Das könnte Ihnen auch gefallen

- Bumi ArmadaDokument60 SeitenBumi Armadamanimaran75Noch keine Bewertungen

- FEED Screen Whitepaper PlantDokument10 SeitenFEED Screen Whitepaper PlantazamshafiqNoch keine Bewertungen

- Vess TimeDokument3 SeitenVess TimeJose Rodrigo Salguero DuranNoch keine Bewertungen

- Replacing Gas-Assisted Glycol Pumps With Electric Pumps: Lessons LearnedDokument11 SeitenReplacing Gas-Assisted Glycol Pumps With Electric Pumps: Lessons LearnedAmji ShahNoch keine Bewertungen

- Foam Behaviour of An Aqueous Solution of Piperazine Nmethyldiethanolamine Mdea Blend As A Function of The Type of Impurities and ConcentrationsDokument6 SeitenFoam Behaviour of An Aqueous Solution of Piperazine Nmethyldiethanolamine Mdea Blend As A Function of The Type of Impurities and ConcentrationsFraz RizviNoch keine Bewertungen

- Material Stream: 1: ConditionsDokument6 SeitenMaterial Stream: 1: ConditionsAKSHEYMEHTANoch keine Bewertungen

- Piperazine Hexahydrate Data SheetDokument2 SeitenPiperazine Hexahydrate Data SheetAnonymous T32l1RNoch keine Bewertungen

- The Effects of Fuel Additives On Diesel Engine Emissions During Steady State and Transient OperationDokument163 SeitenThe Effects of Fuel Additives On Diesel Engine Emissions During Steady State and Transient OperationMohamad El NaggarNoch keine Bewertungen

- D1560Dokument7 SeitenD1560Aleksei AvilaNoch keine Bewertungen

- A Tool For Analysis of Costs On The Manufacturing of The HullDokument7 SeitenA Tool For Analysis of Costs On The Manufacturing of The HullCleber001Noch keine Bewertungen

- Stena BlueGas Form C Sky - Gas Form CDokument17 SeitenStena BlueGas Form C Sky - Gas Form CpoetoetNoch keine Bewertungen

- Short History Og LNG VesselDokument32 SeitenShort History Og LNG VesseljwsommermannNoch keine Bewertungen

- 3.2 - Ballaguet & Barrère-Tricca - Sulphur CycleDokument24 Seiten3.2 - Ballaguet & Barrère-Tricca - Sulphur CyclesantiagoNoch keine Bewertungen

- Purchasing ManagerDokument3 SeitenPurchasing Managerapi-79114099Noch keine Bewertungen

- Tanker Operator April 2012Dokument60 SeitenTanker Operator April 2012Melissa CharnNoch keine Bewertungen

- Intertek Assay ReportDokument18 SeitenIntertek Assay Reportmohsen ranjbar100% (1)

- Intertanko Gas and Marine Seminar: Blending/Commingling of LPG Cargoes On Board Gas CarriersDokument19 SeitenIntertanko Gas and Marine Seminar: Blending/Commingling of LPG Cargoes On Board Gas Carriersmouloud miloud100% (1)

- Diethylene Glycol Cargo Handling SheetDokument7 SeitenDiethylene Glycol Cargo Handling SheettoanvmpetrologxNoch keine Bewertungen

- Diagram Alir Fluida 3 Fasa: Gas Dehydrator Gas Scrubber X-MastreeDokument1 SeiteDiagram Alir Fluida 3 Fasa: Gas Dehydrator Gas Scrubber X-Mastree'Aditz Nento S'Noch keine Bewertungen

- Tackling FSRU Operational ChallengesDokument22 SeitenTackling FSRU Operational ChallengesAnonymous icnhaNsFNoch keine Bewertungen

- Chemical AGRUDokument4 SeitenChemical AGRUDwi CahyonoNoch keine Bewertungen

- Cost Effective Integrated Gas Plant Design Sulfinol MDokument2 SeitenCost Effective Integrated Gas Plant Design Sulfinol Mamirho3ein100% (1)

- Compact LNG C Design Brochure - 110609Dokument4 SeitenCompact LNG C Design Brochure - 110609pal_malayNoch keine Bewertungen

- Propeller Cap TurbineDokument4 SeitenPropeller Cap TurbineKapil VermaNoch keine Bewertungen

- 002 Tacr enDokument233 Seiten002 Tacr enhandaru dwi yunantoNoch keine Bewertungen

- Different Types of TankersDokument23 SeitenDifferent Types of TankersBhupender Ramchandani100% (2)

- Exp 1Dokument18 SeitenExp 1Jennifer BurnettNoch keine Bewertungen

- Downstream Map LPG in IndonesiaDokument2 SeitenDownstream Map LPG in IndonesiaZaenal MutaqinNoch keine Bewertungen

- DNV Unveils LNG-Fueled VLCC..Dokument3 SeitenDNV Unveils LNG-Fueled VLCC..VelmohanaNoch keine Bewertungen

- Penspen Brochure 2015 UKDokument19 SeitenPenspen Brochure 2015 UKperrychemNoch keine Bewertungen

- Shaft Couplings and UJsDokument48 SeitenShaft Couplings and UJstahirabbasNoch keine Bewertungen

- 2596.1.03 - OfFSHORE - 02 - Selection of Trading Tankers For FPSO Conversion ProjectsDokument15 Seiten2596.1.03 - OfFSHORE - 02 - Selection of Trading Tankers For FPSO Conversion Projectsbooraj007100% (1)

- Frequently Asked Questions (FAQs) CII - Carbon Intensity Indicator - DNVDokument4 SeitenFrequently Asked Questions (FAQs) CII - Carbon Intensity Indicator - DNVanand raoNoch keine Bewertungen

- Final Report Freight IntegratorsDokument86 SeitenFinal Report Freight IntegratorsFattha FaisalNoch keine Bewertungen

- Gow Strategy Review March 2011Dokument15 SeitenGow Strategy Review March 2011Shraddha GhagNoch keine Bewertungen

- Dry Dock TermsDokument15 SeitenDry Dock TermswaleedyehiaNoch keine Bewertungen

- Test Separator Trailer Prices 2013Dokument3 SeitenTest Separator Trailer Prices 2013hermit44535Noch keine Bewertungen

- Structural Engineering Challenges in MODU To MOPU ConversionDokument18 SeitenStructural Engineering Challenges in MODU To MOPU Conversionrohitf117Noch keine Bewertungen

- 5NRJHL Saipem FY2020 Results JMEEBODokument42 Seiten5NRJHL Saipem FY2020 Results JMEEBOsudhakarrrrrrNoch keine Bewertungen

- Giignl Annual Report 2019-CompressedDokument56 SeitenGiignl Annual Report 2019-CompressedDivyansh SharmaNoch keine Bewertungen

- WSCE Mini LNG Plant Case StudiesDokument4 SeitenWSCE Mini LNG Plant Case StudiesKopi BrisbaneNoch keine Bewertungen

- Otc 21292 FPSO Motion CriteriaDokument7 SeitenOtc 21292 FPSO Motion CriteriaJean David ChanNoch keine Bewertungen

- FPSO Projects Worldwide 2019 - 1549865522Dokument1 SeiteFPSO Projects Worldwide 2019 - 1549865522Puix Ozil TherPanzer100% (1)

- LNG Terminals in JapanDokument12 SeitenLNG Terminals in Japantotoq51100% (2)

- Aldorf Presentation 5th World LNG August 31Dokument29 SeitenAldorf Presentation 5th World LNG August 31stavros7Noch keine Bewertungen

- Shell Time 4 May 02 As Amended July 03Dokument6 SeitenShell Time 4 May 02 As Amended July 03Antonia TrujiNoch keine Bewertungen

- Global LNG SupplyDokument38 SeitenGlobal LNG SupplyShravan MentaNoch keine Bewertungen

- Clean Tankerwire 030818Dokument7 SeitenClean Tankerwire 030818Philippos MichailidisNoch keine Bewertungen

- LNG - Urn 05 - 1016Dokument67 SeitenLNG - Urn 05 - 1016kaspersky2009Noch keine Bewertungen

- Joint Industry Guidance On The Supply and Use of 0.50 Sulphur Marine FuelDokument64 SeitenJoint Industry Guidance On The Supply and Use of 0.50 Sulphur Marine FuelharrdyNoch keine Bewertungen

- Voyage Estimating: Related NewsDokument11 SeitenVoyage Estimating: Related NewsNikhil SalviNoch keine Bewertungen

- Brochure Tge GasDokument13 SeitenBrochure Tge GasCemGülerNoch keine Bewertungen

- FSRU Market 2020 and BeyondDokument1 SeiteFSRU Market 2020 and Beyondabhey rathoreNoch keine Bewertungen

- Guidelines For Produced Water Evaporators in SAGD 2007Dokument16 SeitenGuidelines For Produced Water Evaporators in SAGD 2007pipedown456Noch keine Bewertungen

- Floating Gas Solutions: Project DisciplineDokument6 SeitenFloating Gas Solutions: Project DisciplinesmashfacemcgeeNoch keine Bewertungen

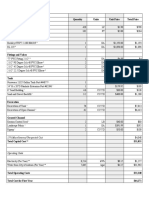

- Cost Estimate For Senior Design - Sheet1 1Dokument2 SeitenCost Estimate For Senior Design - Sheet1 1api-400559384Noch keine Bewertungen

- Cost Estimate For Senior Design - Sheet1 1Dokument2 SeitenCost Estimate For Senior Design - Sheet1 1api-400559384Noch keine Bewertungen

- 2008 SES Coke Drum User's Group SeminarDokument77 Seiten2008 SES Coke Drum User's Group SeminarJavier GarcíaNoch keine Bewertungen

- Dimon LetterDokument46 SeitenDimon LetterHeisenbergNoch keine Bewertungen

- The Traditional Epic Art of Bangladesh Intangible Cultural Heritage of HumanityDokument11 SeitenThe Traditional Epic Art of Bangladesh Intangible Cultural Heritage of HumanityKalipada SenNoch keine Bewertungen

- Analysis of Pile Foundation Subjected To Horizontal and Lateral ForcesDokument15 SeitenAnalysis of Pile Foundation Subjected To Horizontal and Lateral ForcesKalipada Sen100% (1)

- List of Indian Standard Code For Civil and Structural Works PDFDokument148 SeitenList of Indian Standard Code For Civil and Structural Works PDFKalipada Sen100% (1)

- Analysis of Pile Groups Subjected To Vertical and Horizontal Loads PDFDokument7 SeitenAnalysis of Pile Groups Subjected To Vertical and Horizontal Loads PDFKalipada SenNoch keine Bewertungen

- Displacement Design of Marine Structure For Batter Piles PDFDokument13 SeitenDisplacement Design of Marine Structure For Batter Piles PDFKalipada SenNoch keine Bewertungen

- PLNG Marine Operations Manual PDFDokument142 SeitenPLNG Marine Operations Manual PDFKalipada SenNoch keine Bewertungen

- CNG Vs LNG For Heavy Duty TrucksDokument7 SeitenCNG Vs LNG For Heavy Duty TrucksKalipada SenNoch keine Bewertungen

- Hoegh LNG FSRU PresentationDokument28 SeitenHoegh LNG FSRU PresentationKalipada Sen100% (1)

- Petronet LNG Limited - Dahej Terminal Information PDFDokument106 SeitenPetronet LNG Limited - Dahej Terminal Information PDFKalipada SenNoch keine Bewertungen

- PIANC - Guidelines For Protecting Berthing Structures From Scour Caused by Ships PDFDokument154 SeitenPIANC - Guidelines For Protecting Berthing Structures From Scour Caused by Ships PDFKalipada Sen100% (3)

- Maneuvering and Control of Marine VehiclesDokument152 SeitenManeuvering and Control of Marine VehiclesKalipada SenNoch keine Bewertungen

- Construction Method Jetty Area PDFDokument16 SeitenConstruction Method Jetty Area PDFKalipada Sen100% (6)

- Waves Measurement and AnalysisDokument168 SeitenWaves Measurement and Analysisnikhilgarg_gjuNoch keine Bewertungen

- FSRU FEED Document List - TypicalDokument9 SeitenFSRU FEED Document List - TypicalKalipada SenNoch keine Bewertungen

- Ship DynamicsDokument82 SeitenShip Dynamicsthenavaler100% (2)

- Designer Checklist For ASD TugDokument22 SeitenDesigner Checklist For ASD TugKalipada SenNoch keine Bewertungen

- Standard Inspection Report For The LNG FacilitesDokument22 SeitenStandard Inspection Report For The LNG FacilitesKalipada SenNoch keine Bewertungen

- A Letter To GodDokument48 SeitenA Letter To GodYushfa SheikhNoch keine Bewertungen

- Std9-Geog-latitude and Longitude (2013)Dokument8 SeitenStd9-Geog-latitude and Longitude (2013)LuciaNoch keine Bewertungen

- 001 VARS Tutor-ManualDokument6 Seiten001 VARS Tutor-ManualVenkatesh ModiNoch keine Bewertungen

- Providing (Or Provided), As (Or So) Long As, and On Condition ThatDokument1 SeiteProviding (Or Provided), As (Or So) Long As, and On Condition Thatgusti annisaNoch keine Bewertungen

- CBC BrochureDokument20 SeitenCBC BrochureMrinal RoyNoch keine Bewertungen

- Transport in Plants - Transpiration RateDokument26 SeitenTransport in Plants - Transpiration RatePavanchand ThakurNoch keine Bewertungen

- Anne Mather's TitlesDokument5 SeitenAnne Mather's Titlesmarastenv650% (3)

- Yokozawa Takafumi No Baai Story 4Dokument4 SeitenYokozawa Takafumi No Baai Story 4Don-don AnchetaNoch keine Bewertungen

- 04 Geography - PDF UsetDokument8 Seiten04 Geography - PDF UsetVijay Singh SultanNoch keine Bewertungen

- I Found My Heart in San Francisco 18 - RenewalDokument314 SeitenI Found My Heart in San Francisco 18 - RenewalLiv93100% (1)

- Plant Adaptations: Plants Can Survive in Many ExtremeDokument30 SeitenPlant Adaptations: Plants Can Survive in Many ExtremeAo AlandraNoch keine Bewertungen

- Tropical Architecture PhilDokument4 SeitenTropical Architecture PhilJohn Lesther BalondoNoch keine Bewertungen

- Drip XDokument2 SeitenDrip XMujjo SahbNoch keine Bewertungen

- ICDS Movie ReviewDokument3 SeitenICDS Movie ReviewAdarsh NethwewalaNoch keine Bewertungen

- MCQDokument53 SeitenMCQPawanNoch keine Bewertungen

- Tsunami - Catálogo 13/14Dokument88 SeitenTsunami - Catálogo 13/14nykd5Noch keine Bewertungen

- System Dynamics Simulation - RevisedDokument63 SeitenSystem Dynamics Simulation - RevisedSunny TrivediNoch keine Bewertungen

- Typhoon: Atmospheric ConditionDokument14 SeitenTyphoon: Atmospheric ConditionCleofe SobiacoNoch keine Bewertungen

- Gas Liquid Separation TechnologyDokument24 SeitenGas Liquid Separation TechnologyAlan ChewNoch keine Bewertungen

- Nepali English Dictionary PDFDokument148 SeitenNepali English Dictionary PDFMKPashaPashaNoch keine Bewertungen

- Geography TasksDokument31 SeitenGeography TasksD DurbNoch keine Bewertungen

- Global Warming: BY M.Sreedhar PatnaikDokument16 SeitenGlobal Warming: BY M.Sreedhar PatnaikSreedhar Patnaik.MNoch keine Bewertungen

- SARC Project Contingency MethodologyDokument5 SeitenSARC Project Contingency MethodologyMahesh ManoharanNoch keine Bewertungen

- Project Report On CSEBDokument6 SeitenProject Report On CSEBMahaManthraNoch keine Bewertungen

- Qual2kw5 TheoryDokument115 SeitenQual2kw5 TheoryIka Bayu KartikasariNoch keine Bewertungen

- Grammar PretestDokument11 SeitenGrammar PretestLanguageCentreNoch keine Bewertungen

- Water Security STD 9th Textbook by Techy BagDokument86 SeitenWater Security STD 9th Textbook by Techy Bagpooja TiwariNoch keine Bewertungen

- 1200 Commonly Repeated Words in IELTS Listening TestDokument3 Seiten1200 Commonly Repeated Words in IELTS Listening TestTracy VuNoch keine Bewertungen

- I Love You, You'Re Perfect... Now Change - SongbookDokument275 SeitenI Love You, You'Re Perfect... Now Change - SongbookAnonymous lLMYxNy97% (31)

- Normal Communication Behaviour of HospitDokument12 SeitenNormal Communication Behaviour of HospitArif AnwarNoch keine Bewertungen