Das könnte Ihnen auch gefallen

- CA Notes Sale of Goods On Approval or Return Basis PDFDokument14 SeitenCA Notes Sale of Goods On Approval or Return Basis PDFBijay Aryan Dhakal100% (1)

- CAFCINTER CAFINAL CADokument72 SeitenCAFCINTER CAFINAL CAManmeet Singh100% (1)

- NAHTA Professional Classes Fund Accounting QuestionsDokument48 SeitenNAHTA Professional Classes Fund Accounting Questionsmonudeep aggarwalNoch keine Bewertungen

- As 16Dokument11 SeitenAs 16Harsh PatelNoch keine Bewertungen

- Unit 5: Death of A PartnerDokument23 SeitenUnit 5: Death of A PartnerKARTIK CHADHANoch keine Bewertungen

- Introduction To Final AccountsDokument38 SeitenIntroduction To Final AccountsCA Deepak Ehn88% (8)

- Investment Accounts: Attempt Wise AnalysisDokument54 SeitenInvestment Accounts: Attempt Wise AnalysisJaveedNoch keine Bewertungen

- 2b CA Intermediate GST Question Bank 8th Edition Dec 2021 ExamDokument232 Seiten2b CA Intermediate GST Question Bank 8th Edition Dec 2021 ExamSATHYA SAINATH MNoch keine Bewertungen

- CA IPCC Accounting Guideline Answers May 2015Dokument24 SeitenCA IPCC Accounting Guideline Answers May 2015Prashant PandeyNoch keine Bewertungen

- FOFA RatiosDokument11 SeitenFOFA RatiosShilpa RajuNoch keine Bewertungen

- MTP1 May2022 - Paper 5 Advanced AccountingDokument24 SeitenMTP1 May2022 - Paper 5 Advanced AccountingYash YashwantNoch keine Bewertungen

- Partnership NotesDokument68 SeitenPartnership NotesSandeepNoch keine Bewertungen

- Ca Ipcc Costing and Financial Management Suggested Answers May 2015Dokument20 SeitenCa Ipcc Costing and Financial Management Suggested Answers May 2015Prasanna KumarNoch keine Bewertungen

- Paper - 5: Advanced Accounting: © The Institute of Chartered Accountants of IndiaDokument31 SeitenPaper - 5: Advanced Accounting: © The Institute of Chartered Accountants of IndiaVarun reddyNoch keine Bewertungen

- CS Exec - Prog - Paper-2 Company AC Cost & Management AccountingDokument25 SeitenCS Exec - Prog - Paper-2 Company AC Cost & Management AccountingGautam SinghNoch keine Bewertungen

- CAF-BCK-Additional Questions PDFDokument24 SeitenCAF-BCK-Additional Questions PDFadnan sheikNoch keine Bewertungen

- Question Bank - Chapter 0: Compiled by Neeraj Arora and TEAMDokument14 SeitenQuestion Bank - Chapter 0: Compiled by Neeraj Arora and TEAMDaanish MittalNoch keine Bewertungen

- Law Quesbank by Amit PopliDokument300 SeitenLaw Quesbank by Amit PopliAashish Tiwari100% (1)

- Chapter 4 Share Capital and DebenturesDokument102 SeitenChapter 4 Share Capital and DebenturesAbhay SharmaNoch keine Bewertungen

- LEVERAGE Online Problem SheetDokument6 SeitenLEVERAGE Online Problem SheetSoumendra RoyNoch keine Bewertungen

- Paper - 3: Cost and Management Accounting: © The Institute of Chartered Accountants of IndiaDokument24 SeitenPaper - 3: Cost and Management Accounting: © The Institute of Chartered Accountants of IndiaUdaykiran BheemaganiNoch keine Bewertungen

- CA Final May 2020 Question Bank PDFDokument1.624 SeitenCA Final May 2020 Question Bank PDFAjay JosephNoch keine Bewertungen

- Chapter - 5: Toppers Institute N.P.O.-QuestionsDokument32 SeitenChapter - 5: Toppers Institute N.P.O.-QuestionsVivek kumarNoch keine Bewertungen

- Chapter 2 - Income From House PropertyDokument15 SeitenChapter 2 - Income From House PropertyPuran GuptaNoch keine Bewertungen

- M & A Solutions PDFDokument28 SeitenM & A Solutions PDFayushmehtha7Noch keine Bewertungen

- Financial AccountingDokument60 SeitenFinancial AccountingSurajNoch keine Bewertungen

- CAP III - Suggested Answer Papers - All Subjects - June 2019 PDFDokument133 SeitenCAP III - Suggested Answer Papers - All Subjects - June 2019 PDFsantosh thapa chhetriNoch keine Bewertungen

- Company Accounts Issue of Shares Par Premium DiscountDokument20 SeitenCompany Accounts Issue of Shares Par Premium DiscountDilwar Hussain100% (1)

- Chapter 7 - Value of Supply - NotesDokument16 SeitenChapter 7 - Value of Supply - NotesPuran GuptaNoch keine Bewertungen

- Taxation Paper 4: Income-tax Law Multiple Choice QuestionsDokument20 SeitenTaxation Paper 4: Income-tax Law Multiple Choice QuestionsKartik0% (1)

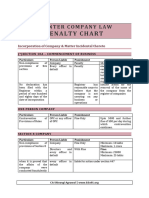

- Important Penalty - CA Inter LawDokument14 SeitenImportant Penalty - CA Inter Lawnagaraj9032230429100% (1)

- Law MTPDokument21 SeitenLaw MTPMohit SharmaNoch keine Bewertungen

- 01A Audit of Limited CompaniesDokument34 Seiten01A Audit of Limited CompaniesSai VardhanNoch keine Bewertungen

- Audit and Assurance CAP II Exam Suggested Answers 2010-2015Dokument111 SeitenAudit and Assurance CAP II Exam Suggested Answers 2010-2015shankar k.c.Noch keine Bewertungen

- Banking CompaniesDokument34 SeitenBanking CompaniesLodaNoch keine Bewertungen

- PGBPDokument45 SeitenPGBPNidhi Lath100% (1)

- NAS 37: Provisions, Contingent Liabilities & Contingent Assets NFRS 3: Business CombinationDokument24 SeitenNAS 37: Provisions, Contingent Liabilities & Contingent Assets NFRS 3: Business CombinationSushant MaskeyNoch keine Bewertungen

- Amagamation QnsDokument5 SeitenAmagamation Qnsmohanraokp2279Noch keine Bewertungen

- Cost Sheet - Pages 16Dokument16 SeitenCost Sheet - Pages 16omikron omNoch keine Bewertungen

- Corporate Accounting ProblemDokument6 SeitenCorporate Accounting ProblemparameshwaraNoch keine Bewertungen

- Profit Prior to Incorporation AccountsDokument7 SeitenProfit Prior to Incorporation AccountsParul Bhardwaj VaidyaNoch keine Bewertungen

- Revision Test Paper: Cap-Ii: Advanced Accounting: QuestionsDokument158 SeitenRevision Test Paper: Cap-Ii: Advanced Accounting: Questionsshankar k.c.Noch keine Bewertungen

- 5 Debenture Material3619080524732228932Dokument14 Seiten5 Debenture Material3619080524732228932Prabin stha100% (1)

- Accounting For Specialized Institution Set 2 Scheme of ValuationDokument19 SeitenAccounting For Specialized Institution Set 2 Scheme of ValuationTitus Clement100% (1)

- Unit 6: Average Due Date: Learning OutcomesDokument21 SeitenUnit 6: Average Due Date: Learning OutcomesAshish SultaniaNoch keine Bewertungen

- 18415compsuggans PCC FM Chapter7Dokument13 Seiten18415compsuggans PCC FM Chapter7Mukunthan RBNoch keine Bewertungen

- FR Additional Questions For Practice - Dec 21 ExamsDokument59 SeitenFR Additional Questions For Practice - Dec 21 ExamsmNoch keine Bewertungen

- CHARTERED ACCOUNTANCY PROFESSIONAL CAP-II REVISION TEST PAPERDokument21 SeitenCHARTERED ACCOUNTANCY PROFESSIONAL CAP-II REVISION TEST PAPERbinu100% (1)

- IND AS 32, 107, 109 (With Questions & Answers)Dokument69 SeitenIND AS 32, 107, 109 (With Questions & Answers)Suraj Dwivedi100% (1)

- CA Inter Paper 1 All Question PapersDokument205 SeitenCA Inter Paper 1 All Question PapersNivedita SharmaNoch keine Bewertungen

- F5 Division Roi RiDokument16 SeitenF5 Division Roi RiMazni HanisahNoch keine Bewertungen

- Admission of PartnerDokument3 SeitenAdmission of PartnerPraWin KharateNoch keine Bewertungen

- CAF-Business Economics PDFDokument40 SeitenCAF-Business Economics PDFadnan sheikNoch keine Bewertungen

- Accounting For Partnership Firms: Short Answer Type QuestionsDokument8 SeitenAccounting For Partnership Firms: Short Answer Type QuestionssalumNoch keine Bewertungen

- CA ZAMBIA PROGRAMME EXAM CONSOLIDATED GROUP STATEMENTDokument176 SeitenCA ZAMBIA PROGRAMME EXAM CONSOLIDATED GROUP STATEMENTinnocent moonoNoch keine Bewertungen

- Brs Practise SheetDokument1 SeiteBrs Practise Sheetapi-252642432Noch keine Bewertungen

- ICAI MCQ's INCOME TAX CA INTER MAY - NOV 2024Dokument49 SeitenICAI MCQ's INCOME TAX CA INTER MAY - NOV 2024Anil Reddy100% (1)

- 9405 - Corporate LiquidationDokument4 Seiten9405 - Corporate LiquidationKenneth Anthony BalitayoNoch keine Bewertungen

- Afar 02: Corporate Liquidation: I. True or False - Theory of AccountsDokument5 SeitenAfar 02: Corporate Liquidation: I. True or False - Theory of AccountsRoxell CaibogNoch keine Bewertungen

- Ca Final SFM (New Scheme) Dawn 2022 - Equity ValuationDokument55 SeitenCa Final SFM (New Scheme) Dawn 2022 - Equity Valuationanand kachwaNoch keine Bewertungen

- Detailed Advertisement For The Recruitment of 312 Administrative Officers (Generalists and Specialists) (Scale I) 2018Dokument20 SeitenDetailed Advertisement For The Recruitment of 312 Administrative Officers (Generalists and Specialists) (Scale I) 2018vignesh_vikiNoch keine Bewertungen

- Detailed Advertisement For The Recruitment of 312 Administrative Officers (Generalists and Specialists) (Scale I) 2018Dokument26 SeitenDetailed Advertisement For The Recruitment of 312 Administrative Officers (Generalists and Specialists) (Scale I) 2018msadithianNoch keine Bewertungen

- Books Applicable For May 2018Dokument1 SeiteBooks Applicable For May 2018vignesh_vikiNoch keine Bewertungen

- Financial ReportingDokument25 SeitenFinancial Reportingvignesh_vikiNoch keine Bewertungen

- CA Final SFM Chapter Wise Weightage Applicable For May 2017 NFUH6CATDokument1 SeiteCA Final SFM Chapter Wise Weightage Applicable For May 2017 NFUH6CATvignesh_vikiNoch keine Bewertungen

- First Time Adoption of Ind As 101Dokument3 SeitenFirst Time Adoption of Ind As 101vignesh_vikiNoch keine Bewertungen

- Financial Reporting Notes: Get Finapp On PlaystoreDokument31 SeitenFinancial Reporting Notes: Get Finapp On Playstorevignesh_vikiNoch keine Bewertungen

- CA Final Financial Reporting GMOWIC37Dokument83 SeitenCA Final Financial Reporting GMOWIC37vignesh_vikiNoch keine Bewertungen

- FR Theory NotesDokument31 SeitenFR Theory Notesvignesh_vikiNoch keine Bewertungen

- As 10 PpeDokument10 SeitenAs 10 Ppevignesh_viki100% (1)

- CA Final Financial Reporting Additional Material on Ind AS 32, 107 & 109 ClassificationDokument16 SeitenCA Final Financial Reporting Additional Material on Ind AS 32, 107 & 109 Classificationvignesh_viki100% (1)

- Sri Abirami Thunai temple packages and ratesDokument2 SeitenSri Abirami Thunai temple packages and ratesvignesh_vikiNoch keine Bewertungen

- Improving Employee Experience Through Gamification - Härkönen&TuominenDokument92 SeitenImproving Employee Experience Through Gamification - Härkönen&TuominenVenetia Angelopoulou ZaraliNoch keine Bewertungen

- Jun 2003 - AnsDokument15 SeitenJun 2003 - AnsHubbak KhanNoch keine Bewertungen

- Fashion Marketing of Luxury Brands Recen PDFDokument4 SeitenFashion Marketing of Luxury Brands Recen PDFCosmin RadulescuNoch keine Bewertungen

- 1597165857AFE 202 ASSIGNMENT Aransiola Grace Oluwadunsin Business PlanDokument16 Seiten1597165857AFE 202 ASSIGNMENT Aransiola Grace Oluwadunsin Business PlanMBI TABENoch keine Bewertungen

- Binu 500KDokument11 SeitenBinu 500KAnonymous XdHQb0Noch keine Bewertungen

- Project Report On TCS Courier ServicesDokument8 SeitenProject Report On TCS Courier ServicesMehwish ZahoorNoch keine Bewertungen

- 1687503543sapm 2018-19Dokument230 Seiten1687503543sapm 2018-19Arun P PrasadNoch keine Bewertungen

- P1-1a 6081901141Dokument2 SeitenP1-1a 6081901141Mentari AnggariNoch keine Bewertungen

- Sukuk Al-SalamDokument5 SeitenSukuk Al-SalamHasan Ali BokhariNoch keine Bewertungen

- Merit List Spring 2021Dokument6 SeitenMerit List Spring 2021Rezwan SiamNoch keine Bewertungen

- One-Year Global MBA at World's Largest Business SchoolDokument64 SeitenOne-Year Global MBA at World's Largest Business SchoolZia SilverNoch keine Bewertungen

- 空白信用证版本Dokument5 Seiten空白信用证版本ansontzengNoch keine Bewertungen

- Math 3 - EconomyDokument3 SeitenMath 3 - EconomyJeana Rick GallanoNoch keine Bewertungen

- Test 1 Ma2Dokument15 SeitenTest 1 Ma2Waseem Ahmad Qurashi63% (8)

- Jummy's Final ThesisDokument340 SeitenJummy's Final ThesisSucroses TxtNoch keine Bewertungen

- Genene Tadesse D. HundeDokument65 SeitenGenene Tadesse D. HundeGadaa TDhNoch keine Bewertungen

- Vendor Selection and Development GuideDokument20 SeitenVendor Selection and Development GuideAsher RamishNoch keine Bewertungen

- Developing Jordan's Urban Transport Infrastructure and Regulatory SystemDokument17 SeitenDeveloping Jordan's Urban Transport Infrastructure and Regulatory Systemmohammed ahmedNoch keine Bewertungen

- Chapter 2 The Marketing Environment Social Responsibility and EthicsDokument32 SeitenChapter 2 The Marketing Environment Social Responsibility and EthicsAnhQuocTranNoch keine Bewertungen

- Financial Statement Analysis of Lakshmigraha Worldwide IncDokument77 SeitenFinancial Statement Analysis of Lakshmigraha Worldwide IncSurendra SkNoch keine Bewertungen

- PT. Unilever Indonesia TBK.: Head OfficeDokument1 SeitePT. Unilever Indonesia TBK.: Head OfficeLinaNoch keine Bewertungen

- An Economic Snapshot of Coney Island and Brighton BeachDokument4 SeitenAn Economic Snapshot of Coney Island and Brighton BeachGarth JohnstonNoch keine Bewertungen

- BBMF2023Dokument7 SeitenBBMF2023Yi Lin ChiamNoch keine Bewertungen

- Questions With SolutionsDokument4 SeitenQuestions With SolutionsArshad UllahNoch keine Bewertungen

- Cooperatives (Republic Act No. 9520 A.k, A. Philippine Cooperative Code of 2008)Dokument14 SeitenCooperatives (Republic Act No. 9520 A.k, A. Philippine Cooperative Code of 2008)xinfamousxNoch keine Bewertungen

- Dmgt505 Management Information SystemDokument272 SeitenDmgt505 Management Information SystemJitendra SinghNoch keine Bewertungen

- Chapter 5 - Working Capital ManagementDokument24 SeitenChapter 5 - Working Capital ManagementFatimah Rashidi VirtuousNoch keine Bewertungen

- Trading The News Five ThingsDokument39 SeitenTrading The News Five ThingsRuiNoch keine Bewertungen

- Business Law and Regulations - CorporationDokument15 SeitenBusiness Law and Regulations - CorporationMargie RosetNoch keine Bewertungen

- Nifty Doctor Simple SystemDokument5 SeitenNifty Doctor Simple SystemPratik ChhedaNoch keine Bewertungen