Das könnte Ihnen auch gefallen

- Corporate Financial Analysis with Microsoft ExcelVon EverandCorporate Financial Analysis with Microsoft ExcelBewertung: 5 von 5 Sternen5/5 (1)

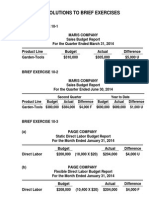

- Chapter 15 - Applied Problem Solutions PDFDokument4 SeitenChapter 15 - Applied Problem Solutions PDFZoha KamalNoch keine Bewertungen

- Balakrishnan MGRL Solutions Ch12Dokument30 SeitenBalakrishnan MGRL Solutions Ch12iluvumiNoch keine Bewertungen

- TutorialActivity 3Dokument7 SeitenTutorialActivity 3Adarsh AchoyburNoch keine Bewertungen

- Tutorial Problems - Capital BudgetingDokument6 SeitenTutorial Problems - Capital BudgetingMarcoBonaparte0% (1)

- WALMART CASE Group1 Finished Revised 3 PDFDokument50 SeitenWALMART CASE Group1 Finished Revised 3 PDFAbdil LahNoch keine Bewertungen

- Managerial Accounting Chapter 5 by GarrisonDokument4 SeitenManagerial Accounting Chapter 5 by GarrisonJoshua Hines100% (1)

- OB Chapter 1Dokument15 SeitenOB Chapter 1Naiha AbidNoch keine Bewertungen

- Chapter 4 - IbfDokument23 SeitenChapter 4 - IbfMuhib NoharioNoch keine Bewertungen

- Cost-Volume-Profit Relationships: Solutions To QuestionsDokument90 SeitenCost-Volume-Profit Relationships: Solutions To QuestionsKathryn Teo100% (1)

- Absorption Costing WorksheetDokument10 SeitenAbsorption Costing WorksheetFaizan ChNoch keine Bewertungen

- 2014 Bep Analysis ExercisesDokument5 Seiten2014 Bep Analysis ExercisesaimeeNoch keine Bewertungen

- MICRO ASS 1 Eco 401Dokument3 SeitenMICRO ASS 1 Eco 401Uroona MalikNoch keine Bewertungen

- If The Coat FitsDokument4 SeitenIf The Coat FitsAngelica OlescoNoch keine Bewertungen

- GNB14 e CH 12 ExamDokument6 SeitenGNB14 e CH 12 Exama_elsaied0% (1)

- Income Tax Guide UgandaDokument13 SeitenIncome Tax Guide UgandaMoses LubangakeneNoch keine Bewertungen

- Designing and Managing Global Marketing StrategiesDokument23 SeitenDesigning and Managing Global Marketing StrategiesShreekānth DāngiNoch keine Bewertungen

- Exam281 20131Dokument14 SeitenExam281 20131AsiiSobhiNoch keine Bewertungen

- Mavis Machine ShopDokument1 SeiteMavis Machine ShopSoni KavithaNoch keine Bewertungen

- Ilovepdf MergedDokument100 SeitenIlovepdf MergedVinny AujlaNoch keine Bewertungen

- Hilton Chapter 13 SolutionsDokument71 SeitenHilton Chapter 13 SolutionsSharkManLazersNoch keine Bewertungen

- RW J Chapter 14 Problem SolutionsDokument6 SeitenRW J Chapter 14 Problem SolutionsAlexandro Lai100% (1)

- Wallace Garden SupplyDokument4 SeitenWallace Garden SupplyestoniloannNoch keine Bewertungen

- Garrison 11ce SM ch11 FinalDokument90 SeitenGarrison 11ce SM ch11 FinalCoco ZaideNoch keine Bewertungen

- Standard CostingDokument18 SeitenStandard Costingpakistan 123Noch keine Bewertungen

- Ans. Corporate Finance Part 2Dokument17 SeitenAns. Corporate Finance Part 2HashimRazaNoch keine Bewertungen

- Ex Ante Beta MeasurementDokument24 SeitenEx Ante Beta MeasurementAnonymous MUA3E8tQNoch keine Bewertungen

- HorngrenIMA14eSM ch10Dokument66 SeitenHorngrenIMA14eSM ch10Zarafshan Gul Gul MuhammadNoch keine Bewertungen

- Operations Management: For Competitive AdvantageDokument47 SeitenOperations Management: For Competitive AdvantagedurgaselvamNoch keine Bewertungen

- AssignmentDokument2 SeitenAssignmentAbdul Moiz YousfaniNoch keine Bewertungen

- Capacity Planning: Mcgraw-Hill/IrwinDokument15 SeitenCapacity Planning: Mcgraw-Hill/IrwinKader KARAAĞAÇNoch keine Bewertungen

- Balakrishnan MGRL Solutions Ch14Dokument36 SeitenBalakrishnan MGRL Solutions Ch14Aditya Krishna100% (1)

- Baldwin Bicycle CompanyDokument19 SeitenBaldwin Bicycle CompanyMannu83Noch keine Bewertungen

- Uhu081 PDFDokument2 SeitenUhu081 PDFsahibjotNoch keine Bewertungen

- UAE Accounting System vs. IFRS Rules.Dokument6 SeitenUAE Accounting System vs. IFRS Rules.Shibam JhaNoch keine Bewertungen

- FA GP5 Assignment 1Dokument4 SeitenFA GP5 Assignment 1saurabhNoch keine Bewertungen

- Https Doc 0k 0s Apps Viewer - GoogleusercontentDokument4 SeitenHttps Doc 0k 0s Apps Viewer - GoogleusercontentAnuranjan Tirkey0% (1)

- Key CH 11 TExt HWprobsDokument3 SeitenKey CH 11 TExt HWprobsAshish BhallaNoch keine Bewertungen

- Ch01 fm202 Finance Small Business EnterpriseDokument9 SeitenCh01 fm202 Finance Small Business Enterprisepratik_483Noch keine Bewertungen

- Practice Midterm 1 SolutionsDokument22 SeitenPractice Midterm 1 Solutionsanupsoren100% (1)

- JobDokument4 SeitenJobNeha SmritiNoch keine Bewertungen

- Nestle-Organizational Behaviour With Refrence To 17 PointsDokument9 SeitenNestle-Organizational Behaviour With Refrence To 17 PointsKhaWaja HamMadNoch keine Bewertungen

- Ratio Analysis DG Khan Cement CompanyDokument6 SeitenRatio Analysis DG Khan Cement CompanysaleihasharifNoch keine Bewertungen

- Fin 4610 HW#1Dokument23 SeitenFin 4610 HW#1Michelle Lam100% (2)

- Jaiib Accounting Module C and Module DDokument340 SeitenJaiib Accounting Module C and Module DAkanksha MNoch keine Bewertungen

- Session 2 - by Catherine Rose Tumbali - PPTDokument25 SeitenSession 2 - by Catherine Rose Tumbali - PPTCathy TumbaliNoch keine Bewertungen

- Formulation of LP Problems-130928022247-Phpapp02Dokument13 SeitenFormulation of LP Problems-130928022247-Phpapp02Anish MonachanNoch keine Bewertungen

- Additional Revision QuestionsDokument3 SeitenAdditional Revision QuestionsShivneel Naidu100% (1)

- ABCQuestionsDokument4 SeitenABCQuestionsAdiltufail AdilNoch keine Bewertungen

- Manpri Case01 ConsolidatedAutomobileCaseAnalysisDokument3 SeitenManpri Case01 ConsolidatedAutomobileCaseAnalysisFrancisco Marvin100% (1)

- Solution Manual For Book CP 4Dokument107 SeitenSolution Manual For Book CP 4SkfNoch keine Bewertungen

- Chicago Valve TemplateDokument5 SeitenChicago Valve TemplatelittlemissjaceyNoch keine Bewertungen

- Lesson 9 Problems of Transfer Pricing Practical ExerciseDokument6 SeitenLesson 9 Problems of Transfer Pricing Practical ExerciseMadhu kumarNoch keine Bewertungen

- Mgt402 - 14midterm Solved PapersDokument125 SeitenMgt402 - 14midterm Solved Papersfari kh100% (1)

- Chapter 5 The Production Process and CostsDokument6 SeitenChapter 5 The Production Process and CostsChristlyn Joy BaralNoch keine Bewertungen

- MA PresentationDokument6 SeitenMA PresentationbarbaroNoch keine Bewertungen

- Sample Cases 1-11 With SolutionsDokument10 SeitenSample Cases 1-11 With SolutionsJenina Rose SalvadorNoch keine Bewertungen

- Capital Method BudgetingDokument7 SeitenCapital Method BudgetingWallace ChitambaNoch keine Bewertungen

- Chapter - 7 - Pay Back PeriodDokument15 SeitenChapter - 7 - Pay Back PeriodAhmed freshekNoch keine Bewertungen

- The Three Little PigsDokument1 SeiteThe Three Little Pigscarlo lastimosaNoch keine Bewertungen

- Hear and SpellDokument3 SeitenHear and Spellcarlo lastimosaNoch keine Bewertungen

- "Western Europe": Mariano Marcos State University College of Teacher Education Laoag CityDokument14 Seiten"Western Europe": Mariano Marcos State University College of Teacher Education Laoag Citycarlo lastimosaNoch keine Bewertungen

- Hear and SpellDokument3 SeitenHear and Spellcarlo lastimosaNoch keine Bewertungen

- Decision Making: Relevant Costs and Benefits: Mcgraw-Hill/IrwinDokument54 SeitenDecision Making: Relevant Costs and Benefits: Mcgraw-Hill/IrwinDaMin ZhouNoch keine Bewertungen

- Ch15 Questions 1Dokument4 SeitenCh15 Questions 1vietnam0711Noch keine Bewertungen

- Time Value of MoneyDokument8 SeitenTime Value of MoneyMuhammad Bilal IsrarNoch keine Bewertungen

- DemonetisationDokument3 SeitenDemonetisationKashreya JayakumarNoch keine Bewertungen

- Reservation ExerciseDokument2 SeitenReservation ExerciseMutia ChimoetNoch keine Bewertungen

- GoibiboDokument4 SeitenGoibiboAshok BansalNoch keine Bewertungen

- Weygandt Managerial 6e SM Release To Printer Ch10Dokument40 SeitenWeygandt Managerial 6e SM Release To Printer Ch10Dave Aguila100% (3)

- Career: Board of Director Mary Kay 1. David HollDokument4 SeitenCareer: Board of Director Mary Kay 1. David HollAmeer Al-asyraf MuhamadNoch keine Bewertungen

- 12 Ways To Beat Your BookieDokument82 Seiten12 Ways To Beat Your Bookieartus1460% (5)

- Airline TermsDokument8 SeitenAirline TermsVenus HatéNoch keine Bewertungen

- Saphelp Nw73ehp1 en 0c Ea5e52e35b627fe10000000a44538d FramesetDokument24 SeitenSaphelp Nw73ehp1 en 0c Ea5e52e35b627fe10000000a44538d Framesety2kmvrNoch keine Bewertungen

- Milken Institute - Mortgage Crisis OverviewDokument84 SeitenMilken Institute - Mortgage Crisis Overviewpemmott100% (3)

- Anatomia de Un Plan de Negocio - Linda Pinson PDFDokument282 SeitenAnatomia de Un Plan de Negocio - Linda Pinson PDFCarolina RuizNoch keine Bewertungen

- Process Costing LafargeDokument23 SeitenProcess Costing LafargeGbrnr Ia AndrntNoch keine Bewertungen

- The IS - LM CurveDokument28 SeitenThe IS - LM CurveVikku AgarwalNoch keine Bewertungen

- True or False in Financial ManagementDokument7 SeitenTrue or False in Financial ManagementDaniel HunksNoch keine Bewertungen

- Sworn Statement of Assets, Liabilities and Net WorthDokument4 SeitenSworn Statement of Assets, Liabilities and Net WorthSugar Fructose GalactoseNoch keine Bewertungen

- Data Sheet BC 547Dokument6 SeitenData Sheet BC 547rodmansupiitaNoch keine Bewertungen

- Taj Lake PalaceDokument2 SeitenTaj Lake PalaceYASHNoch keine Bewertungen

- MASB7 Construction Contract1Dokument2 SeitenMASB7 Construction Contract1hyraldNoch keine Bewertungen

- B-Com GP 1 2018 FinalDokument10 SeitenB-Com GP 1 2018 FinalKhalid AzizNoch keine Bewertungen

- 3 How To Create The PartsDokument47 Seiten3 How To Create The PartsArief Noor RahmanNoch keine Bewertungen

- Contract Change Order No. 1 RedactedDokument8 SeitenContract Change Order No. 1 RedactedL. A. PatersonNoch keine Bewertungen

- Classwork10 06-Chasekinnel 15Dokument4 SeitenClasswork10 06-Chasekinnel 15api-310965037Noch keine Bewertungen

- UN SMA 2015 Bahasa InggrisDokument5 SeitenUN SMA 2015 Bahasa InggrisMohammad EfendiNoch keine Bewertungen

- Marginal CostingDokument10 SeitenMarginal Costinganon_672065362Noch keine Bewertungen

- AFM Exam Report June 2020Dokument6 SeitenAFM Exam Report June 2020Mohsin AijazNoch keine Bewertungen

- SheltaDokument7 SeitenSheltaconfused597Noch keine Bewertungen

- Future Worth Analysis + Capitalized CostDokument19 SeitenFuture Worth Analysis + Capitalized CostjefftboiNoch keine Bewertungen

- Rationing Device: Exists Because of Scarcity. If There Were Enough Resources To Satisfy All Our SeeminglyDokument3 SeitenRationing Device: Exists Because of Scarcity. If There Were Enough Resources To Satisfy All Our SeeminglyMd RifatNoch keine Bewertungen