Das könnte Ihnen auch gefallen

- Investigating The Influences of - Baek-Kyoo Joo PDFDokument20 SeitenInvestigating The Influences of - Baek-Kyoo Joo PDFYamil CruzNoch keine Bewertungen

- The Balanced Scorecard - The Evo - Helena Isabel Barroso Saraiva PDFDokument15 SeitenThe Balanced Scorecard - The Evo - Helena Isabel Barroso Saraiva PDFYamil CruzNoch keine Bewertungen

- The Fourth Theory of Worker Mot - J.J. Haefner PDFDokument5 SeitenThe Fourth Theory of Worker Mot - J.J. Haefner PDFYamil CruzNoch keine Bewertungen

- Towards A Unified Model of Empl - Darren J. Elding PDFDokument11 SeitenTowards A Unified Model of Empl - Darren J. Elding PDFYamil CruzNoch keine Bewertungen

- Application of Groupthink To Ge - David Hogg PDFDokument10 SeitenApplication of Groupthink To Ge - David Hogg PDFYamil CruzNoch keine Bewertungen

- INTEGRATING JOB CHARACTERISTICS - Bernadeta Gostautaite PDFDokument8 SeitenINTEGRATING JOB CHARACTERISTICS - Bernadeta Gostautaite PDFYamil CruzNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5782)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Pot PPTDokument35 SeitenPot PPTRandom PersonNoch keine Bewertungen

- Instant Download Ebook PDF Energy Systems Engineering Evaluation and Implementation Third 3rd Edition PDF ScribdDokument41 SeitenInstant Download Ebook PDF Energy Systems Engineering Evaluation and Implementation Third 3rd Edition PDF Scribdmichael.merchant471100% (43)

- Teacher swap agreement for family reasonsDokument4 SeitenTeacher swap agreement for family reasonsKimber LeeNoch keine Bewertungen

- Problem Areas in The Inpatient DepartmentDokument2 SeitenProblem Areas in The Inpatient DepartmentVineet AgarwalNoch keine Bewertungen

- Iso 1964 1987Dokument11 SeitenIso 1964 1987Dina ANDRIAMAHEFAHERYNoch keine Bewertungen

- Final Literature CircleDokument10 SeitenFinal Literature Circleapi-280793165Noch keine Bewertungen

- Annexure 2 Form 72 (Scope) Annexure IDokument4 SeitenAnnexure 2 Form 72 (Scope) Annexure IVaghasiyaBipinNoch keine Bewertungen

- AC & Crew Lists 881st 5-18-11Dokument43 SeitenAC & Crew Lists 881st 5-18-11ywbh100% (2)

- Bo de On Thi Hoc Ki 1 Lop 3 Mon Tieng AnhDokument66 SeitenBo de On Thi Hoc Ki 1 Lop 3 Mon Tieng AnhHằng DiệuNoch keine Bewertungen

- Court Reviews Liability of Staffing Agency for Damages Caused by Employee StrikeDokument5 SeitenCourt Reviews Liability of Staffing Agency for Damages Caused by Employee StrikeDenzhu MarcuNoch keine Bewertungen

- The Greco-Turkish War of 1920-1922: Greece Seeks Territory in Asia MinorDokument14 SeitenThe Greco-Turkish War of 1920-1922: Greece Seeks Territory in Asia MinorFauzan Rasip100% (1)

- Saic P 3311Dokument7 SeitenSaic P 3311Arshad ImamNoch keine Bewertungen

- Mental Health Admission & Discharge Dip NursingDokument7 SeitenMental Health Admission & Discharge Dip NursingMuranatu CynthiaNoch keine Bewertungen

- Thecodeblocks Com Acl in Nodejs ExplainedDokument1 SeiteThecodeblocks Com Acl in Nodejs ExplainedHamza JaveedNoch keine Bewertungen

- Line GraphDokument13 SeitenLine GraphMikelAgberoNoch keine Bewertungen

- Symbian Os-Seminar ReportDokument20 SeitenSymbian Os-Seminar Reportitsmemonu100% (1)

- HRM Unit 2Dokument69 SeitenHRM Unit 2ranjan_prashant52Noch keine Bewertungen

- Ck-Nac FsDokument2 SeitenCk-Nac Fsadamalay wardiwiraNoch keine Bewertungen

- Block 2 MVA 026Dokument48 SeitenBlock 2 MVA 026abhilash govind mishraNoch keine Bewertungen

- Effectiveness of Laundry Detergents and Bars in Removing Common StainsDokument9 SeitenEffectiveness of Laundry Detergents and Bars in Removing Common StainsCloudy ClaudNoch keine Bewertungen

- Instant Ear Thermometer: Instruction ManualDokument64 SeitenInstant Ear Thermometer: Instruction Manualrene_arevalo690% (1)

- Feminism in Lucia SartoriDokument41 SeitenFeminism in Lucia SartoriRaraNoch keine Bewertungen

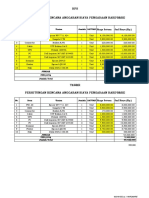

- HPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANDokument2 SeitenHPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANYanto AstriNoch keine Bewertungen

- Is The Question Too Broad or Too Narrow?Dokument3 SeitenIs The Question Too Broad or Too Narrow?teo100% (1)

- ICE Learned Event DubaiDokument32 SeitenICE Learned Event DubaiengkjNoch keine Bewertungen

- Fatwa Backbiting An Aalim Fatwa Razwiya PDFDokument3 SeitenFatwa Backbiting An Aalim Fatwa Razwiya PDFzubairmbbsNoch keine Bewertungen

- TDS Tetrapur 100 (12-05-2014) enDokument2 SeitenTDS Tetrapur 100 (12-05-2014) enCosmin MușatNoch keine Bewertungen

- Training of Local Government Personnel PHDokument5 SeitenTraining of Local Government Personnel PHThea ConsNoch keine Bewertungen

- Official Website of the Department of Homeland Security STEM OPT ExtensionDokument1 SeiteOfficial Website of the Department of Homeland Security STEM OPT ExtensionTanishq SankaNoch keine Bewertungen

- SEIPIDokument20 SeitenSEIPIdexterbautistadecember161985Noch keine Bewertungen