Das könnte Ihnen auch gefallen

- JD Sdn. BHD Study CaseDokument5 SeitenJD Sdn. BHD Study CaseSuperFlyFlyers100% (2)

- Valuing Capital Investment ProjectsDokument16 SeitenValuing Capital Investment ProjectsMetta AprilianaNoch keine Bewertungen

- How We Trade OptionsDokument21 SeitenHow We Trade Optionslecee01100% (1)

- IPMVP Core ConceptsDokument28 SeitenIPMVP Core ConceptsWaleed A. Shreim100% (1)

- Roche Site Redevelopment AnalysisDokument56 SeitenRoche Site Redevelopment AnalysisNJBIZNoch keine Bewertungen

- Implied Volatility Formula Excel TemplateDokument7 SeitenImplied Volatility Formula Excel Templateheisenburg0510Noch keine Bewertungen

- 100 % 36 Units Per Day 50 Trucks Per Day 100 % 100 % 36 Units Per Day 40 Trucks Per Day 100 %Dokument6 Seiten100 % 36 Units Per Day 50 Trucks Per Day 100 % 100 % 36 Units Per Day 40 Trucks Per Day 100 %Cherie Soriano AnanayoNoch keine Bewertungen

- Capital Investment/Net Present Value: Interest Rate DataDokument9 SeitenCapital Investment/Net Present Value: Interest Rate DataWILLAM FABIAN PASTUÑA CAISAGUANONoch keine Bewertungen

- Pasicolan, Mark Joshua BSA 3206: Absorption CostingDokument6 SeitenPasicolan, Mark Joshua BSA 3206: Absorption CostingMark Joshua PasicolanNoch keine Bewertungen

- Managerial Accounting NotesDokument6 SeitenManagerial Accounting NotesMarilou GabayaNoch keine Bewertungen

- B - S ModelDokument3 SeitenB - S ModelMos MasNoch keine Bewertungen

- Black Scholes Option Pricing ModelDokument20 SeitenBlack Scholes Option Pricing Modelsze0920Noch keine Bewertungen

- Year 0 1 Costs Benefits Cost of Capital Terminal ValueDokument4 SeitenYear 0 1 Costs Benefits Cost of Capital Terminal ValueSanjna ChimnaniNoch keine Bewertungen

- Financial Management Bruce HonniballDokument3 SeitenFinancial Management Bruce HonniballjanelleNoch keine Bewertungen

- Apparent Dip Calculator: Stereographic ProjectionDokument14 SeitenApparent Dip Calculator: Stereographic Projectionashfa ulyaNoch keine Bewertungen

- Case 6-1 (ANDI DIAN AULIA-46117022)Dokument5 SeitenCase 6-1 (ANDI DIAN AULIA-46117022)dianNoch keine Bewertungen

- CH 10 SolDokument7 SeitenCH 10 SolNotty SingerNoch keine Bewertungen

- SL No Y (X-RD) (1-T) : Problem Given That CalculateDokument2 SeitenSL No Y (X-RD) (1-T) : Problem Given That Calculatehasanarif0257Noch keine Bewertungen

- Inclass Solutions 5Dokument2 SeitenInclass Solutions 5AceNoch keine Bewertungen

- Breakeven Analysis Cost vs. RevenueDokument1 SeiteBreakeven Analysis Cost vs. RevenueDanielNoch keine Bewertungen

- Assign 4 Natividad BSA 2-13Dokument5 SeitenAssign 4 Natividad BSA 2-13Natividad, Kered ZilyoNoch keine Bewertungen

- Cost Accounting Y - Group A - Assignment11Dokument3 SeitenCost Accounting Y - Group A - Assignment11aldira jasmineNoch keine Bewertungen

- Accounting For Competitive Marketing A Case Study in Marketing Accounting Roxor Watch Company Pty LTDDokument7 SeitenAccounting For Competitive Marketing A Case Study in Marketing Accounting Roxor Watch Company Pty LTDKrystel Joie Caraig ChangNoch keine Bewertungen

- CoffeeCube SampleDokument13 SeitenCoffeeCube Samplelthanhhuyen15Noch keine Bewertungen

- 1 Manufacturing Units Cost Saving Versus Unit Purchase CostDokument5 Seiten1 Manufacturing Units Cost Saving Versus Unit Purchase CostPunkruk McentNoch keine Bewertungen

- Practical Problems & Solutions Class Work Upto IL.10Dokument20 SeitenPractical Problems & Solutions Class Work Upto IL.10Dhanishta PramodNoch keine Bewertungen

- Derivatives Test 3 SolnDokument12 SeitenDerivatives Test 3 SolnHetviNoch keine Bewertungen

- P13-20 (A) Probability 20% 60% 20%: Expexted EPS EPS XPRDokument3 SeitenP13-20 (A) Probability 20% 60% 20%: Expexted EPS EPS XPRJPNoch keine Bewertungen

- CS Topic 02 Marketing Accounting Roxor Watch CompanyDokument5 SeitenCS Topic 02 Marketing Accounting Roxor Watch CompanyIdham Idham IdhamNoch keine Bewertungen

- Corporate Tax Return Project Book-Tax Reconciliation (Adrian Purnama)Dokument6 SeitenCorporate Tax Return Project Book-Tax Reconciliation (Adrian Purnama)akpNoch keine Bewertungen

- Target - 320+87+114 (521) /2 261Dokument4 SeitenTarget - 320+87+114 (521) /2 261sneha patelNoch keine Bewertungen

- Break Even AnalysisDokument1 SeiteBreak Even AnalysisRama KrishnaNoch keine Bewertungen

- Chapter 13 ExcelDokument42 SeitenChapter 13 ExcelMd Al Alif Hossain 2121155630Noch keine Bewertungen

- CVP AnalysisDokument40 SeitenCVP Analysissbjafri0Noch keine Bewertungen

- Chapter 6 Example Trips LogisticsDokument10 SeitenChapter 6 Example Trips LogisticsYUSHIHUINoch keine Bewertungen

- Black Scholes Option Pricing - Dynamic ChartDokument2 SeitenBlack Scholes Option Pricing - Dynamic ChartRock11Noch keine Bewertungen

- Apparent DipDokument14 SeitenApparent Dipmarcos abalNoch keine Bewertungen

- Courtney Down April 06Dokument176 SeitenCourtney Down April 06MarcyNoch keine Bewertungen

- Principles of Corporate Finance: 6th EditionDokument4 SeitenPrinciples of Corporate Finance: 6th EditionParin MaruNoch keine Bewertungen

- Constructing A Downtown Parking Lot in DraperDokument7 SeitenConstructing A Downtown Parking Lot in DraperWater MelonNoch keine Bewertungen

- Solutions To End-Of-Chapter ProblemsDokument4 SeitenSolutions To End-Of-Chapter ProblemsRab RakhaNoch keine Bewertungen

- Task 5 - Pengantar Praktik PengauditanDokument3 SeitenTask 5 - Pengantar Praktik Pengauditanbriliant agengNoch keine Bewertungen

- Waterfall Analysis - 1X Liquidation PreferenceDokument9 SeitenWaterfall Analysis - 1X Liquidation PreferenceMonish KartheekNoch keine Bewertungen

- Sensitivity Analysis Excel TemplateDokument5 SeitenSensitivity Analysis Excel TemplateCele MthokoNoch keine Bewertungen

- FDNACCT - Quiz #2 - Problem Solving - Solutions-2Dokument4 SeitenFDNACCT - Quiz #2 - Problem Solving - Solutions-2Ichi HasukiNoch keine Bewertungen

- 06 Incremental AnalysisDokument11 Seiten06 Incremental AnalysisannarheaNoch keine Bewertungen

- Courtney Downs July 06Dokument51 SeitenCourtney Downs July 06MarcyNoch keine Bewertungen

- Roxor Case Study ComputationDokument4 SeitenRoxor Case Study ComputationAkun koreaNoch keine Bewertungen

- 02 - Oferta Vs DemandaDokument4 Seiten02 - Oferta Vs DemandaMiguel Angel Patiño AntonioliNoch keine Bewertungen

- Two Way Slab-SystemDokument7 SeitenTwo Way Slab-SystemMesfinNoch keine Bewertungen

- Assignment3 WorksheetDokument5 SeitenAssignment3 Worksheetjuri kimNoch keine Bewertungen

- Chapter 26. Tool Kit For Analysis of Capital Structure TheoryDokument11 SeitenChapter 26. Tool Kit For Analysis of Capital Structure TheoryJITIN ARORANoch keine Bewertungen

- Breakeven Analysis CalculatorDokument5 SeitenBreakeven Analysis CalculatoreibeffebieNoch keine Bewertungen

- Business Finance Decision Suggested Solution Test # 2: Answer - 1Dokument4 SeitenBusiness Finance Decision Suggested Solution Test # 2: Answer - 1Syed Muhammad Kazim RazaNoch keine Bewertungen

- Lab # 4-Head Loss in Pipes - FillableDokument4 SeitenLab # 4-Head Loss in Pipes - FillableSarah HaiderNoch keine Bewertungen

- Valuing Capital Investment ProjectsDokument13 SeitenValuing Capital Investment ProjectsSiddhesh MahadikNoch keine Bewertungen

- CVP AnalysisDokument6 SeitenCVP AnalysisSherilyn BunagNoch keine Bewertungen

- Fully Convertible Debenture:: Chapter 21: Convertible Debentures and WarrantsDokument2 SeitenFully Convertible Debenture:: Chapter 21: Convertible Debentures and WarrantsMukul KadyanNoch keine Bewertungen

- ORQUIA AssignmentDokument4 SeitenORQUIA AssignmentClint RoblesNoch keine Bewertungen

- Satistical Process Control Study: Data Collections:-Sample D2 A2 D4Dokument1 SeiteSatistical Process Control Study: Data Collections:-Sample D2 A2 D4cqi9nNoch keine Bewertungen

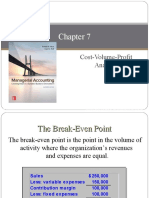

- Hilton 11e Chap007 StudentsDokument38 SeitenHilton 11e Chap007 StudentsMelix SianturiNoch keine Bewertungen

- Let's Practise: Maths Workbook Coursebook 7Von EverandLet's Practise: Maths Workbook Coursebook 7Noch keine Bewertungen

- Okay Okay OkayDokument1 SeiteOkay Okay OkayChukwunoso NwonyeNoch keine Bewertungen

- Beginners Guide To Candlestick TradingDokument87 SeitenBeginners Guide To Candlestick TradingChukwunoso Nwonye100% (1)

- Arrival TimesDokument4 SeitenArrival TimesChukwunoso NwonyeNoch keine Bewertungen

- Tek 9Dokument1 SeiteTek 9Iya CordilleraNoch keine Bewertungen

- 10 1 1 460 5807Dokument17 Seiten10 1 1 460 5807Chukwunoso NwonyeNoch keine Bewertungen

- Price Action Can Be A Pretty Vague Term.Dokument20 SeitenPrice Action Can Be A Pretty Vague Term.Chukwunoso NwonyeNoch keine Bewertungen

- EclipseDokument134 SeitenEclipseChukwunoso Nwonye100% (3)

- Contoh Format Apa StyleDokument8 SeitenContoh Format Apa StyleFutri F. FauziahNoch keine Bewertungen

- Favourite MenuDokument1 SeiteFavourite MenuChukwunoso NwonyeNoch keine Bewertungen

- Get StartDokument108 SeitenGet StartChukwunoso NwonyeNoch keine Bewertungen

- Title MultiZoneDryGasProducerDokument1 SeiteTitle MultiZoneDryGasProducerChukwunoso NwonyeNoch keine Bewertungen

- Examples - Heavy Oil Reservoirs Field Development PlanDokument4 SeitenExamples - Heavy Oil Reservoirs Field Development PlanChukwunoso NwonyeNoch keine Bewertungen

- Title: How To Use This TemplateDokument8 SeitenTitle: How To Use This TemplatejaydeeNoch keine Bewertungen

- Introduction To Reservoir PetrophysicsDokument115 SeitenIntroduction To Reservoir PetrophysicsChukwunoso Nwonye100% (5)

- CalculationDokument9 SeitenCalculationChukwunoso NwonyeNoch keine Bewertungen

- Abbreviation Type of Valve: NPT National Pipe Taper ThreadDokument1 SeiteAbbreviation Type of Valve: NPT National Pipe Taper Threadrinjalb7752Noch keine Bewertungen

- WJETDokument9 SeitenWJETChukwunoso NwonyeNoch keine Bewertungen

- Abbreviations and AcronymsDokument1 SeiteAbbreviations and AcronymsChukwunoso NwonyeNoch keine Bewertungen

- Abbreviations and AcronymsDokument1 SeiteAbbreviations and AcronymsChukwunoso NwonyeNoch keine Bewertungen

- Abbreviations and AcronymsDokument1 SeiteAbbreviations and AcronymsChukwunoso NwonyeNoch keine Bewertungen

- NAPE Presentaion Time Table 2014Dokument1 SeiteNAPE Presentaion Time Table 2014Chukwunoso NwonyeNoch keine Bewertungen

- NAPE Presentaion Time Table 2014Dokument1 SeiteNAPE Presentaion Time Table 2014Chukwunoso NwonyeNoch keine Bewertungen

- Petrel - 2 Days Introduction Courseell DesignDokument7 SeitenPetrel - 2 Days Introduction Courseell DesignChukwunoso NwonyeNoch keine Bewertungen

- Five Exploration Blocks Farm-In Opportunities in Chad - FLYERDokument4 SeitenFive Exploration Blocks Farm-In Opportunities in Chad - FLYERChukwunoso NwonyeNoch keine Bewertungen

- Introduction To Static Model DevelopmentDokument34 SeitenIntroduction To Static Model DevelopmentChukwunoso Nwonye100% (2)

- Numerical Methods in WE-HomeWork 02Dokument1 SeiteNumerical Methods in WE-HomeWork 02Chukwunoso NwonyeNoch keine Bewertungen

- Introduction To R ProgrammingDokument22 SeitenIntroduction To R ProgrammingSwayamtrupta PandaNoch keine Bewertungen

- Best First RTutorialDokument17 SeitenBest First RTutorialfrancobeckham23Noch keine Bewertungen

- Topic 2 ActivitiesDokument2 SeitenTopic 2 ActivitiesPhuong DoNoch keine Bewertungen

- Chapter09 IfDokument10 SeitenChapter09 IfPatricia PamelaNoch keine Bewertungen

- Case Study: Collapse of Long-Term Capital ManagementDokument20 SeitenCase Study: Collapse of Long-Term Capital ManagementVaibhav KharadeNoch keine Bewertungen

- Abbie Merry VecinaBSA 6011Dokument7 SeitenAbbie Merry VecinaBSA 6011elleeeewoodssssNoch keine Bewertungen

- Advace CH 2Dokument43 SeitenAdvace CH 2Bikila MalasaNoch keine Bewertungen

- Audit of PPE Initial MeasurementDokument2 SeitenAudit of PPE Initial MeasurementGwyneth TorrefloresNoch keine Bewertungen

- Assignment 3Dokument2 SeitenAssignment 3smartmanoj0% (1)

- Uber Vs GrabDokument10 SeitenUber Vs GrabZijian ZhuangNoch keine Bewertungen

- Dizon Vs CADokument1 SeiteDizon Vs CAGirin Pantangco NuqueNoch keine Bewertungen

- LM08 Equity Valuation Concepts and Basic Tools IFT NotesDokument19 SeitenLM08 Equity Valuation Concepts and Basic Tools IFT NotesClaptrapjackNoch keine Bewertungen

- Long Call Condor: Montréal ExchangeDokument3 SeitenLong Call Condor: Montréal ExchangepkkothariNoch keine Bewertungen

- Derivatives FT YtDokument28 SeitenDerivatives FT YtSuchit Backup1Noch keine Bewertungen

- Short Patriot One (TSX-PAT) - RousselDokument5 SeitenShort Patriot One (TSX-PAT) - RousselMichael Roussel60% (5)

- Chapter 2Dokument7 SeitenChapter 2Prakash SinghNoch keine Bewertungen

- What Is Double Diagonal Spread - FidelityDokument8 SeitenWhat Is Double Diagonal Spread - FidelityanalystbankNoch keine Bewertungen

- Chap III Off Balance Sheet ActivitiesDokument20 SeitenChap III Off Balance Sheet ActivitiesGing freexNoch keine Bewertungen

- CH 17Dokument39 SeitenCH 17IreneNoch keine Bewertungen

- Dizon v. CA 302 SCRA 288 (1999)Dokument16 SeitenDizon v. CA 302 SCRA 288 (1999)citizenNoch keine Bewertungen

- DR Singh Options 121616-011016NewsletterBinder3 PDFDokument106 SeitenDR Singh Options 121616-011016NewsletterBinder3 PDFsilvofNoch keine Bewertungen

- Ch26 Tool KitADokument21 SeitenCh26 Tool KitARoy HemenwayNoch keine Bewertungen

- SS&C Technologies Certificate in Alternative Investment IndustryDokument45 SeitenSS&C Technologies Certificate in Alternative Investment IndustryUday MugalNoch keine Bewertungen

- Why Do We Need DerivativesDokument4 SeitenWhy Do We Need DerivativesAnkit AroraNoch keine Bewertungen

- Pleadings Docket No 7671-19 PDFDokument71 SeitenPleadings Docket No 7671-19 PDFMarkRossNoch keine Bewertungen

- Adikavi Nannaya University Mba 4TH Sem SyllabusDokument4 SeitenAdikavi Nannaya University Mba 4TH Sem Syllabusnkkiranmai0% (2)

- Unit 7Dokument18 SeitenUnit 7Nenevah AngelNoch keine Bewertungen

- Dhani Stocks User Manual - v.1.0Dokument15 SeitenDhani Stocks User Manual - v.1.0Pratap SinghNoch keine Bewertungen