Das könnte Ihnen auch gefallen

- Types of Software MaintainanceDokument2 SeitenTypes of Software MaintainanceUn Int0% (1)

- WaterfallmodelDokument21 SeitenWaterfallmodelUn IntNoch keine Bewertungen

- Shohar Ke Huquq Biwi Ke ZimmeDokument2 SeitenShohar Ke Huquq Biwi Ke ZimmeUn IntNoch keine Bewertungen

- Auwlaad Ki Parvarish2Dokument30 SeitenAuwlaad Ki Parvarish2Un IntNoch keine Bewertungen

- Information Security Cyber Law Tutorial PDFDokument47 SeitenInformation Security Cyber Law Tutorial PDFKosma KosmicNoch keine Bewertungen

- WF ModelDokument17 SeitenWF ModelUn IntNoch keine Bewertungen

- SDLC Spiral ModelDokument3 SeitenSDLC Spiral ModelCieler GazeRock ArashiNoch keine Bewertungen

- 13software Maintenance Overview PDFDokument6 Seiten13software Maintenance Overview PDFSam BateNoch keine Bewertungen

- VmodelDokument12 SeitenVmodelUn IntNoch keine Bewertungen

- SDLC Waterfall ModelDokument4 SeitenSDLC Waterfall ModelUn IntNoch keine Bewertungen

- V-Model in Software EngineeringDokument16 SeitenV-Model in Software EngineeringUn IntNoch keine Bewertungen

- Taxatio Issues in IndiaDokument16 SeitenTaxatio Issues in IndiaUn IntNoch keine Bewertungen

- SDLC Agile Model PDFDokument3 SeitenSDLC Agile Model PDFAinee AliNoch keine Bewertungen

- WF ModelDokument17 SeitenWF ModelUn IntNoch keine Bewertungen

- SDLC Waterfall ModelDokument4 SeitenSDLC Waterfall ModelUn IntNoch keine Bewertungen

- Incrementalm ODELDokument16 SeitenIncrementalm ODELUn IntNoch keine Bewertungen

- Master Production ScheduleDokument10 SeitenMaster Production ScheduleUn IntNoch keine Bewertungen

- Whatarethechallengesfacedbyaleader 120313090654 Phpapp01Dokument14 SeitenWhatarethechallengesfacedbyaleader 120313090654 Phpapp01Un IntNoch keine Bewertungen

- Authentication 130728051757 Phpapp01Dokument22 SeitenAuthentication 130728051757 Phpapp01Un IntNoch keine Bewertungen

- Real Time Computerized BankingDokument2 SeitenReal Time Computerized BankingUn IntNoch keine Bewertungen

- Software Engineering TutorialDokument17 SeitenSoftware Engineering TutorialUn IntNoch keine Bewertungen

- Softwareestimation 140328050800 Phpapp01Dokument40 SeitenSoftwareestimation 140328050800 Phpapp01Un IntNoch keine Bewertungen

- Online BankingDokument5 SeitenOnline BankingUn IntNoch keine Bewertungen

- Sales Quote1Dokument2 SeitenSales Quote1Un IntNoch keine Bewertungen

- Sale Report TemplateDokument1 SeiteSale Report TemplateUn IntNoch keine Bewertungen

- Invoice TemplateDokument5 SeitenInvoice TemplateUn IntNoch keine Bewertungen

- Order ProcessingDokument22 SeitenOrder ProcessingUn IntNoch keine Bewertungen

- SL - No Qualification Experience NamesDokument4 SeitenSL - No Qualification Experience NamesUn IntNoch keine Bewertungen

- Market SegmentDokument16 SeitenMarket SegmentUn Int100% (1)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- A-Balance SheetDokument2 SeitenA-Balance SheetBabbu DHURIANoch keine Bewertungen

- TNC Family BankingDokument5 SeitenTNC Family BankingarshadNoch keine Bewertungen

- Project Report On Everest Bank LTDDokument28 SeitenProject Report On Everest Bank LTDdt_rock4463% (24)

- 12th MCVC - GFC - Resource MobilizationDokument12 Seiten12th MCVC - GFC - Resource MobilizationMohnish AsherNoch keine Bewertungen

- Executive SummaryDokument36 SeitenExecutive SummaryPooja NirmalNoch keine Bewertungen

- Class 11 Business Studies - Chapter 4Dokument19 SeitenClass 11 Business Studies - Chapter 4Chadalavada GaneshNoch keine Bewertungen

- SEBI Order in PWC Satyam CaseDokument108 SeitenSEBI Order in PWC Satyam Casebhupendra barhatNoch keine Bewertungen

- Awareness and Preferences of Small Savings Plans in ChennaiDokument93 SeitenAwareness and Preferences of Small Savings Plans in ChennaiSourav RoyNoch keine Bewertungen

- General Banking Activities of Janata Bank LimitedDokument52 SeitenGeneral Banking Activities of Janata Bank LimitedsikderNoch keine Bewertungen

- Final Accounts of Banking Companies Problems and SolutionsDokument27 SeitenFinal Accounts of Banking Companies Problems and Solutionsmy Vinay96% (57)

- Financing Self Help Groups of Syndicate Bank Under The Concept of Micro Finance in Bangalore Division KRpuramDokument73 SeitenFinancing Self Help Groups of Syndicate Bank Under The Concept of Micro Finance in Bangalore Division KRpuramPrashanth PB100% (1)

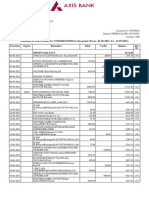

- Statement of Axis Account No:918010113912893 For The Period (From: 01-11-2019 To: 11-02-2020)Dokument4 SeitenStatement of Axis Account No:918010113912893 For The Period (From: 01-11-2019 To: 11-02-2020)Avinash DondapatyNoch keine Bewertungen

- Commercial BanksDokument7 SeitenCommercial BanksRashi BishtNoch keine Bewertungen

- Current AccountsDokument77 SeitenCurrent AccountsVijay AnuNoch keine Bewertungen

- Fixed DepositsDokument2 SeitenFixed DepositsNarendrapratap1Noch keine Bewertungen

- Care Ratings - March 2016 PDFDokument294 SeitenCare Ratings - March 2016 PDFSuresh WadhwaniNoch keine Bewertungen

- What Is BankDokument19 SeitenWhat Is BankSunayana BasuNoch keine Bewertungen

- HDFC Black Book 3 PDFDokument64 SeitenHDFC Black Book 3 PDFKarishma ThakurNoch keine Bewertungen

- Retail Loans On Abhudya BankDokument76 SeitenRetail Loans On Abhudya BankShubham SinghNoch keine Bewertungen

- PDFDokument4 SeitenPDFPrashant Thool0% (1)

- Statement of Axis Account No:917010066315582 For The Period (From: 01-06-2021 To: 12-09-2021)Dokument6 SeitenStatement of Axis Account No:917010066315582 For The Period (From: 01-06-2021 To: 12-09-2021)Anirban DebNoch keine Bewertungen

- 9.1 Banking and Financial Laws (Question Paper)Dokument2 Seiten9.1 Banking and Financial Laws (Question Paper)Medha DwivediNoch keine Bewertungen

- Statement Apr 23 XXXXXXXX8143 PDFDokument4 SeitenStatement Apr 23 XXXXXXXX8143 PDFSTUDY WITH MENoch keine Bewertungen

- DT Case Laws For May 2017Dokument86 SeitenDT Case Laws For May 2017Saurav KakkarNoch keine Bewertungen

- Shree Balaji Alloys v. CIT (2011) 333 ITR 335 (J&K)Dokument11 SeitenShree Balaji Alloys v. CIT (2011) 333 ITR 335 (J&K)Mahesh ThackerNoch keine Bewertungen

- Riaj FainalDokument73 SeitenRiaj FainalzikoNoch keine Bewertungen

- CARE Ratings As Sep2012Dokument191 SeitenCARE Ratings As Sep2012Prashanth TapseNoch keine Bewertungen

- Research WorkDokument74 SeitenResearch Workm.com22shiudkarsudarshanNoch keine Bewertungen

- The Complete Static Banking Awareness PDF CapsuleDokument101 SeitenThe Complete Static Banking Awareness PDF CapsuleS TharakNoch keine Bewertungen

- Study On: Changing Scenario of Investment in Financial MarketDokument79 SeitenStudy On: Changing Scenario of Investment in Financial MarketdarshanNoch keine Bewertungen