Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- 6 01 11Dokument36 Seiten6 01 11grapevineNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Rational-Emotive Behaviour Therapy (Rebt)Dokument11 SeitenRational-Emotive Behaviour Therapy (Rebt)Sheralena Mohd RasidNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Vector Borne DiseasesDokument16 SeitenVector Borne Diseasesanon_931122078Noch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Restoracion Del Organismo Humano 2 de 2Dokument56 SeitenRestoracion Del Organismo Humano 2 de 2Eduardo UribeNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Shell Gadus S3 Wirerope T: Performance, Features & Benefits Main ApplicationsDokument2 SeitenShell Gadus S3 Wirerope T: Performance, Features & Benefits Main ApplicationssfkcrcnNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- VAL-SV-E0163-P PCBA Depanelization Router Elite Machine Validation Plan - Edy-29 Nov (CK)Dokument8 SeitenVAL-SV-E0163-P PCBA Depanelization Router Elite Machine Validation Plan - Edy-29 Nov (CK)arumNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hydrogen Peroxide Market Analysis and Segment Forecast To 2028Dokument103 SeitenHydrogen Peroxide Market Analysis and Segment Forecast To 2028Khiết NguyênNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Diaper Decoder Poster v2Dokument1 SeiteDiaper Decoder Poster v2abhiNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Health 8Dokument319 SeitenHealth 8Anngela Arevalo BarcenasNoch keine Bewertungen

- Sample Cbjip Book of Barangay Kauswagan 1Dokument38 SeitenSample Cbjip Book of Barangay Kauswagan 1Johana Pinagayao AngkadNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Health and Safety in The Kitchen: Lesson 8Dokument18 SeitenHealth and Safety in The Kitchen: Lesson 8Mary Grace Lamarroza RosagaranNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Motivation PDFDokument1 SeiteMotivation PDFAnonymous tBxCPAEX7SNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Mapil Civil Engineering ConstructionDokument2 SeitenMapil Civil Engineering ConstructionakilaNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Juvenile Justice Act 2015 8460163.ppsxDokument20 SeitenJuvenile Justice Act 2015 8460163.ppsxKiran KumarNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Estudiosen Biodiversidad Volumen I2015Dokument252 SeitenEstudiosen Biodiversidad Volumen I2015Margarita FONoch keine Bewertungen

- The IASP Classification of Chronic Pain For.10Dokument6 SeitenThe IASP Classification of Chronic Pain For.10hzol83Noch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Hyper CvadDokument5 SeitenHyper CvadAmr MuhammedNoch keine Bewertungen

- Thesis Protocol Final SarangDokument26 SeitenThesis Protocol Final SarangRaj KotichaNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- A Brief About Legal Services Authorities Act, 1987Dokument3 SeitenA Brief About Legal Services Authorities Act, 1987MINNU MINHAZNoch keine Bewertungen

- The Bethesda System For Reporting Cervical Cytolog PDFDokument359 SeitenThe Bethesda System For Reporting Cervical Cytolog PDFsurekhaNoch keine Bewertungen

- ICAO Manual Doc 9984 1st Edition Alltext en Published March 2013Dokument54 SeitenICAO Manual Doc 9984 1st Edition Alltext en Published March 2013Disability Rights Alliance67% (3)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Past ContinuousDokument2 SeitenPast ContinuousJoaquin GabilondoNoch keine Bewertungen

- The Tongue - Facts, Function & Diseases - Live SciencerDokument12 SeitenThe Tongue - Facts, Function & Diseases - Live SciencerImtiax LaghariNoch keine Bewertungen

- Sample Mental Health Treatment PlanDokument3 SeitenSample Mental Health Treatment PlanCordelia Kpaduwa100% (4)

- Themythofmultitasking Rosen PDFDokument6 SeitenThemythofmultitasking Rosen PDFyeni marcela montañaNoch keine Bewertungen

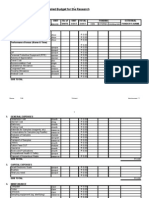

- Proposed Research BudgetDokument3 SeitenProposed Research BudgetAndreMostertNoch keine Bewertungen

- The Independent 21 February 2016Dokument60 SeitenThe Independent 21 February 2016artedlcNoch keine Bewertungen

- Insurance Plan HDFCDokument11 SeitenInsurance Plan HDFCniranjan sahuNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Exercise For Specific Postural Variations in Pistol Shooting Part 2Dokument3 SeitenExercise For Specific Postural Variations in Pistol Shooting Part 2kholamonNoch keine Bewertungen

- Gender Differences in AKI To CKD TransitionDokument13 SeitenGender Differences in AKI To CKD TransitionNatasha AlbaShakiraNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)