenO.A. No. 255 of 2012 Brig NK MehtaIshwer KumarNoch keine Bewertungen

- Indian Ispat submission to Commercial Tax DepartmentDokument3 SeitenIndian Ispat submission to Commercial Tax DepartmentSURANA1973100% (1)

- G.O.Ms - No. 287 Dated: 30-08-2018Dokument68 SeitenG.O.Ms - No. 287 Dated: 30-08-2018Prajoth Kumar100% (1)

- Unit-4 (Mis & E-Payment) January 10, 2023Dokument30 SeitenUnit-4 (Mis & E-Payment) January 10, 2023Dev ParmarNoch keine Bewertungen

- Agreement Format - 13032013 Sdarepo AgentsDokument17 SeitenAgreement Format - 13032013 Sdarepo AgentsIsmail MswNoch keine Bewertungen

- LFAR-Ready Reckoner Audit Report SummaryDokument13 SeitenLFAR-Ready Reckoner Audit Report SummaryJAY SHARMA100% (1)

- Civil Servant APT Rules 1973 PDFDokument8 SeitenCivil Servant APT Rules 1973 PDFbabarNoch keine Bewertungen

- LFAR Report for Bank BranchesDokument16 SeitenLFAR Report for Bank BranchesAmrit SinghaniaNoch keine Bewertungen

- The Role of SEBI in Protecting The Interests of Investors and Regulation of Financial IntermediariesDokument10 SeitenThe Role of SEBI in Protecting The Interests of Investors and Regulation of Financial IntermediariesSaurabh sarojNoch keine Bewertungen

- D RangareddyweeklyVcUploads44 PDFDokument63 SeitenD RangareddyweeklyVcUploads44 PDFtruenameNoch keine Bewertungen

- Report Writing On Road Accidents - FlattenedDokument7 SeitenReport Writing On Road Accidents - FlattenedIqbal HossainNoch keine Bewertungen

- 21 HR Manual For Union Bank Officers Min PDFDokument217 Seiten21 HR Manual For Union Bank Officers Min PDFeswar414Noch keine Bewertungen

- 9th PRC Report On A.P. EmployeesDokument2.031 Seiten9th PRC Report On A.P. Employeesnavn7678% (9)

- Court Case On Dar AppmDokument63 SeitenCourt Case On Dar AppmIndian Railways Knowledge PortalNoch keine Bewertungen

- 7.09.17 Labour RTI Congnizance 8.08Dokument5 Seiten7.09.17 Labour RTI Congnizance 8.08Shri Gopal SoniNoch keine Bewertungen

- Imp. Labour Judgments - 2010Dokument41 SeitenImp. Labour Judgments - 2010DashanandNoch keine Bewertungen

- Letter To GovernorDokument4 SeitenLetter To GovernorMoneylife FoundationNoch keine Bewertungen

- SBI Assignment 1Dokument12 SeitenSBI Assignment 1DeveshMittalNoch keine Bewertungen

- Customer Service in Service Sector BankingDokument8 SeitenCustomer Service in Service Sector BankinghirshahNoch keine Bewertungen

- Memorandum To RBI On ATM CostsDokument18 SeitenMemorandum To RBI On ATM CostsMld OnnetNoch keine Bewertungen

- STD X CH 3 Money and Credit Notes (21-22)Dokument6 SeitenSTD X CH 3 Money and Credit Notes (21-22)Dhwani ShahNoch keine Bewertungen

- Kotak MahindraDokument65 SeitenKotak MahindraNidhi Vijayvergiya100% (1)

- Bombay High Court Issues Rules For Video Conferencing For CourtsDokument14 SeitenBombay High Court Issues Rules For Video Conferencing For CourtsMoneylife FoundationNoch keine Bewertungen

- Mohan Gopal Letter2PMDokument12 SeitenMohan Gopal Letter2PMMoneylife FoundationNoch keine Bewertungen

- Report of The Fact-Finding Mission On Media's Reportage of The Ethnic Violence in ManipurDokument24 SeitenReport of The Fact-Finding Mission On Media's Reportage of The Ethnic Violence in ManipurThe WireNoch keine Bewertungen

- Bombay High Court Issues Rules For Video Conferencing For CourtsDokument14 SeitenBombay High Court Issues Rules For Video Conferencing For CourtsMoneylife FoundationNoch keine Bewertungen

- Mohan Gopal Letter2PMDokument16 SeitenMohan Gopal Letter2PMMoneylife FoundationNoch keine Bewertungen

- RBI Wilful Defaulters PSBs Annex 1 RTIDokument51 SeitenRBI Wilful Defaulters PSBs Annex 1 RTIMoneylife Foundation83% (6)

- Syndicate Bank Risk Assessment and Inspection Reports Shared by RBIDokument276 SeitenSyndicate Bank Risk Assessment and Inspection Reports Shared by RBIMoneylife Foundation100% (5)

- Syndicate Bank Risk Assessment and Inspection Reports Shared by RBIDokument276 SeitenSyndicate Bank Risk Assessment and Inspection Reports Shared by RBIMoneylife Foundation100% (5)

- Syndicate Bank Risk Assessment and Inspection Reports Shared by RBIDokument276 SeitenSyndicate Bank Risk Assessment and Inspection Reports Shared by RBIMoneylife Foundation100% (5)

- SIC Pandes OrderDokument5 SeitenSIC Pandes OrderMoneylife FoundationNoch keine Bewertungen

- City Union Bank Inspection ReportDokument114 SeitenCity Union Bank Inspection ReportMoneylife Foundation100% (1)

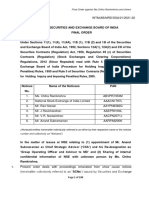

- SEBI Final Order Against Ms. Chitra Ramkrishna and OthersDokument190 SeitenSEBI Final Order Against Ms. Chitra Ramkrishna and OthersMoneylife FoundationNoch keine Bewertungen

- City Union Bank Inspection ReportDokument114 SeitenCity Union Bank Inspection ReportMoneylife Foundation100% (1)

- City Union Bank Inspection ReportDokument114 SeitenCity Union Bank Inspection ReportMoneylife Foundation100% (1)

- 30-Dec-2020-Memorandum To Sebi and Justice BN AgrawalDokument17 Seiten30-Dec-2020-Memorandum To Sebi and Justice BN AgrawalMoneylife FoundationNoch keine Bewertungen

- MLF Presentation To SEBI Mahalingam Committee 13 May 2022Dokument13 SeitenMLF Presentation To SEBI Mahalingam Committee 13 May 2022Moneylife FoundationNoch keine Bewertungen

- ANMI Sub112 Dated 29 Dec To MOF On Limitation ClauseDokument2 SeitenANMI Sub112 Dated 29 Dec To MOF On Limitation ClauseMoneylife FoundationNoch keine Bewertungen

- MLF Presentation To SEBI Mahalingam Committee 13 May 2022Dokument13 SeitenMLF Presentation To SEBI Mahalingam Committee 13 May 2022Moneylife FoundationNoch keine Bewertungen

- Joint-Representation Extension Filing TAR ITReturnsDokument7 SeitenJoint-Representation Extension Filing TAR ITReturnsMoneylife FoundationNoch keine Bewertungen

- Order For Home TestingDokument3 SeitenOrder For Home TestingMoneylife FoundationNoch keine Bewertungen

- SEBI Final Order Against Ms. Chitra Ramkrishna and OthersDokument190 SeitenSEBI Final Order Against Ms. Chitra Ramkrishna and OthersMoneylife FoundationNoch keine Bewertungen

- SEBI Final Order Against Ms. Chitra Ramkrishna and OthersDokument190 SeitenSEBI Final Order Against Ms. Chitra Ramkrishna and OthersMoneylife FoundationNoch keine Bewertungen

- Monthly Data YCEW Dec 2021Dokument4 SeitenMonthly Data YCEW Dec 2021Moneylife FoundationNoch keine Bewertungen

- Erratic and Irresponsible Approach of Finance Ministry Towards IT InfrastructureDokument10 SeitenErratic and Irresponsible Approach of Finance Ministry Towards IT InfrastructureMoneylife FoundationNoch keine Bewertungen

- Reliance Capital Limited: Vu VM of ' ('Dokument4 SeitenReliance Capital Limited: Vu VM of ' ('Moneylife Foundation100% (1)

- Letter To CJI On WritDokument2 SeitenLetter To CJI On WritMoneylife FoundationNoch keine Bewertungen

- PR DICGC AmendmentAct2021 Section18A PaymentToDepositorsOfInsuredBanksUnder AIDDokument3 SeitenPR DICGC AmendmentAct2021 Section18A PaymentToDepositorsOfInsuredBanksUnder AIDMoneylife FoundationNoch keine Bewertungen

- SC Order Northern Railways Vs Sanjay Shukla 06 Sep 2021Dokument7 SeitenSC Order Northern Railways Vs Sanjay Shukla 06 Sep 2021Moneylife FoundationNoch keine Bewertungen

- Instruction No: CustomsDokument2 SeitenInstruction No: CustomsSEAPATH DOCSNoch keine Bewertungen

- BS Bengaluru 30-01-2024Dokument20 SeitenBS Bengaluru 30-01-2024srashmiiiscNoch keine Bewertungen

- Om Changes Mca&Rfp of Tot ModelDokument25 SeitenOm Changes Mca&Rfp of Tot ModelVarun ChandraNoch keine Bewertungen

- Mongolian public housing programme leadersDokument17 SeitenMongolian public housing programme leadersБ. ПүрэвбатNoch keine Bewertungen

- Tamilnadu Govt 10% DA HIKE (35% To 45%) GO 371 24.9.2010 EnglishDokument3 SeitenTamilnadu Govt 10% DA HIKE (35% To 45%) GO 371 24.9.2010 EnglishMohankumar P KNoch keine Bewertungen

- English Annual Report 2021-22Dokument172 SeitenEnglish Annual Report 2021-22Ashish SharmaNoch keine Bewertungen

- September 2022 Current Affairs EnglishDokument90 SeitenSeptember 2022 Current Affairs EnglishVISHWAS RANANoch keine Bewertungen

- Budget Circular 2022-2023Dokument178 SeitenBudget Circular 2022-2023Daksh AgarwalNoch keine Bewertungen

- BALCO Union V Union of India 2002Dokument36 SeitenBALCO Union V Union of India 2002Manisha Singh0% (1)

- CCL1Dokument2 SeitenCCL1rituneshmNoch keine Bewertungen

- AnnualReport2008 09Dokument242 SeitenAnnualReport2008 09Ninad PaiNoch keine Bewertungen

- Aao Syllabus PDFDokument48 SeitenAao Syllabus PDFrijin00c100% (1)

- VST Industries Annual Report 2017-18 HighlightsDokument110 SeitenVST Industries Annual Report 2017-18 HighlightsSatish RNoch keine Bewertungen

- Allsbe PDFDokument338 SeitenAllsbe PDFAbhishek KumarNoch keine Bewertungen

- Dual Family Pension for Armed Forces PersonnelDokument9 SeitenDual Family Pension for Armed Forces PersonnelKumaravel RajamaniNoch keine Bewertungen

- Public Sector Administration QuestionsDokument42 SeitenPublic Sector Administration QuestionsSyed Muazzam Ali Naqvi100% (2)

- GENERAL STUDIES PRACTICE QUESTIONSDokument23 SeitenGENERAL STUDIES PRACTICE QUESTIONSRamesh KumarNoch keine Bewertungen

- Budget ExecutionDokument23 SeitenBudget ExecutionDesiRianaPrasetyaNoch keine Bewertungen

- FINANCE (Allowances) DEPARTMENT G.O.Ms - No.232, Dated 27 April 2020Dokument3 SeitenFINANCE (Allowances) DEPARTMENT G.O.Ms - No.232, Dated 27 April 2020Gowtham RajNoch keine Bewertungen

- List of Organisation Using CPPP EprocurementDokument28 SeitenList of Organisation Using CPPP EprocurementnitinNoch keine Bewertungen

- Budget PPT Group 6 (1) - 1Dokument17 SeitenBudget PPT Group 6 (1) - 17336 Vikas MouryaNoch keine Bewertungen

- Financial Regulatory Bodies of IndiaDokument22 SeitenFinancial Regulatory Bodies of IndiaAli WarsiNoch keine Bewertungen

- 1 Banking Awareness MCQs by K KundanDokument28 Seiten1 Banking Awareness MCQs by K KundanNarendra GuptaNoch keine Bewertungen

- The Masterbuilder - March 2012 - Formwork and Tunneling SpecialDokument241 SeitenThe Masterbuilder - March 2012 - Formwork and Tunneling SpecialChaitanya Raj GoyalNoch keine Bewertungen

- Rajiv Awas Yojana GuidelinesDokument24 SeitenRajiv Awas Yojana GuidelinesSherine David SANoch keine Bewertungen

- Mission Vatsalya Dated 05 July 2022Dokument78 SeitenMission Vatsalya Dated 05 July 2022KkrkumarNoch keine Bewertungen

- AU179 - Divestment ListDokument9 SeitenAU179 - Divestment ListPiyush Ashokchand ChopdaNoch keine Bewertungen

- Mid Monthly December 2015 Exampunditfinalversionpdfofmidmonthlydecember2015Dokument24 SeitenMid Monthly December 2015 Exampunditfinalversionpdfofmidmonthlydecember2015Sahil GuptaNoch keine Bewertungen

- TN govt increases DA to 295Dokument3 SeitenTN govt increases DA to 295NAZIR AHAMEDNoch keine Bewertungen

- IFSWF Delegate ListDokument3 SeitenIFSWF Delegate ListCarlos JesenaNoch keine Bewertungen