Das könnte Ihnen auch gefallen

- ImcDokument3 SeitenImcanishNoch keine Bewertungen

- MCQ PharmacokineticsDokument10 SeitenMCQ PharmacokineticsHarshit Sharma100% (1)

- Tata MotorsDokument27 SeitenTata MotorsShreyansi Singhal83% (6)

- Asian Paints (Case Study 3)Dokument8 SeitenAsian Paints (Case Study 3)Pratik Nayak0% (1)

- Guidance for Processing SushiDokument24 SeitenGuidance for Processing SushigsyaoNoch keine Bewertungen

- The Art of Communication PDFDokument3 SeitenThe Art of Communication PDFHung Tran JamesNoch keine Bewertungen

- A To Z of Architecture PDFDokument403 SeitenA To Z of Architecture PDFfaizan100% (1)

- Group1 Verona GroupDokument16 SeitenGroup1 Verona GroupF13 NIEC25% (4)

- 09 User Guide Xentry Diagnosis Kit 4 enDokument118 Seiten09 User Guide Xentry Diagnosis Kit 4 enDylan DY100% (2)

- Transformers Classics: UK Vol. 3 PreviewDokument10 SeitenTransformers Classics: UK Vol. 3 PreviewGraphic PolicyNoch keine Bewertungen

- London Jets Target Married Male CustomersDokument10 SeitenLondon Jets Target Married Male CustomersRajnesh kumar kundnaniNoch keine Bewertungen

- UCO Reporter 2021, December Edition, November 26, 2021Dokument40 SeitenUCO Reporter 2021, December Edition, November 26, 2021ucopresident100% (2)

- MARU BATTING CENTER CRM CASE STUDYDokument9 SeitenMARU BATTING CENTER CRM CASE STUDYAbsar HashmiNoch keine Bewertungen

- b2b CMR Group7 v8Dokument16 Seitenb2b CMR Group7 v8HarshShahNoch keine Bewertungen

- Strategic Plan TemplateDokument25 SeitenStrategic Plan Templateblazivica999Noch keine Bewertungen

- Cumberland Metal IndustriesDokument2 SeitenCumberland Metal IndustrieskakriakartikNoch keine Bewertungen

- GST's $5M CRM Initiative ROIDokument20 SeitenGST's $5M CRM Initiative ROIKanika Razdan BajajNoch keine Bewertungen

- ENSR - Case AnalysisDokument3 SeitenENSR - Case AnalysisNimish MohananNoch keine Bewertungen

- Transworld Auto Parts Case AnalysisDokument3 SeitenTransworld Auto Parts Case Analysisanon_14260130867% (3)

- CAN - Eli Lilly - Group 8Dokument6 SeitenCAN - Eli Lilly - Group 8Aman Singh100% (2)

- Evoe Spring Spa A Positioning DilemmaDokument16 SeitenEvoe Spring Spa A Positioning DilemmaNandini NagabhushanNoch keine Bewertungen

- TAP Auto Parts Strategy AnalysisDokument14 SeitenTAP Auto Parts Strategy AnalysisRidzki Dira PutraNoch keine Bewertungen

- Deloitte & Touche Consulting GroupDokument6 SeitenDeloitte & Touche Consulting Grouptyagi86Scribd67% (3)

- Allentown Materials CorporationDokument11 SeitenAllentown Materials CorporationSubhajit Mukherjee0% (1)

- House of TataDokument8 SeitenHouse of TataDhiraj KhatriNoch keine Bewertungen

- Knickknack: Case Study: Class: Red TEAM: 11Dokument7 SeitenKnickknack: Case Study: Class: Red TEAM: 11jhadarshnaNoch keine Bewertungen

- Transworld Xls460 Xls EngDokument6 SeitenTransworld Xls460 Xls EngAman Pawar0% (1)

- History I.M.PeiDokument26 SeitenHistory I.M.PeiVedasri RachaNoch keine Bewertungen

- Teaching Note - Customer Analytics at Big BasketDokument20 SeitenTeaching Note - Customer Analytics at Big BasketARPAN100% (4)

- Transworld Auto PartsDokument11 SeitenTransworld Auto PartsPulkit Jain100% (1)

- FM-07 Valuations, Mergers Acquisitions Question PaperDokument4 SeitenFM-07 Valuations, Mergers Acquisitions Question PaperSonu0% (1)

- ITC-Business StrategyDokument47 SeitenITC-Business StrategyAsad khan67% (6)

- TapDokument4 SeitenTaphasanNoch keine Bewertungen

- PV Technologies Case Analysis - Gaining Favorable Evaluation for Major ProjectDokument5 SeitenPV Technologies Case Analysis - Gaining Favorable Evaluation for Major Projectkaransangar100% (1)

- Template for assessing IPCSL's strategies to increase revenues and market shareDokument6 SeitenTemplate for assessing IPCSL's strategies to increase revenues and market shareSubhadra Haribabu0% (1)

- A5 - Indian ProductsDokument18 SeitenA5 - Indian ProductsVignesh nayakNoch keine Bewertungen

- Lego Case Questions and AnswersDokument8 SeitenLego Case Questions and AnswersFaizees100% (2)

- Group 10's Case Analysis: Digital Transformation at GEDokument13 SeitenGroup 10's Case Analysis: Digital Transformation at GEkarthikawarrier100% (2)

- TWA grp8Dokument10 SeitenTWA grp8Aryan Anand100% (1)

- STRATEGIC RESPONSE TO NEW COMPETITIONDokument6 SeitenSTRATEGIC RESPONSE TO NEW COMPETITIONANANTHA BHAIRAVI M100% (1)

- OTISLINE PresentationDokument5 SeitenOTISLINE PresentationRajgopal IyengarNoch keine Bewertungen

- D&T Case AnalysisDokument3 SeitenD&T Case AnalysisSagar Bansal100% (1)

- B2B - Group 3 - Jackson Case StudyDokument5 SeitenB2B - Group 3 - Jackson Case Studyriya agrawallaNoch keine Bewertungen

- Case#14 Analysis Group10Dokument7 SeitenCase#14 Analysis Group10Mohammad Aamir100% (1)

- Becton Dickinson and CompanyDokument19 SeitenBecton Dickinson and CompanyAmitSinghNoch keine Bewertungen

- Becton CaseDokument42 SeitenBecton CaseRaj Shekhar60% (5)

- GiveIndia's Online Marketing StrategyDokument2 SeitenGiveIndia's Online Marketing StrategyAryanshi Dubey0% (2)

- A.P. Møller - Maersk GroupDokument10 SeitenA.P. Møller - Maersk Groupsujeet palNoch keine Bewertungen

- Dabur Distribution NetworkDokument6 SeitenDabur Distribution Networkraja sinha100% (1)

- House of TataDokument36 SeitenHouse of TataHarsh Bhardwaj0% (1)

- Building Brand Infosys-Group 8Dokument4 SeitenBuilding Brand Infosys-Group 8Sauhard GuptaNoch keine Bewertungen

- Microsoft - ISB PM Challenge Campus RoundDokument11 SeitenMicrosoft - ISB PM Challenge Campus RoundNjNoch keine Bewertungen

- Case 4 Precise Software SolutionsDokument3 SeitenCase 4 Precise Software Solutionssaikat sarkarNoch keine Bewertungen

- House of TATA,1995: The Next Generation Group 2, Section A, PGP22Dokument7 SeitenHouse of TATA,1995: The Next Generation Group 2, Section A, PGP22satyakidutta007100% (1)

- SAP Brand Analysis: Ensuring Consistency WorldwideDokument3 SeitenSAP Brand Analysis: Ensuring Consistency WorldwideSachin SuryavanshiNoch keine Bewertungen

- " Bharat Forge LTD.": Group - KaizenDokument31 Seiten" Bharat Forge LTD.": Group - KaizenVijaylakshmi AgarwalNoch keine Bewertungen

- The Multichannel Challenge at Natura in Beauty and Personal CareDokument14 SeitenThe Multichannel Challenge at Natura in Beauty and Personal CareMaría José Chávez Estrada0% (1)

- TiVo Case StudyDokument3 SeitenTiVo Case StudyMuskan PuriNoch keine Bewertungen

- Xiameter - Debasish SahooDokument2 SeitenXiameter - Debasish SahooDebasish SahooNoch keine Bewertungen

- Xylys Case StudyDokument15 SeitenXylys Case StudyAbhigya Maheshwari100% (1)

- VW India's Digital Marketing Strategy to Overcome Industry SlowdownDokument14 SeitenVW India's Digital Marketing Strategy to Overcome Industry SlowdownAnonymous jFkV7Rz49Noch keine Bewertungen

- Case Analysis TIVODokument8 SeitenCase Analysis TIVOMuhammad Nasir0% (1)

- WEC Case AnalysisDokument15 SeitenWEC Case AnalysisAkanksha GuptaNoch keine Bewertungen

- It's A New Day Office 2007 CampaignDokument22 SeitenIt's A New Day Office 2007 Campaignnesninis100% (1)

- Transworld Auto Parts Case OverviewDokument2 SeitenTransworld Auto Parts Case OverviewFarhan ThaibNoch keine Bewertungen

- CTR3 M.FarhanThaibRiantoDokument5 SeitenCTR3 M.FarhanThaibRiantoFarhan ThaibNoch keine Bewertungen

- CTR3 M.FarhanThaibRiantoDokument5 SeitenCTR3 M.FarhanThaibRiantoFarhan ThaibNoch keine Bewertungen

- Ccoe Strategy FrameworkDokument14 SeitenCcoe Strategy FrameworkadebolaNoch keine Bewertungen

- PAnelDokument11 SeitenPAnelkiller dramaNoch keine Bewertungen

- SDDokument1 SeiteSDkiller dramaNoch keine Bewertungen

- Looper Height TagsDokument1 SeiteLooper Height Tagskiller dramaNoch keine Bewertungen

- Combined SPSS in Excel 456Dokument89 SeitenCombined SPSS in Excel 456killer dramaNoch keine Bewertungen

- Paper More-Excel SheetDokument133 SeitenPaper More-Excel Sheetkiller dramaNoch keine Bewertungen

- Boeing 777 ADokument3 SeitenBoeing 777 Akiller dramaNoch keine Bewertungen

- Key Takeaways From E&Y WebinarDokument2 SeitenKey Takeaways From E&Y Webinarkiller dramaNoch keine Bewertungen

- P&G's Organizational EvolutionDokument6 SeitenP&G's Organizational Evolutionkiller dramaNoch keine Bewertungen

- Syntax GG PlotDokument3 SeitenSyntax GG Plotkiller dramaNoch keine Bewertungen

- Nedbank Case Study - FinalDokument2 SeitenNedbank Case Study - Finalkiller dramaNoch keine Bewertungen

- Ucalgary 2013 Kano LienaDokument349 SeitenUcalgary 2013 Kano Lienakiller dramaNoch keine Bewertungen

- Oep SCMP A5 Minibrochure WebDokument8 SeitenOep SCMP A5 Minibrochure Webkiller dramaNoch keine Bewertungen

- Scale For EFA For Resilience ModelDokument9 SeitenScale For EFA For Resilience Modelkiller dramaNoch keine Bewertungen

- Doe PracticeDokument237 SeitenDoe Practicekiller dramaNoch keine Bewertungen

- Specification For - OGPCS008 (Online Grading System)Dokument1 SeiteSpecification For - OGPCS008 (Online Grading System)killer dramaNoch keine Bewertungen

- Type I and Type II Errror in ACCDokument3 SeitenType I and Type II Errror in ACCkiller dramaNoch keine Bewertungen

- Sqms QueryDokument2 SeitenSqms Querykiller dramaNoch keine Bewertungen

- Research Papers Ref 30th JanDokument33 SeitenResearch Papers Ref 30th Jankiller dramaNoch keine Bewertungen

- Executive Summary:: Sl. No. Areas Implications Under GSTDokument2 SeitenExecutive Summary:: Sl. No. Areas Implications Under GSTkiller dramaNoch keine Bewertungen

- LIC Zonal Grievance OfficersDokument1 SeiteLIC Zonal Grievance Officerskiller dramaNoch keine Bewertungen

- Manual For Building ANP Decision ModelsDokument84 SeitenManual For Building ANP Decision Modelskiller dramaNoch keine Bewertungen

- What Is The Difference Between Tier 1 Capital and Tier 2 Capital - InvestopediaDokument6 SeitenWhat Is The Difference Between Tier 1 Capital and Tier 2 Capital - Investopediakiller dramaNoch keine Bewertungen

- PH Case Mexico BOPDokument6 SeitenPH Case Mexico BOPkiller dramaNoch keine Bewertungen

- Reliance Trend Store ProjectDokument9 SeitenReliance Trend Store Projectkiller dramaNoch keine Bewertungen

- Macro Note BookDokument56 SeitenMacro Note Bookkiller dramaNoch keine Bewertungen

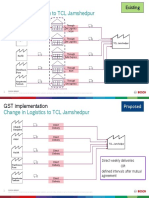

- Annexure 2 - Change in Logistics To TCL JamshedpurDokument2 SeitenAnnexure 2 - Change in Logistics To TCL Jamshedpurkiller dramaNoch keine Bewertungen

- Incomplete Solutions Case StudyDokument6 SeitenIncomplete Solutions Case Studykiller dramaNoch keine Bewertungen

- Randall's Advertising & Sales Promotion Case Study AnalysisDokument6 SeitenRandall's Advertising & Sales Promotion Case Study Analysiskiller dramaNoch keine Bewertungen

- Mo Os Best Post GST PDFDokument60 SeitenMo Os Best Post GST PDFkiller dramaNoch keine Bewertungen

- GST: A Metamorphic ReformDokument46 SeitenGST: A Metamorphic Reformkiller dramaNoch keine Bewertungen

- Shell Rimula R7 AD 5W-30: Performance, Features & Benefits Main ApplicationsDokument2 SeitenShell Rimula R7 AD 5W-30: Performance, Features & Benefits Main ApplicationsAji WibowoNoch keine Bewertungen

- NUC BIOS Update Readme PDFDokument3 SeitenNUC BIOS Update Readme PDFSuny Zany Anzha MayaNoch keine Bewertungen

- Assessment - Lesson 1Dokument12 SeitenAssessment - Lesson 1Charlynjoy AbañasNoch keine Bewertungen

- Marketing Case Study - MM1 (EPGPX02, GROUP-06)Dokument5 SeitenMarketing Case Study - MM1 (EPGPX02, GROUP-06)kaushal dhapareNoch keine Bewertungen

- Colorectal Disease - 2023 - Freund - Can Preoperative CT MR Enterography Preclude The Development of Crohn S Disease LikeDokument10 SeitenColorectal Disease - 2023 - Freund - Can Preoperative CT MR Enterography Preclude The Development of Crohn S Disease Likedavidmarkovic032Noch keine Bewertungen

- Reserve Management Parts I and II WBP Public 71907Dokument86 SeitenReserve Management Parts I and II WBP Public 71907Primo KUSHFUTURES™ M©QUEENNoch keine Bewertungen

- Ce QuizDokument2 SeitenCe QuizCidro Jake TyronNoch keine Bewertungen

- Southern Railway, Tiruchchirappalli: RC Guards Batch No: 1819045 Paper PresentationDokument12 SeitenSouthern Railway, Tiruchchirappalli: RC Guards Batch No: 1819045 Paper PresentationSathya VNoch keine Bewertungen

- Towards A Socially Responsible Management Control SystemDokument24 SeitenTowards A Socially Responsible Management Control Systemsavpap78Noch keine Bewertungen

- Rashi - Effusion CytDokument56 SeitenRashi - Effusion CytShruthi N.RNoch keine Bewertungen

- SSC CGL Tier 2 Quantitative Abilities 16-Nov-2020Dokument17 SeitenSSC CGL Tier 2 Quantitative Abilities 16-Nov-2020aNoch keine Bewertungen

- Brother LS2300 Sewing Machine Instruction ManualDokument96 SeitenBrother LS2300 Sewing Machine Instruction ManualiliiexpugnansNoch keine Bewertungen

- Gautam KDokument12 SeitenGautam Kgautam kayapakNoch keine Bewertungen

- F. nucleatum L-cysteine Desulfhydrase GeneDokument6 SeitenF. nucleatum L-cysteine Desulfhydrase GeneatikramadhaniNoch keine Bewertungen

- Doctrine of Double EffectDokument69 SeitenDoctrine of Double Effectcharu555Noch keine Bewertungen

- Deep Work Book - English ResumoDokument9 SeitenDeep Work Book - English ResumoJoão Pedro OnozatoNoch keine Bewertungen

- Cambridge IGCSE: Pakistan Studies 0448/01Dokument4 SeitenCambridge IGCSE: Pakistan Studies 0448/01Mehmood AlimNoch keine Bewertungen

- Ice-Cream ConesDokument6 SeitenIce-Cream ConesAlfonso El SabioNoch keine Bewertungen

- Tribal Ethics of Mizo and Ao NagasDokument8 SeitenTribal Ethics of Mizo and Ao NagasVincent TharteaNoch keine Bewertungen

- Manoj KR - KakatiDokument5 SeitenManoj KR - Kakatimanoj kakatiNoch keine Bewertungen

- DSME2051CDokument5 SeitenDSME2051Choi chingNoch keine Bewertungen

- The Sociopath's MantraDokument2 SeitenThe Sociopath's MantraStrategic ThinkerNoch keine Bewertungen