Das könnte Ihnen auch gefallen

- Equity Valuation: Models from Leading Investment BanksVon EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNoch keine Bewertungen

- LP AnswerDokument6 SeitenLP Answerkibria youngsterNoch keine Bewertungen

- Engineering Service Revenues World Summary: Market Values & Financials by CountryVon EverandEngineering Service Revenues World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- 4ac1 02 Rms 20240125Dokument9 Seiten4ac1 02 Rms 20240125Nang Phyu Sin Yadanar KyawNoch keine Bewertungen

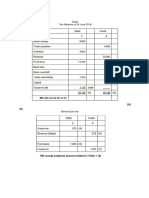

- Sujide, Kendrew Statement of Comprehensive IncomeDokument5 SeitenSujide, Kendrew Statement of Comprehensive IncomeKendrew SujideNoch keine Bewertungen

- Igcse May 2022 Paper 2R MSDokument10 SeitenIgcse May 2022 Paper 2R MSmihirNoch keine Bewertungen

- Batch 18 1st Preboard (P1)Dokument14 SeitenBatch 18 1st Preboard (P1)Jericho PedragosaNoch keine Bewertungen

- Statement of Comprehensive Income: Problem 1: True or FalseDokument17 SeitenStatement of Comprehensive Income: Problem 1: True or FalsePaula Bautista100% (3)

- Chapter 2 Statement of Comprehensive IncomeDokument4 SeitenChapter 2 Statement of Comprehensive IncomebwimeeeNoch keine Bewertungen

- Cost Sheet: (-) Sales of WastageDokument1 SeiteCost Sheet: (-) Sales of WastageAuras Raj PantaNoch keine Bewertungen

- Budgeting Review QuestionDokument5 SeitenBudgeting Review QuestionFrankNoch keine Bewertungen

- December 2007 Exam - Case 1 - AcmeGameDokument3 SeitenDecember 2007 Exam - Case 1 - AcmeGamesherif_awadNoch keine Bewertungen

- 2018 - Exam 1 - Q1 - Sug SolDokument4 Seiten2018 - Exam 1 - Q1 - Sug SolmamitjasNoch keine Bewertungen

- 9706 Accounting: MARK SCHEME For The May/June 2014 SeriesDokument6 Seiten9706 Accounting: MARK SCHEME For The May/June 2014 SeriesDanny DrinkwaterNoch keine Bewertungen

- MA1 sample of midterm testDokument4 SeitenMA1 sample of midterm testLoan VũNoch keine Bewertungen

- Sol. Man. - Chapter 2 - Statement of Comprehensive IncomeDokument15 SeitenSol. Man. - Chapter 2 - Statement of Comprehensive IncomeKATHRYN CLAUDETTE RESENTE100% (1)

- WAC11 01 Rms 20180815Dokument36 SeitenWAC11 01 Rms 20180815MirHaiderAliShaurovNoch keine Bewertungen

- Solution - Mock Exam - 240120 - 142640Dokument6 SeitenSolution - Mock Exam - 240120 - 142640lebiyacNoch keine Bewertungen

- FinAcc3 Chap4Dokument9 SeitenFinAcc3 Chap4Iyah AmranNoch keine Bewertungen

- Prepare Financial StatementsDokument16 SeitenPrepare Financial StatementsDayaan ANoch keine Bewertungen

- Answer Key Accounting Paper 2 Term 3 Form 4Dokument8 SeitenAnswer Key Accounting Paper 2 Term 3 Form 4Aejaz MohamedNoch keine Bewertungen

- Answer Key Accounting Paper 2 Term 3 Form 4Dokument8 SeitenAnswer Key Accounting Paper 2 Term 3 Form 4Aejaz MohamedNoch keine Bewertungen

- Mark Scheme (Provisional) Summer 2021Dokument25 SeitenMark Scheme (Provisional) Summer 2021Mashhood Babar ButtNoch keine Bewertungen

- Mark Scheme (Provisional) Summer 2021Dokument25 SeitenMark Scheme (Provisional) Summer 2021new yearNoch keine Bewertungen

- Accounting and Financial Management 1B Sample ExamDokument7 SeitenAccounting and Financial Management 1B Sample ExamS MNoch keine Bewertungen

- Mark Scheme With Examiners' Report: GCE A Level Accounting (9011)Dokument16 SeitenMark Scheme With Examiners' Report: GCE A Level Accounting (9011)hisakofelixNoch keine Bewertungen

- Activity No. 2 (Moredo) : Problem 1Dokument3 SeitenActivity No. 2 (Moredo) : Problem 1Eloisa Joy MoredoNoch keine Bewertungen

- Financial Accounting 2022 NeHu Question PaperDokument7 SeitenFinancial Accounting 2022 NeHu Question PaperSuraj BoseNoch keine Bewertungen

- TAX3761 EXAM PACK JPJBLFDokument146 SeitenTAX3761 EXAM PACK JPJBLFMonica Deetlefs0% (1)

- Business Finance Decision Suggested Solution Test # 2: Answer - 1Dokument4 SeitenBusiness Finance Decision Suggested Solution Test # 2: Answer - 1Syed Muhammad Kazim RazaNoch keine Bewertungen

- AFE 5008 Model Answers for Final ExamsDokument10 SeitenAFE 5008 Model Answers for Final ExamsDiana TuckerNoch keine Bewertungen

- Financial Accounting and Reporting - JA - 2022 - Suggested AnswersDokument8 SeitenFinancial Accounting and Reporting - JA - 2022 - Suggested AnswersMonira afrozNoch keine Bewertungen

- A - Mock PSPM Set 2Dokument6 SeitenA - Mock PSPM Set 2IZZAH NUR ATHIRAH BINTI AZLI MoeNoch keine Bewertungen

- CFAS 16 and 18Dokument2 SeitenCFAS 16 and 18Cath OquialdaNoch keine Bewertungen

- Manufacturing Costs and COGSDokument4 SeitenManufacturing Costs and COGSNia BranzuelaNoch keine Bewertungen

- Job Costing Question Bank SSDokument6 SeitenJob Costing Question Bank SSTamaraNoch keine Bewertungen

- Cost Accounting Question BankDokument28 SeitenCost Accounting Question BankdeepakgokuldasNoch keine Bewertungen

- Income Statement AnalysisDokument6 SeitenIncome Statement AnalysisLove IslamNoch keine Bewertungen

- Financial Accounting and Reporting: IFRS - 2015 December MSDokument18 SeitenFinancial Accounting and Reporting: IFRS - 2015 December MSMarchella LukitoNoch keine Bewertungen

- Chapter 6 Exercise Activity With AnswersDokument25 SeitenChapter 6 Exercise Activity With Answers乙คckคrψ YTNoch keine Bewertungen

- COST SHEET ANALYSISDokument5 SeitenCOST SHEET ANALYSISVasudev ANoch keine Bewertungen

- Example Problems W Solutions in SFP & SCFDokument7 SeitenExample Problems W Solutions in SFP & SCFQueen Valle100% (1)

- DAIBB Accounting 2020Dokument14 SeitenDAIBB Accounting 2020BelalHossainNoch keine Bewertungen

- Bracknell Cash Flow QuestionDokument3 SeitenBracknell Cash Flow Questionsanjay blakeNoch keine Bewertungen

- 9706 Accounting: MARK SCHEME For The May/June 2015 SeriesDokument6 Seiten9706 Accounting: MARK SCHEME For The May/June 2015 SeriesMahad UmarNoch keine Bewertungen

- Group assignment on FSDokument4 SeitenGroup assignment on FSHuyền TrangNoch keine Bewertungen

- Royal Escape LTD - Co Balance Sheet For The Month Ended, Dec.31,2020Dokument9 SeitenRoyal Escape LTD - Co Balance Sheet For The Month Ended, Dec.31,2020KemerutNoch keine Bewertungen

- 9706 Accounting: MARK SCHEME For The October/November 2008 Question PaperDokument5 Seiten9706 Accounting: MARK SCHEME For The October/November 2008 Question PapercheekybuoiNoch keine Bewertungen

- Answers 2014 Vol 3 CH 4 PDFDokument8 SeitenAnswers 2014 Vol 3 CH 4 PDFLian Blakely CousinNoch keine Bewertungen

- 9706 s12 Ms 22 PDFDokument6 Seiten9706 s12 Ms 22 PDFmarryNoch keine Bewertungen

- Cost and Management Accounting test answers under 40 charsDokument2 SeitenCost and Management Accounting test answers under 40 charsfarsi786100% (1)

- Zimsec - Nov - 2016 - Ms 3Dokument9 SeitenZimsec - Nov - 2016 - Ms 3Wesley KisiNoch keine Bewertungen

- MAC2601-SuggestedsolutionOct November2013Dokument12 SeitenMAC2601-SuggestedsolutionOct November2013DINEO PRUDENCE NONGNoch keine Bewertungen

- Banitog, Brigitte C. BSA 211Dokument8 SeitenBanitog, Brigitte C. BSA 211MyunimintNoch keine Bewertungen

- 4ac1-02-rms-20220825Dokument10 Seiten4ac1-02-rms-20220825attackdfg2002Noch keine Bewertungen

- Cost Accounting and Control 3Dokument4 SeitenCost Accounting and Control 3Davis MonNoch keine Bewertungen

- Financial Accounting and Reporting: IFRS - 2016 June MSDokument17 SeitenFinancial Accounting and Reporting: IFRS - 2016 June MSMarchella LukitoNoch keine Bewertungen

- AK Audit of Receivables ACP103Dokument2 SeitenAK Audit of Receivables ACP103km dummieNoch keine Bewertungen

- Core Mathematics C1: Pearson Edexcel GCEDokument28 SeitenCore Mathematics C1: Pearson Edexcel GCEni99leNoch keine Bewertungen

- 2005 Jan AS MOD MSDokument11 Seiten2005 Jan AS MOD MShisakofelixNoch keine Bewertungen

- Mark Scheme (Results) January 2016: Pearson Edexcel IAL in Accounting (WAC01) Paper 01Dokument21 SeitenMark Scheme (Results) January 2016: Pearson Edexcel IAL in Accounting (WAC01) Paper 01hisakofelixNoch keine Bewertungen

- Mark Scheme (Results) Summer 2013: International GCSE Accounting (4AC0)Dokument14 SeitenMark Scheme (Results) Summer 2013: International GCSE Accounting (4AC0)hisakofelixNoch keine Bewertungen

- 2007 Jan A2 MS PDFDokument11 Seiten2007 Jan A2 MS PDFhisakofelixNoch keine Bewertungen

- 4AC0 01 MSC 20110824 V4Dokument14 Seiten4AC0 01 MSC 20110824 V4hisakofelixNoch keine Bewertungen

- WST01 01 Que 20160615Dokument28 SeitenWST01 01 Que 20160615iKRaToSxNoch keine Bewertungen

- Question Paper1 2005 Accounts PDFDokument12 SeitenQuestion Paper1 2005 Accounts PDFhisakofelixNoch keine Bewertungen

- WST01 01 Que 20160615Dokument28 SeitenWST01 01 Que 20160615iKRaToSxNoch keine Bewertungen

- Core Mathematics C1: Pearson Edexcel GCEDokument28 SeitenCore Mathematics C1: Pearson Edexcel GCEni99leNoch keine Bewertungen

- EdExcel A Level Accountancy Unit 1 Paper 1 Jan 2008 PDFDokument28 SeitenEdExcel A Level Accountancy Unit 1 Paper 1 Jan 2008 PDFhisakofelixNoch keine Bewertungen

- 4AC0 01 MSC 20110824 V4Dokument14 Seiten4AC0 01 MSC 20110824 V4hisakofelixNoch keine Bewertungen

- 5203 - 0311 S1 November 2003Dokument5 Seiten5203 - 0311 S1 November 2003iantocNoch keine Bewertungen

- Insert Source Booklet Jan 09 6001Dokument12 SeitenInsert Source Booklet Jan 09 6001Yue Ying0% (1)

- 2007 Jan AS MS PDFDokument20 Seiten2007 Jan AS MS PDFhisakofelixNoch keine Bewertungen

- 2007 Jan AS MS PDFDokument20 Seiten2007 Jan AS MS PDFhisakofelixNoch keine Bewertungen

- 2002 May AS MSDokument14 Seiten2002 May AS MShisakofelixNoch keine Bewertungen

- 4AC0 01 MSC 20110824 V4Dokument14 Seiten4AC0 01 MSC 20110824 V4hisakofelixNoch keine Bewertungen

- 4AC0 June2011 ExampaperDokument28 Seiten4AC0 June2011 ExampaperhisakofelixNoch keine Bewertungen

- 2007 Jan AS MS PDFDokument20 Seiten2007 Jan AS MS PDFhisakofelixNoch keine Bewertungen

- 6663 01 Que 20150513Dokument32 Seiten6663 01 Que 20150513hisakofelixNoch keine Bewertungen

- 4AC0 01 MSC 20110824 V4Dokument14 Seiten4AC0 01 MSC 20110824 V4hisakofelixNoch keine Bewertungen

- 2007 Jan A2 MS PDFDokument11 Seiten2007 Jan A2 MS PDFhisakofelixNoch keine Bewertungen

- Mark Scheme With Examiners' Report: GCE A Level Accounting (9011)Dokument16 SeitenMark Scheme With Examiners' Report: GCE A Level Accounting (9011)hisakofelixNoch keine Bewertungen

- 4AC0 01 MSC 20110824 V4Dokument14 Seiten4AC0 01 MSC 20110824 V4hisakofelixNoch keine Bewertungen

- Mark Scheme With Examiners' Report: GCE A Level Accounting (9011)Dokument16 SeitenMark Scheme With Examiners' Report: GCE A Level Accounting (9011)hisakofelixNoch keine Bewertungen

- Upload-6001 01 Que 201301081365590466 PDFDokument52 SeitenUpload-6001 01 Que 201301081365590466 PDFhisakofelixNoch keine Bewertungen

- EdExcel A Level Accountancy Unit 2 Paper 1 Jan 2008 PDFDokument28 SeitenEdExcel A Level Accountancy Unit 2 Paper 1 Jan 2008 PDFhisakofelixNoch keine Bewertungen

- EdExcel A Level Accountancy Unit 1 Paper 1 Jan 2008 PDFDokument28 SeitenEdExcel A Level Accountancy Unit 1 Paper 1 Jan 2008 PDFhisakofelixNoch keine Bewertungen

- Programme Report Light The SparkDokument17 SeitenProgramme Report Light The SparkAbhishek Mishra100% (1)

- 3838 Chandra Dev Gurung BSBADM502 Assessment 2 ProjectDokument13 Seiten3838 Chandra Dev Gurung BSBADM502 Assessment 2 Projectxadow sahNoch keine Bewertungen

- Sapkale Sandspit 2020Dokument5 SeitenSapkale Sandspit 2020jbs_geoNoch keine Bewertungen

- Tata Chemicals Yearly Reports 2019 20Dokument340 SeitenTata Chemicals Yearly Reports 2019 20AkchikaNoch keine Bewertungen

- Empowerment Technologies Learning ActivitiesDokument7 SeitenEmpowerment Technologies Learning ActivitiesedzNoch keine Bewertungen

- Jurisdiction On Criminal Cases and PrinciplesDokument6 SeitenJurisdiction On Criminal Cases and PrinciplesJeffrey Garcia IlaganNoch keine Bewertungen

- 2JA5K2 FullDokument22 Seiten2JA5K2 FullLina LacorazzaNoch keine Bewertungen

- Credentials List with Multiple Usernames, Passwords and Expiration DatesDokument1 SeiteCredentials List with Multiple Usernames, Passwords and Expiration DatesJOHN VEGANoch keine Bewertungen

- Complaint Handling Policy and ProceduresDokument2 SeitenComplaint Handling Policy and Proceduresjyoti singhNoch keine Bewertungen

- TX Set 1 Income TaxDokument6 SeitenTX Set 1 Income TaxMarielle CastañedaNoch keine Bewertungen

- API MidtermDokument4 SeitenAPI MidtermsimranNoch keine Bewertungen

- Usa Easa 145Dokument31 SeitenUsa Easa 145Surya VenkatNoch keine Bewertungen

- Banas Dairy ETP Training ReportDokument38 SeitenBanas Dairy ETP Training ReportEagle eye0% (2)

- I. ICT (Information & Communication Technology: LESSON 1: Introduction To ICTDokument2 SeitenI. ICT (Information & Communication Technology: LESSON 1: Introduction To ICTEissa May VillanuevaNoch keine Bewertungen

- AKTA MERGER (FINAL) - MND 05 07 2020 FNLDokument19 SeitenAKTA MERGER (FINAL) - MND 05 07 2020 FNLNicoleNoch keine Bewertungen

- MiniQAR MK IIDokument4 SeitenMiniQAR MK IIChristina Gray0% (1)

- SD Electrolux LT 4 Partisi 21082023Dokument3 SeitenSD Electrolux LT 4 Partisi 21082023hanifahNoch keine Bewertungen

- Case Study - Soren ChemicalDokument3 SeitenCase Study - Soren ChemicalSallySakhvadzeNoch keine Bewertungen

- For Mail Purpose Performa For Reg of SupplierDokument4 SeitenFor Mail Purpose Performa For Reg of SupplierAkshya ShreeNoch keine Bewertungen

- Berry B Brey Part IDokument49 SeitenBerry B Brey Part Ikalpesh_chandakNoch keine Bewertungen

- Portable dual-input thermometer with RS232 connectivityDokument2 SeitenPortable dual-input thermometer with RS232 connectivityTaha OpedNoch keine Bewertungen

- 1990-1994 Electrical Wiring - DiagramsDokument13 Seiten1990-1994 Electrical Wiring - Diagramsal exNoch keine Bewertungen

- Applicants at Huye Campus SiteDokument4 SeitenApplicants at Huye Campus SiteHIRWA Cyuzuzo CedricNoch keine Bewertungen

- Royal Enfield Market PositioningDokument7 SeitenRoyal Enfield Market PositioningApoorv Agrawal67% (3)

- Chapter 1 Qus OnlyDokument28 SeitenChapter 1 Qus OnlySaksharNoch keine Bewertungen

- 7458-PM Putting The Pieces TogetherDokument11 Seiten7458-PM Putting The Pieces Togethermello06Noch keine Bewertungen

- StandardsDokument3 SeitenStandardshappystamps100% (1)

- Hardened Concrete - Methods of Test: Indian StandardDokument16 SeitenHardened Concrete - Methods of Test: Indian StandardjitendraNoch keine Bewertungen

- 1 Estafa - Arriola Vs PeopleDokument11 Seiten1 Estafa - Arriola Vs PeopleAtty Richard TenorioNoch keine Bewertungen

- Aptio ™ Text Setup Environment (TSE) User ManualDokument42 SeitenAptio ™ Text Setup Environment (TSE) User Manualdhirender karkiNoch keine Bewertungen