Das könnte Ihnen auch gefallen

- 2015: Outlook for Stocks, Bonds, Commodities, Currencies and Real EstateVon Everand2015: Outlook for Stocks, Bonds, Commodities, Currencies and Real EstateNoch keine Bewertungen

- Westpac WeeklyDokument10 SeitenWestpac WeeklysugengNoch keine Bewertungen

- DI Canada OutlookDokument8 SeitenDI Canada OutlookGeorge KapellosNoch keine Bewertungen

- India Investment Strategy - November 18Dokument26 SeitenIndia Investment Strategy - November 18shahavNoch keine Bewertungen

- Peru Economic Outlook 1Q17Dokument30 SeitenPeru Economic Outlook 1Q17Deepak SamavedamNoch keine Bewertungen

- Swiss Re Canada Economic Outlook 3Q19Dokument2 SeitenSwiss Re Canada Economic Outlook 3Q19Fox WalkerNoch keine Bewertungen

- Recent Economic Developments in Singapore: 5 September 2017Dokument20 SeitenRecent Economic Developments in Singapore: 5 September 2017Aroos AhmadNoch keine Bewertungen

- Economic Outlook - Risk Is A Sharper-Than-Expected Slowdown in in The 2H, Not A Double Dip - 18/6/2010Dokument14 SeitenEconomic Outlook - Risk Is A Sharper-Than-Expected Slowdown in in The 2H, Not A Double Dip - 18/6/2010Rhb InvestNoch keine Bewertungen

- Deloitte Au Cip Tourism Hotel Outlook Edition 1 2019 120419Dokument13 SeitenDeloitte Au Cip Tourism Hotel Outlook Edition 1 2019 120419deadlsweetyNoch keine Bewertungen

- WTO Trade Statistics and Outlook April 2017Dokument21 SeitenWTO Trade Statistics and Outlook April 2017Coleman NeeNoch keine Bewertungen

- Economic Outlook 2016 12Dokument13 SeitenEconomic Outlook 2016 12vae2797Noch keine Bewertungen

- Ups and Downs: Inside..Dokument9 SeitenUps and Downs: Inside..buddhacrisNoch keine Bewertungen

- Global inflation outlook and monetary policy challengesDokument4 SeitenGlobal inflation outlook and monetary policy challengesUneth CityNoch keine Bewertungen

- Director ReportDokument48 SeitenDirector ReportAakash DasNoch keine Bewertungen

- Performance of Debt Markt: An Article ReviewDokument11 SeitenPerformance of Debt Markt: An Article ReviewNida SubhaniNoch keine Bewertungen

- Global Economic ResearchDokument6 SeitenGlobal Economic ResearchAndyNoch keine Bewertungen

- Us Real Estate Outlook 2018Dokument28 SeitenUs Real Estate Outlook 2018gollumNoch keine Bewertungen

- BRICS Economies: An AnalysisDokument6 SeitenBRICS Economies: An AnalysismilagrosNoch keine Bewertungen

- Mid-Year Investment Outlook For 2023Dokument14 SeitenMid-Year Investment Outlook For 2023ShreyNoch keine Bewertungen

- MI WP YearAhead2023 PDFDokument13 SeitenMI WP YearAhead2023 PDFJNoch keine Bewertungen

- ARTICLEDokument2 SeitenARTICLEMj BollenaNoch keine Bewertungen

- Weo Update July 2017 PDFDokument7 SeitenWeo Update July 2017 PDFhgfed4321Noch keine Bewertungen

- Statement of The Monetary Policy Committee - 24 January 2017Dokument10 SeitenStatement of The Monetary Policy Committee - 24 January 2017Tiso Blackstar GroupNoch keine Bewertungen

- Crisil Sme Connect Feb10Dokument36 SeitenCrisil Sme Connect Feb10ramanindiaNoch keine Bewertungen

- US Economic Outlook - For 2017 and BeyondDokument6 SeitenUS Economic Outlook - For 2017 and BeyondpiyushNoch keine Bewertungen

- Croatia GDP Growth to Remain Strong Despite RisksDokument2 SeitenCroatia GDP Growth to Remain Strong Despite RisksHasan DelibaltaNoch keine Bewertungen

- Swedbank Economic Outlook Update, November 2015Dokument17 SeitenSwedbank Economic Outlook Update, November 2015Swedbank AB (publ)Noch keine Bewertungen

- Directors' Report: I. Economic Backdrop and Banking EnvironmentDokument53 SeitenDirectors' Report: I. Economic Backdrop and Banking EnvironmentPuja BhallaNoch keine Bewertungen

- Oct 21st Bank of Canada Rate AnnouncementDokument2 SeitenOct 21st Bank of Canada Rate AnnouncementMortgage ResourcesNoch keine Bewertungen

- Factors Affecting Investments in Pakistan's EconomyDokument7 SeitenFactors Affecting Investments in Pakistan's EconomyHome PhoneNoch keine Bewertungen

- Asian Development Outlook: Paths Diverge in Recovery From The PandemicDokument7 SeitenAsian Development Outlook: Paths Diverge in Recovery From The PandemicChea ChetraNoch keine Bewertungen

- Chinese Economy - Macroeconomic Analysis For Tesla's Investment DecisionDokument6 SeitenChinese Economy - Macroeconomic Analysis For Tesla's Investment DecisionVrajesh ChitaliaNoch keine Bewertungen

- NZ Economic OutlookDokument15 SeitenNZ Economic OutlookJohn ChoiNoch keine Bewertungen

- Crisil Ecoview: March 2010Dokument32 SeitenCrisil Ecoview: March 2010Aparajita BasakNoch keine Bewertungen

- Nedbank Se Rentekoers-Barometer Vir Mei 2016Dokument4 SeitenNedbank Se Rentekoers-Barometer Vir Mei 2016Netwerk24SakeNoch keine Bewertungen

- BC - Projects Portfolio Overview - Oct - LR1 Austrialia Hotel GroupDokument39 SeitenBC - Projects Portfolio Overview - Oct - LR1 Austrialia Hotel GroupEshwar KumarNoch keine Bewertungen

- Australia and New ZealandDokument11 SeitenAustralia and New ZealandedgarmerchanNoch keine Bewertungen

- PreBudgetExpectations2011-12 Anagram 180211Dokument18 SeitenPreBudgetExpectations2011-12 Anagram 180211chaterji_aNoch keine Bewertungen

- SEB Report: Asian Recovery - Please Hold The LineDokument9 SeitenSEB Report: Asian Recovery - Please Hold The LineSEB GroupNoch keine Bewertungen

- Happy New Year?: Liftoff!Dokument1 SeiteHappy New Year?: Liftoff!babbabeuNoch keine Bewertungen

- Philippine Economy Growth Slows in 2019 but Poverty Reduction ContinuesDokument5 SeitenPhilippine Economy Growth Slows in 2019 but Poverty Reduction ContinuesMichaelAngeloBattungNoch keine Bewertungen

- In Union Budget 2023 Detailed Analysis NoexpDokument78 SeitenIn Union Budget 2023 Detailed Analysis NoexppatrodeskNoch keine Bewertungen

- Crisil Sme Connect Dec09Dokument32 SeitenCrisil Sme Connect Dec09Rahul JainNoch keine Bewertungen

- Natixis Asia 2020 Outlook: Growth Still Slowing: C2 - Inter Nal NatixisDokument2 SeitenNatixis Asia 2020 Outlook: Growth Still Slowing: C2 - Inter Nal NatixisAlezNgNoch keine Bewertungen

- March Market Outlook: Equities & Commodities Under PressureDokument8 SeitenMarch Market Outlook: Equities & Commodities Under PressureMoed D'lhoxNoch keine Bewertungen

- Americas: Economic Review January 2011: at A GlanceDokument9 SeitenAmericas: Economic Review January 2011: at A Glancemathew_rexNoch keine Bewertungen

- Country Report India February 2022Dokument5 SeitenCountry Report India February 2022Daniel DannyNoch keine Bewertungen

- WEOupdateJan2019 PDFDokument8 SeitenWEOupdateJan2019 PDFsalt1322Noch keine Bewertungen

- GX Global Powers of Retailing 2022Dokument52 SeitenGX Global Powers of Retailing 2022Ngoc Ngan LyNoch keine Bewertungen

- Annual ReportDokument10 SeitenAnnual Reportcharu555Noch keine Bewertungen

- JPM2019-09 MI - 2020outlook - 112719Dokument12 SeitenJPM2019-09 MI - 2020outlook - 112719RyanNoch keine Bewertungen

- Statement by Philip Lowe, Governor: Monetary Policy Decision - Media Releases - RBADokument3 SeitenStatement by Philip Lowe, Governor: Monetary Policy Decision - Media Releases - RBATraderNoch keine Bewertungen

- Through The Looking Glass Chinas 2023 GDP and The Year AheadDokument11 SeitenThrough The Looking Glass Chinas 2023 GDP and The Year Aheadt8enedNoch keine Bewertungen

- Subsidiaries of Icici Bank Ar Fy2018Dokument512 SeitenSubsidiaries of Icici Bank Ar Fy2018AladdinNoch keine Bewertungen

- Global Economic Outlook1Dokument2 SeitenGlobal Economic Outlook1Harry CerqueiraNoch keine Bewertungen

- Monetary Policy Report - CanadaDokument12 SeitenMonetary Policy Report - CanadaHeenaNoch keine Bewertungen

- BC Economic Forecast BC Economic Forecast 2013-17013-17 - Feb13Dokument15 SeitenBC Economic Forecast BC Economic Forecast 2013-17013-17 - Feb13pikevrNoch keine Bewertungen

- What Is The Outlook For BRICsDokument7 SeitenWhat Is The Outlook For BRICstrolaiNoch keine Bewertungen

- 2023 AsiaDokument8 Seiten2023 AsiaJuan LaredoNoch keine Bewertungen

- MPR NOV 2017 - v3Dokument36 SeitenMPR NOV 2017 - v3Rossana CairaNoch keine Bewertungen

- NAB CEO Press Conference Transcript PDFDokument4 SeitenNAB CEO Press Conference Transcript PDFmrfutschNoch keine Bewertungen

- West Pac WeeklyDokument12 SeitenWest Pac WeeklymrfutschNoch keine Bewertungen

- Wbc-Ec 2020Dokument6 SeitenWbc-Ec 2020mrfutschNoch keine Bewertungen

- Ops PDFDokument43 SeitenOps PDFmrfutschNoch keine Bewertungen

- Australian Markets Weekly: Underemployment Dragging On Wages GrowthDokument6 SeitenAustralian Markets Weekly: Underemployment Dragging On Wages GrowthmrfutschNoch keine Bewertungen

- NAB Residential Property Survey Q1 2018Dokument11 SeitenNAB Residential Property Survey Q1 2018mrfutschNoch keine Bewertungen

- Eoy Doc 2018 PDFDokument3 SeitenEoy Doc 2018 PDFmrfutschNoch keine Bewertungen

- China Economic Update 15 April 2019Dokument3 SeitenChina Economic Update 15 April 2019mrfutschNoch keine Bewertungen

- ANZ Media CommentsDokument3 SeitenANZ Media CommentsmrfutschNoch keine Bewertungen

- Aus Chamber Westpac 2018 Q2Dokument14 SeitenAus Chamber Westpac 2018 Q2mrfutschNoch keine Bewertungen

- Bank Pac WeeklyDokument14 SeitenBank Pac WeeklymrfutschNoch keine Bewertungen

- ANZ Subordinated Offer DocumentDokument99 SeitenANZ Subordinated Offer DocumentmrfutschNoch keine Bewertungen

- 2018 ANZ Stadium Event Calendar: A-League, NRL, Concerts & MoreDokument1 Seite2018 ANZ Stadium Event Calendar: A-League, NRL, Concerts & MoremrfutschNoch keine Bewertungen

- 2018 ANZ Stadium Event Calendar: A-League, NRL, Concerts & MoreDokument1 Seite2018 ANZ Stadium Event Calendar: A-League, NRL, Concerts & MoremrfutschNoch keine Bewertungen

- ANU Key Dates WestpacDokument1 SeiteANU Key Dates WestpacmrfutschNoch keine Bewertungen

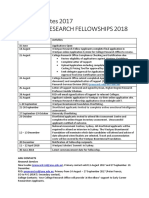

- Mailer 2017 Westpac Research Fellowships Opening of ApplicationsDokument1 SeiteMailer 2017 Westpac Research Fellowships Opening of ApplicationsmrfutschNoch keine Bewertungen

- West Pac WeeklyDokument10 SeitenWest Pac WeeklymrfutschNoch keine Bewertungen

- Westpac Future Leaders Scholarship Presentation 2016Dokument7 SeitenWestpac Future Leaders Scholarship Presentation 2016mrfutschNoch keine Bewertungen

- Budget PaperDokument308 SeitenBudget PapermrfutschNoch keine Bewertungen

- Teaching and Learning 21st Century SkillsDokument37 SeitenTeaching and Learning 21st Century SkillsMac SensNoch keine Bewertungen

- US Economic Update Points to Stronger Growth in Q2 2017Dokument5 SeitenUS Economic Update Points to Stronger Growth in Q2 2017mrfutschNoch keine Bewertungen

- Westpac Group Financial CalendarDokument4 SeitenWestpac Group Financial CalendarmrfutschNoch keine Bewertungen

- Quotes HieroclesDokument1 SeiteQuotes HieroclesmrfutschNoch keine Bewertungen

- RandDokument9 SeitenRandalfredNoch keine Bewertungen

- Dagon Rising - The Litany of Dagon by Phil HineDokument28 SeitenDagon Rising - The Litany of Dagon by Phil HineDru De Nicola De Nicola100% (1)

- Cults of Cthulhu - H.P. Lovecraft and The Occult TraditionDokument26 SeitenCults of Cthulhu - H.P. Lovecraft and The Occult TraditionTsigalko77100% (2)

- Parent Orientation Powerpoint-2013-2014 PreschoolDokument46 SeitenParent Orientation Powerpoint-2013-2014 PreschoolmrfutschNoch keine Bewertungen

- Economic OutlookDokument70 SeitenEconomic OutlookmrfutschNoch keine Bewertungen

- Macroeconomic: Policy EnvironmentDokument350 SeitenMacroeconomic: Policy Environmentavnish kanojiaNoch keine Bewertungen

- Opinion On TRAIN LawDokument9 SeitenOpinion On TRAIN LawVia Maria MalapoteNoch keine Bewertungen

- Common CoursesDokument37 SeitenCommon CoursesanusgeorgeNoch keine Bewertungen

- Managerial Economics Assessment-2: Model SolutionDokument10 SeitenManagerial Economics Assessment-2: Model SolutionR K SinghNoch keine Bewertungen

- Scarlett Tax Policy and Economic Growth in Jamaica FinalDokument28 SeitenScarlett Tax Policy and Economic Growth in Jamaica FinalBrandon KnightNoch keine Bewertungen

- Budget Reform Bill Atty Maria Paula DomingoDokument38 SeitenBudget Reform Bill Atty Maria Paula DomingoBernadette LlanetaNoch keine Bewertungen

- Solved Explain Whether Borrowing Constraints Increase or Decrease The Potency ofDokument1 SeiteSolved Explain Whether Borrowing Constraints Increase or Decrease The Potency ofM Bilal SaleemNoch keine Bewertungen

- Economic Growth: Cameroon'SDokument53 SeitenEconomic Growth: Cameroon'SFabrice EwoloNoch keine Bewertungen

- Crowding out explainedDokument3 SeitenCrowding out explainedsattysattuNoch keine Bewertungen

- Dashen Bank 2023 Report 4 Website 2 1Dokument63 SeitenDashen Bank 2023 Report 4 Website 2 1yemaneatakNoch keine Bewertungen

- Lobj18 0005498Dokument48 SeitenLobj18 0005498Nadil NinduwaraNoch keine Bewertungen

- ChinaDokument11 SeitenChinaSANGARA NANDA A/L KARRUPPIAH MoeNoch keine Bewertungen

- ব াংক ভাইভা সহািয়কাDokument15 Seitenব াংক ভাইভা সহািয়কাইরফানুল আলম সিদ্দীকিNoch keine Bewertungen

- MCQsDokument140 SeitenMCQsHAssan AftabNoch keine Bewertungen

- Key aspects of fiscal policy and budget processDokument40 SeitenKey aspects of fiscal policy and budget processdaljit singhNoch keine Bewertungen

- Chapter 5 UnemploymentDokument48 SeitenChapter 5 UnemploymentCha Boon KitNoch keine Bewertungen

- Managerial EconomicsDokument137 SeitenManagerial EconomicsDarshan AhlawatNoch keine Bewertungen

- Gabor European Derisking State-1Dokument30 SeitenGabor European Derisking State-1Maximus L MadusNoch keine Bewertungen

- BCA BrochureDokument15 SeitenBCA BrochurejitenparekhNoch keine Bewertungen

- Hsslive XII Economics Macro CH 5Dokument7 SeitenHsslive XII Economics Macro CH 5RameshKumarMuraliNoch keine Bewertungen

- 1.indra MaipitaDokument30 Seiten1.indra MaipitaDedy HusrizalNoch keine Bewertungen

- Duterte's Ambitious 'Build, Build, Build' Project To Transform The Philippines Could Become His LegacyDokument15 SeitenDuterte's Ambitious 'Build, Build, Build' Project To Transform The Philippines Could Become His LegacyHannah SantosNoch keine Bewertungen

- Fiscal Policy of IndiaDokument18 SeitenFiscal Policy of IndiaRahulNoch keine Bewertungen

- File 6530ce398b6c4 2024 2026 MTEF&FSP Transmittal Draft FinalDokument85 SeitenFile 6530ce398b6c4 2024 2026 MTEF&FSP Transmittal Draft FinalMayowa DurosinmiNoch keine Bewertungen

- Cyclical UnemploymentDokument7 SeitenCyclical UnemploymentKatherine PierceNoch keine Bewertungen

- FRBM ActDokument2 SeitenFRBM Actrajesh_scribd1984Noch keine Bewertungen

- ECE 202 Notes Study Economics Yr1 Prt2Dokument106 SeitenECE 202 Notes Study Economics Yr1 Prt2gavin henning100% (1)

- Public-Fiscal-Administration by Leonor BrionesDokument679 SeitenPublic-Fiscal-Administration by Leonor BrionesSherdoll Anne BayonaNoch keine Bewertungen

- BEGP2 OutDokument28 SeitenBEGP2 OutSainadha Reddy PonnapureddyNoch keine Bewertungen

- Economics/05 Monetary and Fiscal PolicyDokument45 SeitenEconomics/05 Monetary and Fiscal PolicyHarshavardhan SJNoch keine Bewertungen

- How to Talk to Anyone at Work: 72 Little Tricks for Big Success Communicating on the JobVon EverandHow to Talk to Anyone at Work: 72 Little Tricks for Big Success Communicating on the JobBewertung: 4.5 von 5 Sternen4.5/5 (36)

- 7 Principles of Transformational Leadership: Create a Mindset of Passion, Innovation, and GrowthVon Everand7 Principles of Transformational Leadership: Create a Mindset of Passion, Innovation, and GrowthBewertung: 5 von 5 Sternen5/5 (51)

- The Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverVon EverandThe Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverBewertung: 4.5 von 5 Sternen4.5/5 (186)

- The Power of People Skills: How to Eliminate 90% of Your HR Problems and Dramatically Increase Team and Company Morale and PerformanceVon EverandThe Power of People Skills: How to Eliminate 90% of Your HR Problems and Dramatically Increase Team and Company Morale and PerformanceBewertung: 5 von 5 Sternen5/5 (22)

- How to Lead: Wisdom from the World's Greatest CEOs, Founders, and Game ChangersVon EverandHow to Lead: Wisdom from the World's Greatest CEOs, Founders, and Game ChangersBewertung: 4.5 von 5 Sternen4.5/5 (94)

- The 7 Habits of Highly Effective PeopleVon EverandThe 7 Habits of Highly Effective PeopleBewertung: 4 von 5 Sternen4/5 (2564)

- The First Minute: How to start conversations that get resultsVon EverandThe First Minute: How to start conversations that get resultsBewertung: 4.5 von 5 Sternen4.5/5 (55)

- Leadership Skills that Inspire Incredible ResultsVon EverandLeadership Skills that Inspire Incredible ResultsBewertung: 4.5 von 5 Sternen4.5/5 (11)

- Spark: How to Lead Yourself and Others to Greater SuccessVon EverandSpark: How to Lead Yourself and Others to Greater SuccessBewertung: 4.5 von 5 Sternen4.5/5 (130)

- Transformed: Moving to the Product Operating ModelVon EverandTransformed: Moving to the Product Operating ModelBewertung: 4 von 5 Sternen4/5 (1)

- Billion Dollar Lessons: What You Can Learn from the Most Inexcusable Business Failures of the Last Twenty-five YearsVon EverandBillion Dollar Lessons: What You Can Learn from the Most Inexcusable Business Failures of the Last Twenty-five YearsBewertung: 4.5 von 5 Sternen4.5/5 (52)

- Scaling Up: How a Few Companies Make It...and Why the Rest Don't, Rockefeller Habits 2.0Von EverandScaling Up: How a Few Companies Make It...and Why the Rest Don't, Rockefeller Habits 2.0Noch keine Bewertungen

- The 4 Disciplines of Execution: Revised and Updated: Achieving Your Wildly Important GoalsVon EverandThe 4 Disciplines of Execution: Revised and Updated: Achieving Your Wildly Important GoalsBewertung: 4.5 von 5 Sternen4.5/5 (47)

- Management Mess to Leadership Success: 30 Challenges to Become the Leader You Would FollowVon EverandManagement Mess to Leadership Success: 30 Challenges to Become the Leader You Would FollowBewertung: 4.5 von 5 Sternen4.5/5 (27)

- Work Stronger: Habits for More Energy, Less Stress, and Higher Performance at WorkVon EverandWork Stronger: Habits for More Energy, Less Stress, and Higher Performance at WorkBewertung: 4.5 von 5 Sternen4.5/5 (12)

- Summary: Choose Your Enemies Wisely: Business Planning for the Audacious Few: Key Takeaways, Summary and AnalysisVon EverandSummary: Choose Your Enemies Wisely: Business Planning for the Audacious Few: Key Takeaways, Summary and AnalysisBewertung: 4.5 von 5 Sternen4.5/5 (3)

- The ONE Thing: The Surprisingly Simple Truth Behind Extraordinary Results: Key Takeaways, Summary & Analysis IncludedVon EverandThe ONE Thing: The Surprisingly Simple Truth Behind Extraordinary Results: Key Takeaways, Summary & Analysis IncludedBewertung: 4.5 von 5 Sternen4.5/5 (124)

- The Introverted Leader: Building on Your Quiet StrengthVon EverandThe Introverted Leader: Building on Your Quiet StrengthBewertung: 4.5 von 5 Sternen4.5/5 (35)

- Transformed: Moving to the Product Operating ModelVon EverandTransformed: Moving to the Product Operating ModelBewertung: 4 von 5 Sternen4/5 (1)

- The 12 Week Year: Get More Done in 12 Weeks than Others Do in 12 MonthsVon EverandThe 12 Week Year: Get More Done in 12 Weeks than Others Do in 12 MonthsBewertung: 4.5 von 5 Sternen4.5/5 (410)

- The Little Big Things: 163 Ways to Pursue ExcellenceVon EverandThe Little Big Things: 163 Ways to Pursue ExcellenceNoch keine Bewertungen

- Kaizen: The Ultimate Guide to Mastering Continuous Improvement And Transforming Your Life With Self DisciplineVon EverandKaizen: The Ultimate Guide to Mastering Continuous Improvement And Transforming Your Life With Self DisciplineBewertung: 4.5 von 5 Sternen4.5/5 (36)

- Unlocking Potential: 7 Coaching Skills That Transform Individuals, Teams, & OrganizationsVon EverandUnlocking Potential: 7 Coaching Skills That Transform Individuals, Teams, & OrganizationsBewertung: 4.5 von 5 Sternen4.5/5 (27)

- Sustainability Management: Global Perspectives on Concepts, Instruments, and StakeholdersVon EverandSustainability Management: Global Perspectives on Concepts, Instruments, and StakeholdersBewertung: 5 von 5 Sternen5/5 (1)

- 300+ PMP Practice Questions Aligned with PMBOK 7, Agile Methods, and Key Process Groups - 2024: First EditionVon Everand300+ PMP Practice Questions Aligned with PMBOK 7, Agile Methods, and Key Process Groups - 2024: First EditionNoch keine Bewertungen