Das könnte Ihnen auch gefallen

- 2019 AwardsDokument88 Seiten2019 AwardsRishabh GuptaNoch keine Bewertungen

- Optimization with Multiple Objectives: Techniques and Applications in Radiation Therapy PlanningDokument17 SeitenOptimization with Multiple Objectives: Techniques and Applications in Radiation Therapy PlanningBarathNoch keine Bewertungen

- CV Template for Analyst Level ProfessionalDokument1 SeiteCV Template for Analyst Level ProfessionalRishabh GuptaNoch keine Bewertungen

- 12 Sales PromotionsDokument21 Seiten12 Sales PromotionsgamenikeNoch keine Bewertungen

- Intro To Social Entrepreneurship - Outline 17-19 v1Dokument3 SeitenIntro To Social Entrepreneurship - Outline 17-19 v1Rishabh GuptaNoch keine Bewertungen

- CamScanner Document ScansDokument52 SeitenCamScanner Document ScansRishabh GuptaNoch keine Bewertungen

- BAV Course OutlineDokument4 SeitenBAV Course OutlineRishabh GuptaNoch keine Bewertungen

- End-Term Exam Schedule - Term III 2017-19Dokument1 SeiteEnd-Term Exam Schedule - Term III 2017-19Rishabh GuptaNoch keine Bewertungen

- Material and Energy BalanceDokument23 SeitenMaterial and Energy BalanceSaurabh KumarNoch keine Bewertungen

- Singapore High Commission Authorised Visa Agents in KolkataDokument1 SeiteSingapore High Commission Authorised Visa Agents in KolkataRishabh GuptaNoch keine Bewertungen

- Analysis of Sports AnalyticsDokument5 SeitenAnalysis of Sports AnalyticsRishabh GuptaNoch keine Bewertungen

- Grades ModelDokument15 SeitenGrades ModelRishabh GuptaNoch keine Bewertungen

- Emotional Intelligence QuestiDokument4 SeitenEmotional Intelligence QuestiRishabh Gupta100% (1)

- Day2 TT ResultsDokument18 SeitenDay2 TT ResultsRishabh GuptaNoch keine Bewertungen

- QT2 Class Notes PDFDokument46 SeitenQT2 Class Notes PDFRishabh GuptaNoch keine Bewertungen

- Ch9 Solutions To The ExercisesDokument2 SeitenCh9 Solutions To The ExercisesRishabh GuptaNoch keine Bewertungen

- BRM Notes - 20180212154410Dokument52 SeitenBRM Notes - 20180212154410Rishabh GuptaNoch keine Bewertungen

- Briquettes IntroDokument1 SeiteBriquettes IntroRishabh GuptaNoch keine Bewertungen

- XLRI BMDokument246 SeitenXLRI BMSundaramNoch keine Bewertungen

- QT2 Class NotesDokument46 SeitenQT2 Class NotesRishabh GuptaNoch keine Bewertungen

- 3 Values HandoutDokument6 Seiten3 Values HandoutYatin AroraNoch keine Bewertungen

- 5 Learning HandoutDokument13 Seiten5 Learning HandoutRishabh GuptaNoch keine Bewertungen

- Linear Regression Reading Material 1Dokument13 SeitenLinear Regression Reading Material 1Rishabh GuptaNoch keine Bewertungen

- Iimu CSR Report 2017 Sep19 For WebDokument58 SeitenIimu CSR Report 2017 Sep19 For WebRishabh GuptaNoch keine Bewertungen

- Ping Pong Ek Aur Ek Gyarah: Smashing ChopstersDokument2 SeitenPing Pong Ek Aur Ek Gyarah: Smashing ChopstersRishabh GuptaNoch keine Bewertungen

- Avendus Live ProjectDokument2 SeitenAvendus Live ProjectRishabh GuptaNoch keine Bewertungen

- Chapter 01 - The Challenge of Corporate Ethics Today-September 26, 2017Dokument33 SeitenChapter 01 - The Challenge of Corporate Ethics Today-September 26, 2017Rishabh GuptaNoch keine Bewertungen

- Links ManacDokument2 SeitenLinks ManacRishabh GuptaNoch keine Bewertungen

- MicroDokument101 SeitenMicroPooja Ujjwal JainNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5782)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Income Taxation ExplainedDokument15 SeitenIncome Taxation ExplainedJustin Andre SiguanNoch keine Bewertungen

- Mepco Online BillDokument1 SeiteMepco Online BillMuhammad UmarNoch keine Bewertungen

- Bank statement with transaction detailsDokument3 SeitenBank statement with transaction detailsBokul0% (1)

- National Internal Revenue CodeDokument23 SeitenNational Internal Revenue Codeuserfriendly12345Noch keine Bewertungen

- Taxation Law & Practice Module-1Dokument298 SeitenTaxation Law & Practice Module-1swapbjspnNoch keine Bewertungen

- Comparative Study of Savings Account Service ChargesDokument18 SeitenComparative Study of Savings Account Service Chargesmanish121Noch keine Bewertungen

- NT Police Supplementary Benefit Scheme Annual ReportDokument41 SeitenNT Police Supplementary Benefit Scheme Annual ReportcaptovateNoch keine Bewertungen

- Petty Cash - Soe-Voucher-EmilyDokument7 SeitenPetty Cash - Soe-Voucher-EmilyMary LouellaNoch keine Bewertungen

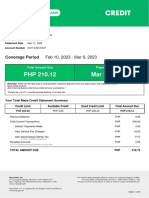

- MayaCredit SoA 2023MARDokument2 SeitenMayaCredit SoA 2023MARJan SaysonNoch keine Bewertungen

- To Be Filled Up by BIRDokument2 SeitenTo Be Filled Up by BIRmay1st200867% (6)

- ICICI Bank Savings Statement for January 2019Dokument3 SeitenICICI Bank Savings Statement for January 2019జెల్ల ఉమేష్ అను నేనుNoch keine Bewertungen

- Schedule of Benef Its: Savings Account Effective January 1, 2022Dokument2 SeitenSchedule of Benef Its: Savings Account Effective January 1, 2022Aniket DubeyNoch keine Bewertungen

- IT CalculatorDokument49 SeitenIT CalculatorMotheesh ReddyNoch keine Bewertungen

- Income Statement: Clymel Cebu Music SchoolDokument3 SeitenIncome Statement: Clymel Cebu Music SchoolLorn RobNoch keine Bewertungen

- Gu 5 Qgwar HZ DRMCTPDokument15 SeitenGu 5 Qgwar HZ DRMCTPVara Prasad AvulaNoch keine Bewertungen

- P Narendra Pay SlipDokument2 SeitenP Narendra Pay SlipBADI APPALARAJUNoch keine Bewertungen

- ICSE Fee Structure For The AY2022-2024Dokument2 SeitenICSE Fee Structure For The AY2022-2024Geethanjali d.nNoch keine Bewertungen

- Statement Aug 2013Dokument10 SeitenStatement Aug 2013berstuck100% (2)

- RMC 46-2008Dokument12 SeitenRMC 46-2008pja_14100% (4)

- Tax invoice for automotive plugsDokument1 SeiteTax invoice for automotive plugsChaudhary NitinNoch keine Bewertungen

- Tuition TableDokument2 SeitenTuition TableJerlin Orexy Ubeda GutierrezNoch keine Bewertungen

- Registered Post: On 29 Sep 2022 Vide This Officeletter No. 8926/07/E8 DT 29 Sep 2022. andDokument1 SeiteRegistered Post: On 29 Sep 2022 Vide This Officeletter No. 8926/07/E8 DT 29 Sep 2022. andSunil SalunkeNoch keine Bewertungen

- Deutsche Bank vs. CIR PDFDokument13 SeitenDeutsche Bank vs. CIR PDFPJ SLSRNoch keine Bewertungen

- Up Law Complex: Uggested Answers To The 2017 Bar Examination Questions in TaxationDokument9 SeitenUp Law Complex: Uggested Answers To The 2017 Bar Examination Questions in TaxationNissi JonnaNoch keine Bewertungen

- Phil. Guaranty Co. Taxation of Reinsurance Premiums Ceded AbroadDokument1 SeitePhil. Guaranty Co. Taxation of Reinsurance Premiums Ceded AbroadRhyz Taruc-ConsorteNoch keine Bewertungen

- Cosmote Mobile Telecomm Sa Greece 2021 PDFDokument1 SeiteCosmote Mobile Telecomm Sa Greece 2021 PDFGh UnlockersNoch keine Bewertungen

- EMS Grade 8 Control TestDokument4 SeitenEMS Grade 8 Control TestRiane van TonderNoch keine Bewertungen

- Statement of AccountDokument7 SeitenStatement of AccountAdventurous FreakNoch keine Bewertungen

- MCQ CA Final Fundamentals of Base Erosion and Profit ShiftingDokument4 SeitenMCQ CA Final Fundamentals of Base Erosion and Profit ShiftingAbdul Qayyum RazaNoch keine Bewertungen

- TQ1136035 Ack 20220319033835Dokument1 SeiteTQ1136035 Ack 20220319033835Mukesh YadavNoch keine Bewertungen