Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Financial Statemen TsDokument1 SeiteFinancial Statemen TsJoel JimenezNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Three Main Types of AnglesDokument4 SeitenThree Main Types of AnglesJoel JimenezNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hi PrelimDokument5 SeitenHi PrelimJoel JimenezNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- Mountain DesertsDokument2 SeitenMountain DesertsTroisNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Revised Withholding Tax TablesDokument1 SeiteRevised Withholding Tax TablesJonasAblangNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Amita Legaspi: /NB, GMA NewsDokument1 SeiteAmita Legaspi: /NB, GMA NewsJoel JimenezNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Psychology: Psychology Is The Study ofDokument2 SeitenPsychology: Psychology Is The Study ofJoel JimenezNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Transition Guide to PFRS for SMEsDokument1 SeiteTransition Guide to PFRS for SMEsJoel JimenezNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Value Is The Price That Would Be Received To Sell An Asset or Paid To Transfer A Liability in An Orderly Transaction Between Market Participants at The Measurement DateDokument1 SeiteValue Is The Price That Would Be Received To Sell An Asset or Paid To Transfer A Liability in An Orderly Transaction Between Market Participants at The Measurement DateJoel JimenezNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- Takehome atDokument4 SeitenTakehome atJoel JimenezNoch keine Bewertungen

- Chapter 7 - Chromosomal Basis of Inheritance - 3Dokument35 SeitenChapter 7 - Chromosomal Basis of Inheritance - 3jhela18Noch keine Bewertungen

- Commercial Lease Agreement 2Dokument7 SeitenCommercial Lease Agreement 2Joel JimenezNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- ChaptDokument4 SeitenChaptJoel JimenezNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Tax RemDokument8 SeitenTax RemJoel JimenezNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- CkmalsDokument18 SeitenCkmalsJoel JimenezNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Nite AllDokument2 SeitenNite AllJoel JimenezNoch keine Bewertungen

- CHAfs RDokument18 SeitenCHAfs RJoel JimenezNoch keine Bewertungen

- Financial Statements PresentationDokument2 SeitenFinancial Statements PresentationJoel JimenezNoch keine Bewertungen

- Models of Corporate Governance: Anglo-US, Japanese, and German ModelsDokument6 SeitenModels of Corporate Governance: Anglo-US, Japanese, and German ModelsJoel JimenezNoch keine Bewertungen

- ChaptDokument4 SeitenChaptJoel JimenezNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- UeDokument10 SeitenUeJoel JimenezNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- BIerwerDokument11 SeitenBIerwerJoel JimenezNoch keine Bewertungen

- Revised Withholding Tax TablesDokument1 SeiteRevised Withholding Tax TablesJonasAblangNoch keine Bewertungen

- Models of Corporate Governance: Anglo-US, Japanese, and German ModelsDokument6 SeitenModels of Corporate Governance: Anglo-US, Japanese, and German ModelsJoel JimenezNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- CKDokument1 SeiteCKJoel JimenezNoch keine Bewertungen

- Board of Directors Corporations: Interlocking Directorate Refers To The Practice of Members of A CorporateDokument2 SeitenBoard of Directors Corporations: Interlocking Directorate Refers To The Practice of Members of A CorporateJoel JimenezNoch keine Bewertungen

- Bi 2Dokument12 SeitenBi 2Joel JimenezNoch keine Bewertungen

- Glaciers, Desert and WindDokument63 SeitenGlaciers, Desert and WindJoel JimenezNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Statement of The ProblemDokument11 SeitenStatement of The ProblemJoel JimenezNoch keine Bewertungen

- Aegon Life Insurance Marketing Strategy AnalysisDokument22 SeitenAegon Life Insurance Marketing Strategy AnalysissalmanNoch keine Bewertungen

- Dryousry Hospitality Consulting: Hotel Pre Opening RoadmapDokument35 SeitenDryousry Hospitality Consulting: Hotel Pre Opening RoadmapTix VirakNoch keine Bewertungen

- Creating Custom Context AttributesDokument19 SeitenCreating Custom Context AttributesahosainyNoch keine Bewertungen

- RolexDokument17 SeitenRolexAnkush AnguralNoch keine Bewertungen

- Steid ProfileDokument95 SeitenSteid Profileapi-3799305100% (11)

- Sale of Conjugal Property Without Liquidation ValidDokument2 SeitenSale of Conjugal Property Without Liquidation ValidJoan MagasoNoch keine Bewertungen

- Sales Manager Solar Engineer in Dallas FT Worth TX Resume John JohnsonDokument2 SeitenSales Manager Solar Engineer in Dallas FT Worth TX Resume John JohnsonJohnJohnsonNoch keine Bewertungen

- Building and Sustaining Relationships in Retailing: Retail Management: A Strategic ApproachDokument34 SeitenBuilding and Sustaining Relationships in Retailing: Retail Management: A Strategic ApproachebustosfNoch keine Bewertungen

- Sample Deed of Absolute SaleDokument3 SeitenSample Deed of Absolute SaleAnna NavaNoch keine Bewertungen

- Gallardo's Goes To Mexico (Repaired)Dokument20 SeitenGallardo's Goes To Mexico (Repaired)Soumya Siddharth Rout100% (3)

- Retail Shop ManagementDokument18 SeitenRetail Shop Managementkowsalya18Noch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- NIKE Presentation Slide EditDokument24 SeitenNIKE Presentation Slide EditAtiQah NOtyhNoch keine Bewertungen

- GAP IncDokument109 SeitenGAP Incgcdint3100% (1)

- Assignment On Hair SalonDokument14 SeitenAssignment On Hair SalonmanuNoch keine Bewertungen

- Joshua Kennon What Is A FranchiseDokument6 SeitenJoshua Kennon What Is A FranchiseNico A. Cotzias Jr.Noch keine Bewertungen

- Analisis Industri Dan PersainganDokument16 SeitenAnalisis Industri Dan PersainganJaka WenjaniNoch keine Bewertungen

- The Law of ContractDokument8 SeitenThe Law of ContractVivek RuparelNoch keine Bewertungen

- Lums Leveragingthestyloshoesexperience 130119101835 Phpapp01Dokument20 SeitenLums Leveragingthestyloshoesexperience 130119101835 Phpapp01Bushra UmarNoch keine Bewertungen

- Mangorrific: A Nutritious Mango Milktea ShakeDokument14 SeitenMangorrific: A Nutritious Mango Milktea ShakeErvin Evangelista100% (1)

- Interbrand Design Forum Newsletter: How Design Drives Retail Brand ValueDokument4 SeitenInterbrand Design Forum Newsletter: How Design Drives Retail Brand ValueBeth LingNoch keine Bewertungen

- Impact of Salesperson Behavior on Customer Perceived Service QualityDokument98 SeitenImpact of Salesperson Behavior on Customer Perceived Service QualityJehan Marie GiananNoch keine Bewertungen

- ADF Foods Limited - Report - 17th June 2008 - DhananjayanDokument2 SeitenADF Foods Limited - Report - 17th June 2008 - Dhananjayanapi-3702531Noch keine Bewertungen

- Domino's Pizza History, Menu, Advertising & Pricing StrategiesDokument15 SeitenDomino's Pizza History, Menu, Advertising & Pricing StrategiesEe ZatNoch keine Bewertungen

- Curriculum and syllabus guide for commerce classes 11 and 12Dokument6 SeitenCurriculum and syllabus guide for commerce classes 11 and 12Jay Karta100% (1)

- Ammended Picfare Distributor Agreement January, 2019docxDokument20 SeitenAmmended Picfare Distributor Agreement January, 2019docxlegaloffice picfare.comNoch keine Bewertungen

- 0.4-Short Term BudgetingDokument49 Seiten0.4-Short Term BudgetingMatsuno Chifuyu100% (1)

- Dissolution and winding up of partnership between Serra and MotaDokument3 SeitenDissolution and winding up of partnership between Serra and MotaNLainie OmarNoch keine Bewertungen

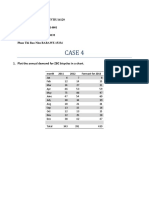

- Case 4: Luyen Ngoc Do Quyen BTFTIU14129 Ngo Khanh Duy BTARIU14601 Pham Gia Huy BTFTIU14132 Phan Thi Bao Nhu BABAWE 15334Dokument4 SeitenCase 4: Luyen Ngoc Do Quyen BTFTIU14129 Ngo Khanh Duy BTARIU14601 Pham Gia Huy BTFTIU14132 Phan Thi Bao Nhu BABAWE 15334HuynhGiangNoch keine Bewertungen

- Business PlanDokument20 SeitenBusiness PlanRoxenne Traya100% (1)

- Invty EstimationDokument6 SeitenInvty EstimationdmiahalNoch keine Bewertungen

- The Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeVon EverandThe Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeBewertung: 4.5 von 5 Sternen4.5/5 (85)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Von EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Bewertung: 4.5 von 5 Sternen4.5/5 (12)

- The Science of Positive Focus: Live Seminar: Master Keys for Reaching Your Next LevelVon EverandThe Science of Positive Focus: Live Seminar: Master Keys for Reaching Your Next LevelBewertung: 5 von 5 Sternen5/5 (51)

- Summary: Who Not How: The Formula to Achieve Bigger Goals Through Accelerating Teamwork by Dan Sullivan & Dr. Benjamin Hardy:Von EverandSummary: Who Not How: The Formula to Achieve Bigger Goals Through Accelerating Teamwork by Dan Sullivan & Dr. Benjamin Hardy:Bewertung: 5 von 5 Sternen5/5 (2)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindVon EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindBewertung: 5 von 5 Sternen5/5 (231)

- Anything You Want: 40 lessons for a new kind of entrepreneurVon EverandAnything You Want: 40 lessons for a new kind of entrepreneurBewertung: 5 von 5 Sternen5/5 (46)

- Summary of The Subtle Art of Not Giving A F*ck: A Counterintuitive Approach to Living a Good Life by Mark Manson: Key Takeaways, Summary & Analysis IncludedVon EverandSummary of The Subtle Art of Not Giving A F*ck: A Counterintuitive Approach to Living a Good Life by Mark Manson: Key Takeaways, Summary & Analysis IncludedBewertung: 4.5 von 5 Sternen4.5/5 (38)

- 12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurVon Everand12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurBewertung: 4 von 5 Sternen4/5 (2)

- ChatGPT Side Hustles 2024 - Unlock the Digital Goldmine and Get AI Working for You Fast with More Than 85 Side Hustle Ideas to Boost Passive Income, Create New Cash Flow, and Get Ahead of the CurveVon EverandChatGPT Side Hustles 2024 - Unlock the Digital Goldmine and Get AI Working for You Fast with More Than 85 Side Hustle Ideas to Boost Passive Income, Create New Cash Flow, and Get Ahead of the CurveNoch keine Bewertungen