Das könnte Ihnen auch gefallen

- Business Policy FormulationDokument21 SeitenBusiness Policy FormulationWachee Mbugua50% (2)

- The Way To Sell: Powered byDokument25 SeitenThe Way To Sell: Powered bysagarsononiNoch keine Bewertungen

- Level 1:: Advanced Financial Modeler (Afm)Dokument23 SeitenLevel 1:: Advanced Financial Modeler (Afm)munaftNoch keine Bewertungen

- LAS IN ENTREPRENEURSHIP WEEK 4Dokument5 SeitenLAS IN ENTREPRENEURSHIP WEEK 4IMELDA CORONACIONNoch keine Bewertungen

- George F Kennan and The Birth of Containment The Greek Test CaseDokument17 SeitenGeorge F Kennan and The Birth of Containment The Greek Test CaseEllinikos Emfilios100% (1)

- Analyzing Evidence of College Readiness: A Tri-Level Empirical & Conceptual FrameworkDokument66 SeitenAnalyzing Evidence of College Readiness: A Tri-Level Empirical & Conceptual FrameworkJinky RegonayNoch keine Bewertungen

- Revolute-Input Delta Robot DescriptionDokument43 SeitenRevolute-Input Delta Robot DescriptionIbrahim EssamNoch keine Bewertungen

- Ashforth & Mael 1989 Social Identity Theory and The OrganizationDokument21 SeitenAshforth & Mael 1989 Social Identity Theory and The Organizationhoorie100% (1)

- Lpgas: Northwest Europe Daily Assessments $/MTDokument5 SeitenLpgas: Northwest Europe Daily Assessments $/MTMilkiss SweetNoch keine Bewertungen

- Kolom Inventory CardDokument1 SeiteKolom Inventory CardargarinirizqiayuNoch keine Bewertungen

- Prices Are Starting From: Quantum of The SeasDokument1 SeitePrices Are Starting From: Quantum of The SeasoverpopulationNoch keine Bewertungen

- Ceka Cahaya Kalbar TBK.: Company Report: January 2012Dokument3 SeitenCeka Cahaya Kalbar TBK.: Company Report: January 2012dennyaikiNoch keine Bewertungen

- Lpgas: Northwest Europe Daily Assessments $/MTDokument5 SeitenLpgas: Northwest Europe Daily Assessments $/MTMilkiss SweetNoch keine Bewertungen

- Faiq Buner ExpencesDokument108 SeitenFaiq Buner ExpencesPalwasha GulNoch keine Bewertungen

- Summary Report POLDokument5 SeitenSummary Report POLFeroz GullNoch keine Bewertungen

- Rekapitulasi Anggaran Pembiayaan Dan Oprasional: TotalDokument23 SeitenRekapitulasi Anggaran Pembiayaan Dan Oprasional: Totalogi syaNoch keine Bewertungen

- Lpgas: Northwest Europe Daily Assessments $/MTDokument6 SeitenLpgas: Northwest Europe Daily Assessments $/MTMilkiss SweetNoch keine Bewertungen

- Chart Availability ListDokument42 SeitenChart Availability ListKunal SinghNoch keine Bewertungen

- Thawe Marine Pte LTD Soa Pt. Gemilang Bina Lintas Tirta - UsdDokument2 SeitenThawe Marine Pte LTD Soa Pt. Gemilang Bina Lintas Tirta - UsdBrevetAB Kartini2018Noch keine Bewertungen

- Document Planning Schedule With Plan Bar Rev DDokument22 SeitenDocument Planning Schedule With Plan Bar Rev DRamesh SelvarajNoch keine Bewertungen

- Daily Expense Sheet Date Details Parts Sublet Fair Entertainment Travelling Expother ExpDokument7 SeitenDaily Expense Sheet Date Details Parts Sublet Fair Entertainment Travelling Expother ExpMir Zohaib Raza TalpurNoch keine Bewertungen

- Note PDFDokument1 SeiteNote PDFrezkyfpNoch keine Bewertungen

- Jawab A DateDokument8 SeitenJawab A Date26Rizqy Fathur RahmanNoch keine Bewertungen

- Expenses and income statement for apartment complexDokument10 SeitenExpenses and income statement for apartment complexPriyadarshini KamathNoch keine Bewertungen

- H&M Inspection ScheduleDokument1 SeiteH&M Inspection ScheduleShakil Al JabirNoch keine Bewertungen

- Rekap Bon Belanja SeptemberDokument6 SeitenRekap Bon Belanja Septemberesty ameliaNoch keine Bewertungen

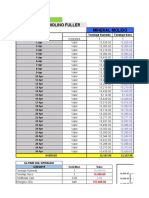

- Fuller Mill Mineral Grinding Trends in AprilDokument14 SeitenFuller Mill Mineral Grinding Trends in AprilCesar Francisco Quispe RomeroNoch keine Bewertungen

- Material ReceivingDokument26 SeitenMaterial Receivingahsan_butt_libraNoch keine Bewertungen

- Jay Ushin LTD: Receive Jobwork Challan Item ReportDokument8 SeitenJay Ushin LTD: Receive Jobwork Challan Item Reporttara_karkiNoch keine Bewertungen

- 1/16/2018 BT-05 Boom Truck J.Palad N.Gojo Cruz 332.8: Date Operator Helper Odometer Equipment Code Equipment DescriptionDokument78 Seiten1/16/2018 BT-05 Boom Truck J.Palad N.Gojo Cruz 332.8: Date Operator Helper Odometer Equipment Code Equipment DescriptionFroilan EspinosaNoch keine Bewertungen

- Sales and purchases journalsDokument7 SeitenSales and purchases journalsFileon ChiacNoch keine Bewertungen

- Kuya Doms FormatDokument7 SeitenKuya Doms FormatAnn Rey Nambayan (Rhae)Noch keine Bewertungen

- Cib GF Jan To Dec 2018Dokument413 SeitenCib GF Jan To Dec 2018Jerwin Cases TiamsonNoch keine Bewertungen

- PDF DocumentDokument2 SeitenPDF DocumentLinh Trang DamNoch keine Bewertungen

- WK 42 - 20 CARRIERS - S&P MARKET REPORTdraftDokument2 SeitenWK 42 - 20 CARRIERS - S&P MARKET REPORTdraftFotini HalouvaNoch keine Bewertungen

- IPO Advisory BlogDokument7 SeitenIPO Advisory Blogcalvinchoi0Noch keine Bewertungen

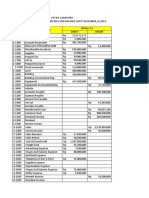

- PT FIFA COMPUTER TRIAL BALANCE AND BALANCE SHEETDokument70 SeitenPT FIFA COMPUTER TRIAL BALANCE AND BALANCE SHEETDwi Susanti NugrahaningtyasNoch keine Bewertungen

- Margin Guide: Agriculture EquitiesDokument3 SeitenMargin Guide: Agriculture EquitiesGaro OhanogluNoch keine Bewertungen

- Demurrage Summary - Dec19Dokument2 SeitenDemurrage Summary - Dec19Subramanian SaravananNoch keine Bewertungen

- Headwise Expenses Format OCT - 2019MMMMMDokument8 SeitenHeadwise Expenses Format OCT - 2019MMMMMtearstainedheartNoch keine Bewertungen

- Alce de Fruto Registros de CosechaDokument9 SeitenAlce de Fruto Registros de CosechaLUBRISERVICIOS JGNoch keine Bewertungen

- 10 - Account CurrentDokument5 Seiten10 - Account Currentjyotsanakirad1234Noch keine Bewertungen

- Kingsley Ozioko 1379711807 20210215060655Dokument29 SeitenKingsley Ozioko 1379711807 20210215060655Divine GraceofgodNoch keine Bewertungen

- Current Commanders For SaleDokument1 SeiteCurrent Commanders For SaleJuanNoch keine Bewertungen

- OTD Weekly Breakup Week #20Dokument16 SeitenOTD Weekly Breakup Week #20Zohair AbbasNoch keine Bewertungen

- Brothers Store Statement of AccountDokument7 SeitenBrothers Store Statement of AccountanwarNoch keine Bewertungen

- Rentaequipos Colombia rent and transport equipmentDokument1 SeiteRentaequipos Colombia rent and transport equipmentSantiago MoranthNoch keine Bewertungen

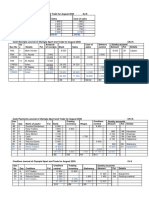

- Debtors Journal of Olympia Sport and Trade For August 2020DJ 8Dokument7 SeitenDebtors Journal of Olympia Sport and Trade For August 2020DJ 8thokoanebokang00Noch keine Bewertungen

- DSR Garut Oktober 2021Dokument7 SeitenDSR Garut Oktober 2021Zamzam HadiantoNoch keine Bewertungen

- SWAS BTST - STBT Calls Sheet For OCT-19: Sr. No Date Time Stocks Buy / Sell Lot Size (2x)Dokument42 SeitenSWAS BTST - STBT Calls Sheet For OCT-19: Sr. No Date Time Stocks Buy / Sell Lot Size (2x)Ashish Bhangale0% (1)

- Sales and Purchase Journal For October 2019Dokument14 SeitenSales and Purchase Journal For October 2019KarlayaanNoch keine Bewertungen

- Stock Detail S.NO. Material Amount RemarkDokument1 SeiteStock Detail S.NO. Material Amount RemarkEr Rohit VermaNoch keine Bewertungen

- Pt. Cyber Futures: Trading FormDokument3 SeitenPt. Cyber Futures: Trading FormHardjo PitoyoNoch keine Bewertungen

- Revisions NGDokument31 SeitenRevisions NGRobert ScorpionhhNoch keine Bewertungen

- Consolidated Statement For Savings AccountDokument3 SeitenConsolidated Statement For Savings AccountFrederick KamNoch keine Bewertungen

- Invoice: Dolsey LTD 863 West 44Th Street NORFOLK, VA 23508Dokument1 SeiteInvoice: Dolsey LTD 863 West 44Th Street NORFOLK, VA 23508Chris FendiNoch keine Bewertungen

- Shop Aguinaldo Liquidation ReportDokument1 SeiteShop Aguinaldo Liquidation ReportDjakob ManaogNoch keine Bewertungen

- AR-Report 26 April'10Dokument61 SeitenAR-Report 26 April'10dwinita fitriNoch keine Bewertungen

- Practice Test Answers CH 12Dokument3 SeitenPractice Test Answers CH 12Adoree RamosNoch keine Bewertungen

- Sales & Receivables Journal-CITRADokument2 SeitenSales & Receivables Journal-CITRAIqbal FisikaNoch keine Bewertungen

- PT GLN Facilities (Pig Launcher Gayam-Mudi Station) Chemical Consumption at P/L Gayam Fso Cinta NatomasDokument5 SeitenPT GLN Facilities (Pig Launcher Gayam-Mudi Station) Chemical Consumption at P/L Gayam Fso Cinta Natomasmohammad basukiNoch keine Bewertungen

- Week 41 S&P Market ReportDokument2 SeitenWeek 41 S&P Market ReportFotini HalouvaNoch keine Bewertungen

- Status Legend Customer Broker PO# Supplier DescriptionDokument6 SeitenStatus Legend Customer Broker PO# Supplier DescriptionJohn Carlo EstabilloNoch keine Bewertungen

- Trade NOV 2019Dokument4 SeitenTrade NOV 2019deep peNoch keine Bewertungen

- FA-Depreciation - Inventory SolvedDokument13 SeitenFA-Depreciation - Inventory SolvedAdhiraj MukherjeeNoch keine Bewertungen

- Inventory and Depreciation MethodsDokument13 SeitenInventory and Depreciation MethodsAdhiraj MukherjeeNoch keine Bewertungen

- Journal 4Dokument6 SeitenJournal 4RishiiieeeznNoch keine Bewertungen

- Jason A Brown: 1374 Cabin Creek Drive, Nicholson, GA 30565Dokument3 SeitenJason A Brown: 1374 Cabin Creek Drive, Nicholson, GA 30565Jason BrownNoch keine Bewertungen

- United States v. Christopher King, 724 F.2d 253, 1st Cir. (1984)Dokument9 SeitenUnited States v. Christopher King, 724 F.2d 253, 1st Cir. (1984)Scribd Government DocsNoch keine Bewertungen

- Class 11 English Snapshots Chapter 1Dokument2 SeitenClass 11 English Snapshots Chapter 1Harsh彡Eagle彡Noch keine Bewertungen

- UntitledDokument17 SeitenUntitledВладислав ПроскураNoch keine Bewertungen

- Research Paper Is at DominosDokument6 SeitenResearch Paper Is at Dominosssharma83Noch keine Bewertungen

- Assignment Brief Starting A Small BusinessDokument3 SeitenAssignment Brief Starting A Small BusinessFaraz0% (1)

- Ass 3 MGT206 11.9.2020Dokument2 SeitenAss 3 MGT206 11.9.2020Ashiqur RahmanNoch keine Bewertungen

- Bluetooth Mobile Based College CampusDokument12 SeitenBluetooth Mobile Based College CampusPruthviraj NayakNoch keine Bewertungen

- Unit 11 LeadershipDokument4 SeitenUnit 11 LeadershipMarijana DragašNoch keine Bewertungen

- Present Simple Tense ExplainedDokument12 SeitenPresent Simple Tense ExplainedRosa Beatriz Cantero DominguezNoch keine Bewertungen

- CPARDokument22 SeitenCPARAngelo Christian MandarNoch keine Bewertungen

- GNED 500 Social AnalysisDokument2 SeitenGNED 500 Social AnalysisEshita SinhaNoch keine Bewertungen

- BRM 6Dokument48 SeitenBRM 6Tanu GuptaNoch keine Bewertungen

- Sovereignty of AllahDokument1 SeiteSovereignty of AllahmajjjidNoch keine Bewertungen

- Global Trustworthiness 2022 ReportDokument32 SeitenGlobal Trustworthiness 2022 ReportCaroline PimentelNoch keine Bewertungen

- Subarachnoid Cisterns & Cerebrospinal FluidDokument41 SeitenSubarachnoid Cisterns & Cerebrospinal Fluidharjoth395Noch keine Bewertungen

- Sigafoose Robert Diane 1984 SingaporeDokument5 SeitenSigafoose Robert Diane 1984 Singaporethe missions networkNoch keine Bewertungen

- Indian Archaeology 1967 - 68 PDFDokument69 SeitenIndian Archaeology 1967 - 68 PDFATHMANATHANNoch keine Bewertungen

- Absolute TowersDokument11 SeitenAbsolute TowersSandi Harlan100% (1)

- Social Media Marketing - AssignmentDokument8 SeitenSocial Media Marketing - AssignmentAllen RodaNoch keine Bewertungen

- Ethical CRM PracticesDokument21 SeitenEthical CRM Practicesanon_522592057Noch keine Bewertungen

- Unit Revision-Integrated Systems For Business EnterprisesDokument8 SeitenUnit Revision-Integrated Systems For Business EnterprisesAbby JiangNoch keine Bewertungen