Das könnte Ihnen auch gefallen

- Merchandising Periodic SampleDokument14 SeitenMerchandising Periodic SampleYam Pinoy100% (2)

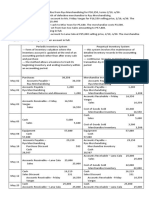

- Mira's School Supplies Store Financial AnalysisDokument1 SeiteMira's School Supplies Store Financial AnalysisMiguel Lulab100% (1)

- Santa Rosa Campus City of Santa Rosa, Laguna: Polytechnic University of The PhilippinesDokument19 SeitenSanta Rosa Campus City of Santa Rosa, Laguna: Polytechnic University of The PhilippinesareumNoch keine Bewertungen

- L2: The Accounting Cycle (AJPUAFCPR) : Accounting For Service and Merchandising Entities ACC11Dokument12 SeitenL2: The Accounting Cycle (AJPUAFCPR) : Accounting For Service and Merchandising Entities ACC11Rose LaureanoNoch keine Bewertungen

- ACCOUNTING ENTITY ASSUMPTION explainedDokument8 SeitenACCOUNTING ENTITY ASSUMPTION explainedJonalyn abesNoch keine Bewertungen

- 8 ACCT 1A&B MerchandisingDokument13 Seiten8 ACCT 1A&B MerchandisingShannon MojicaNoch keine Bewertungen

- Lesson 16: Accounting Practice SetDokument47 SeitenLesson 16: Accounting Practice SetMai Ruiz100% (1)

- Sem Plang Merchandising Periodic Problem With AnswersDokument21 SeitenSem Plang Merchandising Periodic Problem With Answerscole sprouse100% (1)

- General Journal: Date Account Titles and Explanation Ref Debit CreditDokument17 SeitenGeneral Journal: Date Account Titles and Explanation Ref Debit CreditPrecious NosaNoch keine Bewertungen

- Accounting cycle stepsDokument36 SeitenAccounting cycle stepsRodolfo CorpuzNoch keine Bewertungen

- Accounting Cycle of a Service BusinessDokument17 SeitenAccounting Cycle of a Service BusinessAmie Jane Miranda100% (1)

- Gelua Accounting - PlatoDokument57 SeitenGelua Accounting - PlatoJerome NatividadNoch keine Bewertungen

- Journalize the above transactions in the general journal of Bert PhotographyDokument24 SeitenJournalize the above transactions in the general journal of Bert PhotographyManuel Panotes Reantazo50% (2)

- Accounting Cycle of A Merchandising BusinessDokument21 SeitenAccounting Cycle of A Merchandising Businesszedrick edenNoch keine Bewertungen

- Fabm 1: Accounting For Merchandising ConcernDokument29 SeitenFabm 1: Accounting For Merchandising ConcernJan Vincent A. LadresNoch keine Bewertungen

- Test Bank 4Dokument5 SeitenTest Bank 4Jinx Cyrus RodilloNoch keine Bewertungen

- Accounting Worksheet Problem 4Dokument19 SeitenAccounting Worksheet Problem 4RELLON, James, M.100% (1)

- Tesda Perpetual GuidelinesDokument12 SeitenTesda Perpetual GuidelinesMichael Angelo Laguna Dela FuenteNoch keine Bewertungen

- Activity 2 - TB, W, CEDokument18 SeitenActivity 2 - TB, W, CEGina Calling Danao100% (1)

- Accounting For Merchandising Operations LongDokument2 SeitenAccounting For Merchandising Operations Longgk concepcionNoch keine Bewertungen

- Furniture Repair Shop Chart of AccountsDokument6 SeitenFurniture Repair Shop Chart of AccountsRechelleRuthM.DeiparineNoch keine Bewertungen

- Assignment November11 KylaAccountingDokument2 SeitenAssignment November11 KylaAccountingADRIANO, Glecy C.Noch keine Bewertungen

- AccDokument13 SeitenAccFrancis V MaestradoNoch keine Bewertungen

- Montrose Company May TransactionsDokument3 SeitenMontrose Company May TransactionsROB101512100% (1)

- Merchandising BusinessDokument11 SeitenMerchandising BusinessABM-AKRISTINE DELA CRUZNoch keine Bewertungen

- Merchandising - Journal EntriesDokument3 SeitenMerchandising - Journal EntriesBhea Ballesteros CabasanNoch keine Bewertungen

- Tesda Perpetual and Periodic Inventory SystemsDokument6 SeitenTesda Perpetual and Periodic Inventory Systemsnelia d. onteNoch keine Bewertungen

- Kea Sari Accounting 2.2Dokument2 SeitenKea Sari Accounting 2.2Joedy Mar MirandaNoch keine Bewertungen

- Problem Special JournalsDokument6 SeitenProblem Special JournalsCarmi Fecero100% (2)

- 5 Adjusting Entries For Prepaid ExpenseDokument4 Seiten5 Adjusting Entries For Prepaid Expenseapi-299265916Noch keine Bewertungen

- Ocean Laundry Shop Journal Entries & Trial BalanceDokument45 SeitenOcean Laundry Shop Journal Entries & Trial BalanceRachellyn Limentang100% (1)

- Fundamentals of Accountancy, Business, and Management 2: ExpectationDokument131 SeitenFundamentals of Accountancy, Business, and Management 2: ExpectationAngela Garcia100% (1)

- Journal entries for Lopez TradingDokument12 SeitenJournal entries for Lopez TradingŁei Silvestre100% (1)

- Perpetual Inventory Method PDFDokument13 SeitenPerpetual Inventory Method PDFthegianthony100% (1)

- Acc 102 PeriodicDokument16 SeitenAcc 102 Periodicgerald shepy100% (1)

- Trial Balance Accounting RecordsDokument8 SeitenTrial Balance Accounting RecordsKevin Espiritu100% (1)

- The Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingDokument12 SeitenThe Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingKim Patrick Victoria100% (1)

- ACCOUNTING CYCLE FOR MERCHANDISING CONCERNDokument30 SeitenACCOUNTING CYCLE FOR MERCHANDISING CONCERNMary100% (2)

- Or, Deposit Slip and Withdrawl SlipDokument4 SeitenOr, Deposit Slip and Withdrawl SlipJessica Rose AlbaracinNoch keine Bewertungen

- Recording Merchandising TransactionsDokument4 SeitenRecording Merchandising Transactionsacidreign50% (2)

- Basic Accounting ReviewerDokument4 SeitenBasic Accounting ReviewerRyan Dizon100% (1)

- ACC 102 Perpetual Inventory SystemDokument21 SeitenACC 102 Perpetual Inventory Systemice100% (1)

- 10-Step Accounting Cycle ExplainedDokument16 Seiten10-Step Accounting Cycle ExplainedSteffane Mae Sasutil100% (1)

- Perpetual Answer KeyDokument15 SeitenPerpetual Answer KeyAngel AmbrosioNoch keine Bewertungen

- Larry Jones Laundry Shop New FormatDokument18 SeitenLarry Jones Laundry Shop New FormatVincent Madrid100% (1)

- For Periodic Inventory System: What Is The CASE 2.1 CASE 2.2 CASE 2.3Dokument2 SeitenFor Periodic Inventory System: What Is The CASE 2.1 CASE 2.2 CASE 2.3LalaineNoch keine Bewertungen

- Closing EntriesDokument4 SeitenClosing Entriesapi-299265916Noch keine Bewertungen

- FABM 1 2ndQDokument67 SeitenFABM 1 2ndQBernard Baruiz0% (1)

- Integ Acc FinalsDokument201 SeitenInteg Acc FinalsBack upNoch keine Bewertungen

- Accounting defined as economic info systemDokument11 SeitenAccounting defined as economic info systemKyrzen NovillaNoch keine Bewertungen

- PROJECT-Service Dave 10 Adjustment. ..+-+Dokument48 SeitenPROJECT-Service Dave 10 Adjustment. ..+-+Dave Peralta0% (1)

- ACTG101 Adjusting EntriesDokument63 SeitenACTG101 Adjusting EntriesPrincess Ann PunoNoch keine Bewertungen

- Solution To Workshop No. 1Dokument10 SeitenSolution To Workshop No. 1Bryan PazNoch keine Bewertungen

- Comprehensive ProblemDokument2 SeitenComprehensive ProblemCeline Floranza100% (1)

- Exercise Periodic and PerpetualDokument4 SeitenExercise Periodic and PerpetualYally100% (1)

- Perpetual Vs Periodic Inventory SystemDokument9 SeitenPerpetual Vs Periodic Inventory SystemKhrystyna Kos100% (1)

- Completing of The Accounting Cycle PDFDokument15 SeitenCompleting of The Accounting Cycle PDFZairah HamanaNoch keine Bewertungen

- Accounting Principles: Second Canadian EditionDokument36 SeitenAccounting Principles: Second Canadian EditionMelody YayongNoch keine Bewertungen

- Accounting for Merchandising Firms: Income Statement and Cost of Goods SoldDokument15 SeitenAccounting for Merchandising Firms: Income Statement and Cost of Goods SoldRose Marie Recorte100% (1)

- Lecture, Chap. 5Dokument5 SeitenLecture, Chap. 5Moshe FarzanNoch keine Bewertungen

- Iphone 6s Manual User GuideDokument196 SeitenIphone 6s Manual User GuideSamuel ShepherdNoch keine Bewertungen

- Bookkeeping Quiz PDFDokument5 SeitenBookkeeping Quiz PDFEllie Cerino100% (1)

- Steering SystemDokument41 SeitenSteering SystemAnonymous 2k0o6az6lNoch keine Bewertungen

- Cooling SystemDokument38 SeitenCooling SystemAnonymous 2k0o6az6lNoch keine Bewertungen

- U C A O R A S: Nderstanding Omputers: N Verview For Ecords and Rchives TaffDokument73 SeitenU C A O R A S: Nderstanding Omputers: N Verview For Ecords and Rchives Taffnew2trackNoch keine Bewertungen

- U C A O R A S: Nderstanding Omputers: N Verview For Ecords and Rchives TaffDokument73 SeitenU C A O R A S: Nderstanding Omputers: N Verview For Ecords and Rchives Taffnew2trackNoch keine Bewertungen

- HPE 102: First Aid, Safety & CPR Syllabus Lecture Hours/Credits: 3/2Dokument7 SeitenHPE 102: First Aid, Safety & CPR Syllabus Lecture Hours/Credits: 3/2Anonymous 2k0o6az6lNoch keine Bewertungen

- Anatomy and PhysiologyDokument4 SeitenAnatomy and PhysiologyAnonymous 2k0o6az6lNoch keine Bewertungen

- Problem Solving & Decision MakingDokument10 SeitenProblem Solving & Decision MakingAnonymous 2k0o6az6lNoch keine Bewertungen

- Amo Plan 2014Dokument4 SeitenAmo Plan 2014kaps2385Noch keine Bewertungen

- ACM JournalDokument5 SeitenACM JournalThesisNoch keine Bewertungen

- Popular Tools CatalogDokument24 SeitenPopular Tools CatalogCarbide Processors IncNoch keine Bewertungen

- Gavrila Eduard 2Dokument6 SeitenGavrila Eduard 2Eduard Gabriel GavrilăNoch keine Bewertungen

- Export - Import Cycle - PPSXDokument15 SeitenExport - Import Cycle - PPSXMohammed IkramaliNoch keine Bewertungen

- Table of Contents and Executive SummaryDokument38 SeitenTable of Contents and Executive SummarySourav Ojha0% (1)

- 2019 ASME Section V ChangesDokument61 Seiten2019 ASME Section V Changesmanisami7036100% (4)

- Case Study - Help DocumentDokument2 SeitenCase Study - Help DocumentRahNoch keine Bewertungen

- Lay Out New PL Press QltyDokument68 SeitenLay Out New PL Press QltyDadan Hendra KurniawanNoch keine Bewertungen

- Network Theory - BASICS - : By: Mr. Vinod SalunkheDokument17 SeitenNetwork Theory - BASICS - : By: Mr. Vinod Salunkhevinod SALUNKHENoch keine Bewertungen

- Windows Keyboard Shortcuts OverviewDokument3 SeitenWindows Keyboard Shortcuts OverviewShaik Arif100% (1)

- Outstanding 12m Bus DrivelineDokument2 SeitenOutstanding 12m Bus DrivelineArshad ShaikhNoch keine Bewertungen

- VFD ManualDokument187 SeitenVFD ManualgpradiptaNoch keine Bewertungen

- Book 7 More R-Controlled-VowelsDokument180 SeitenBook 7 More R-Controlled-VowelsPolly Mark100% (1)

- Offshore Wind Turbine 6mw Robust Simple EfficientDokument4 SeitenOffshore Wind Turbine 6mw Robust Simple EfficientCristian Jhair PerezNoch keine Bewertungen

- Löwenstein Medical: Intensive Care VentilationDokument16 SeitenLöwenstein Medical: Intensive Care VentilationAlina Pedraza100% (1)

- 1 Univalent Functions The Elementary Theory 2018Dokument12 Seiten1 Univalent Functions The Elementary Theory 2018smpopadeNoch keine Bewertungen

- Shell Omala S2 G150 DatasheetDokument3 SeitenShell Omala S2 G150 Datasheetphankhoa83-1Noch keine Bewertungen

- Contract To Sell LansanganDokument2 SeitenContract To Sell LansanganTet BuanNoch keine Bewertungen

- Classification of Methods of MeasurementsDokument60 SeitenClassification of Methods of MeasurementsVenkat Krishna100% (2)

- EGMM - Training Partner MOUDokument32 SeitenEGMM - Training Partner MOUShaik HussainNoch keine Bewertungen

- Wei Et Al 2016Dokument7 SeitenWei Et Al 2016Aline HunoNoch keine Bewertungen

- MR15 Mechanical Engineering SyllabusDokument217 SeitenMR15 Mechanical Engineering Syllabusramji_kkpNoch keine Bewertungen

- ABRAMS M H The Fourth Dimension of A PoemDokument17 SeitenABRAMS M H The Fourth Dimension of A PoemFrancyne FrançaNoch keine Bewertungen

- An Improved Ant Colony Algorithm and Its ApplicatiDokument10 SeitenAn Improved Ant Colony Algorithm and Its ApplicatiI n T e R e Y eNoch keine Bewertungen

- Value Chain AnalysisDokument4 SeitenValue Chain AnalysisnidamahNoch keine Bewertungen

- Design Your Loyalty Program in 2 WeeksDokument53 SeitenDesign Your Loyalty Program in 2 WeeksLorena TacuryNoch keine Bewertungen

- Reaction CalorimetryDokument7 SeitenReaction CalorimetrySankar Adhikari100% (1)

- Evolution BrochureDokument4 SeitenEvolution Brochurelucas28031978Noch keine Bewertungen

- METRIC_ENGLISHDokument14 SeitenMETRIC_ENGLISHKehinde AdebayoNoch keine Bewertungen