Das könnte Ihnen auch gefallen

- EMR Inv Day 2022 SlidesDokument99 SeitenEMR Inv Day 2022 SlidesXDL1100% (2)

- Balance Sheet StructuresVon EverandBalance Sheet StructuresAnthony N BirtsNoch keine Bewertungen

- Iso SampleDokument14 SeitenIso Samplemritunjay100% (2)

- Investment Banking Pitchbook TemplateDokument30 SeitenInvestment Banking Pitchbook TemplateVũ Hoàng AnhNoch keine Bewertungen

- Sap MDG GuideDokument10 SeitenSap MDG GuideAnonymous 1WXZc0j100% (1)

- Fabm2 q1 Mod5 Part-1-AnalysisDokument21 SeitenFabm2 q1 Mod5 Part-1-AnalysisAmber Dela Cruz100% (2)

- MS - Good Losses, Bad LossesDokument13 SeitenMS - Good Losses, Bad LossesResearch ReportsNoch keine Bewertungen

- Cost Volume Profit AnalysisDokument18 SeitenCost Volume Profit AnalysisLea GaacNoch keine Bewertungen

- Question Results: (Skipped)Dokument39 SeitenQuestion Results: (Skipped)ganesanmani198567% (3)

- Cross Docking ConfigurationDokument16 SeitenCross Docking ConfigurationRam Mani50% (2)

- GD 4Q21 Earnings Highlights-and-Outlook-FinalDokument13 SeitenGD 4Q21 Earnings Highlights-and-Outlook-Finals95qgd9rmjNoch keine Bewertungen

- Utb AnnualReport09Dokument60 SeitenUtb AnnualReport09Wilson LarbiNoch keine Bewertungen

- Canon Annual Report 2019Dokument94 SeitenCanon Annual Report 2019Venkatesan KanagarajanNoch keine Bewertungen

- Nyse FFG 2010Dokument5 SeitenNyse FFG 2010Bijoy AhmedNoch keine Bewertungen

- Yahoo! Inc.: Q3'10 Financial HighlightsDokument24 SeitenYahoo! Inc.: Q3'10 Financial HighlightsJay YarowNoch keine Bewertungen

- Yahoo! Inc.: Q3'10 Financial HighlightsDokument24 SeitenYahoo! Inc.: Q3'10 Financial HighlightsTechCrunchNoch keine Bewertungen

- Canon Annual Report 2018Dokument98 SeitenCanon Annual Report 2018olga domrachevaNoch keine Bewertungen

- Q4 & FY '10 Results: Paris - February 23, 2011Dokument37 SeitenQ4 & FY '10 Results: Paris - February 23, 2011mukul_goyalinNoch keine Bewertungen

- 4 - 2021 Consolidated Financial StatementsDokument58 Seiten4 - 2021 Consolidated Financial Statementsasmita23840Noch keine Bewertungen

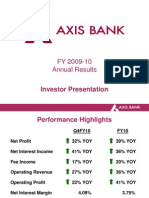

- FY 2009-10 Annual Results: Investor PresentationDokument34 SeitenFY 2009-10 Annual Results: Investor PresentationDujesh KardamNoch keine Bewertungen

- EPM What Is New 16.12 UpdateDokument37 SeitenEPM What Is New 16.12 UpdateKumar MNoch keine Bewertungen

- Focused On Outcomes: Rated By: PACRA & VISDokument234 SeitenFocused On Outcomes: Rated By: PACRA & VISFahimNoch keine Bewertungen

- NYSE LEVI 2021 CopyableDokument166 SeitenNYSE LEVI 2021 Copyableshrimp shrimpNoch keine Bewertungen

- Q2 2020 Earnings Presentation American Tower CorporationDokument25 SeitenQ2 2020 Earnings Presentation American Tower CorporationKenya ToledoNoch keine Bewertungen

- Article GoodlossesbadlossesDokument13 SeitenArticle GoodlossesbadlossesRatan Lal SharmaNoch keine Bewertungen

- ROK AR Web 13Dokument88 SeitenROK AR Web 13Niraj TakalkhedeNoch keine Bewertungen

- Task 2 TemplateDokument2 SeitenTask 2 TemplateGauravVeeruSinghNoch keine Bewertungen

- CanadiansForTaxFairness eDokument7 SeitenCanadiansForTaxFairness ejuliawilma123321Noch keine Bewertungen

- Chapter 2 - Analysis of Financial StatementDokument43 SeitenChapter 2 - Analysis of Financial StatementtheputeriizzahNoch keine Bewertungen

- 4Q2022 ResultsPresentation 1mar2023 FinalDokument14 Seiten4Q2022 ResultsPresentation 1mar2023 FinalCharlie CalitrokeNoch keine Bewertungen

- EFIN 519 ( (Bank Fund Management) : On "Key Performance Indicator (KPI) "Dokument22 SeitenEFIN 519 ( (Bank Fund Management) : On "Key Performance Indicator (KPI) "anika moniNoch keine Bewertungen

- Canon Annual Report 2017Dokument94 SeitenCanon Annual Report 2017MedisonicFlorAtalayaNoch keine Bewertungen

- 2017 Preliminary Results AnnouncementDokument143 Seiten2017 Preliminary Results AnnouncementAviva GroupNoch keine Bewertungen

- Bringing More To The Table.: 2006 Annual ReportDokument93 SeitenBringing More To The Table.: 2006 Annual Reportapi-3697911Noch keine Bewertungen

- 1.0 AMMB Investor Presentation - FY17 31.5.17fDokument62 Seiten1.0 AMMB Investor Presentation - FY17 31.5.17fAli Gokhan KocanNoch keine Bewertungen

- MERALCO Annual Report 2011Dokument162 SeitenMERALCO Annual Report 2011Anonymous ic2CDkFNoch keine Bewertungen

- Fy22 Full Year Results PresentationDokument30 SeitenFy22 Full Year Results Presentation李冰Noch keine Bewertungen

- PNRA Panera Bread 2016 Annual Shareholder PresentationDokument46 SeitenPNRA Panera Bread 2016 Annual Shareholder PresentationAla BasterNoch keine Bewertungen

- Session 2 - Financial Statement AnalysisDokument43 SeitenSession 2 - Financial Statement Analysisluoyifei1988Noch keine Bewertungen

- Paccar Ar 2012Dokument94 SeitenPaccar Ar 2012Quang PhanNoch keine Bewertungen

- Joint Venture Management - Sales Positioning - EN20210624Dokument41 SeitenJoint Venture Management - Sales Positioning - EN20210624pramodpatidar2018Noch keine Bewertungen

- Applied Optoelectronics Inc REPORT 11.29.23Dokument3 SeitenApplied Optoelectronics Inc REPORT 11.29.23physicallen1791Noch keine Bewertungen

- Presentation of SandlerDokument16 SeitenPresentation of SandlerAdorvis IncNoch keine Bewertungen

- Enova IR Enova Investor Presentation July 2022Dokument36 SeitenEnova IR Enova Investor Presentation July 2022Dov LeviNoch keine Bewertungen

- YHOO Q409EarningsPresentation FinalDokument22 SeitenYHOO Q409EarningsPresentation Finalhblodget6728Noch keine Bewertungen

- Constellation Software Inc.: To Our ShareholdersDokument5 SeitenConstellation Software Inc.: To Our ShareholdersSugar RayNoch keine Bewertungen

- Accenture EPM PoVDokument20 SeitenAccenture EPM PoVRendy DjunaediNoch keine Bewertungen

- Dynashears CaseDokument5 SeitenDynashears CaseScribdTranslationsNoch keine Bewertungen

- Wipro Ratio AnalysisDokument32 SeitenWipro Ratio Analysisvaibhavs_1009Noch keine Bewertungen

- LOTOS Group Databook 31032022Dokument34 SeitenLOTOS Group Databook 31032022centrumatNoch keine Bewertungen

- Drug Discovery & Development For The World Market From India: How RealDokument20 SeitenDrug Discovery & Development For The World Market From India: How RealRicky TiwariNoch keine Bewertungen

- ZOES WB Presentation June17 (1) 2017Dokument29 SeitenZOES WB Presentation June17 (1) 2017Ala BasterNoch keine Bewertungen

- FM - Wesfarmers - Annual ReportDokument184 SeitenFM - Wesfarmers - Annual Reportw4w4w4w4w4Noch keine Bewertungen

- Australia Investment Banking Review First Quarter 2021: Refinitiv Deals IntelligenceDokument15 SeitenAustralia Investment Banking Review First Quarter 2021: Refinitiv Deals IntelligenceYohei John MikawaNoch keine Bewertungen

- AGibson 12e Ch05Dokument36 SeitenAGibson 12e Ch05Jamroz KhanNoch keine Bewertungen

- Model Solution: Company-Operated RestaurantsDokument16 SeitenModel Solution: Company-Operated Restaurantspranjal92pandeyNoch keine Bewertungen

- Fourth Quarter 2010 Conference Call: February 10, 2011Dokument33 SeitenFourth Quarter 2010 Conference Call: February 10, 2011bisht789Noch keine Bewertungen

- Living Up To The Promise: Analyst MeetDokument11 SeitenLiving Up To The Promise: Analyst MeetNirmal ShahNoch keine Bewertungen

- Pace BrochureDokument8 SeitenPace BrochureHimanshuNoch keine Bewertungen

- MM Fin HighlightsDokument1 SeiteMM Fin HighlightsAbhinavHarshalNoch keine Bewertungen

- Financial Results Briefing Material For FY2019: April 1, 2018 To March 31, 2019Dokument30 SeitenFinancial Results Briefing Material For FY2019: April 1, 2018 To March 31, 2019choiand1Noch keine Bewertungen

- Braced for Impact: Reforming Kazakhstan's National Financial Holding for Development Effectiveness and Market CreationVon EverandBraced for Impact: Reforming Kazakhstan's National Financial Holding for Development Effectiveness and Market CreationNoch keine Bewertungen

- Developing A Marketing Plan: Name of The StudentDokument14 SeitenDeveloping A Marketing Plan: Name of The StudentFadhil WigunaNoch keine Bewertungen

- 2021 UTS JawabanDokument8 Seiten2021 UTS JawabanAdam FitraNoch keine Bewertungen

- Golds Gym Marketing Audit Report SHDokument16 SeitenGolds Gym Marketing Audit Report SHErikaOruaAngelesNoch keine Bewertungen

- SAIL Quiz FormatDokument16 SeitenSAIL Quiz FormatZulfiqar AliNoch keine Bewertungen

- UNEP POPS BATBEP GUID GUIDELINES 2019 7.enDokument69 SeitenUNEP POPS BATBEP GUID GUIDELINES 2019 7.enAmpiraNoch keine Bewertungen

- Accredited Supply Chain Professional (Ascp)Dokument5 SeitenAccredited Supply Chain Professional (Ascp)Mohammad Cipto SugionoNoch keine Bewertungen

- Vendor Managed InventoryDokument10 SeitenVendor Managed InventoryAnish DalmiaNoch keine Bewertungen

- CRM and ERPDokument11 SeitenCRM and ERPnithin rajeevanNoch keine Bewertungen

- IBM E-Business ModelDokument16 SeitenIBM E-Business ModelSyed Irfan AliNoch keine Bewertungen

- JD of SAP PP or QM ConsultantDokument2 SeitenJD of SAP PP or QM ConsultantRafi ShaikNoch keine Bewertungen

- Name Muhammad Talal Akhtar Roll No. 201360284 Subject Principal of Marketing Section MKT201F Company NestléDokument3 SeitenName Muhammad Talal Akhtar Roll No. 201360284 Subject Principal of Marketing Section MKT201F Company NestléMuhammad Talal AzeemNoch keine Bewertungen

- Chapter 4 Value ChainDokument24 SeitenChapter 4 Value ChainashlyNoch keine Bewertungen

- PS6 2Dokument3 SeitenPS6 2doanquynhnth1019Noch keine Bewertungen

- India PCN Course Exam FeeDokument3 SeitenIndia PCN Course Exam FeeJames100% (1)

- Kumwell Exothermic WeldingDokument93 SeitenKumwell Exothermic WeldingAgus Nur SetiawanNoch keine Bewertungen

- Senior High School Learning Materials in Entrepreneurship: Expenses Paid For Goods or ServicesDokument4 SeitenSenior High School Learning Materials in Entrepreneurship: Expenses Paid For Goods or ServicesShayne BonayonNoch keine Bewertungen

- Let'S Start With Analyzing The FedexDokument3 SeitenLet'S Start With Analyzing The FedexGumbat KPKNoch keine Bewertungen

- Value Stream Mapping VSM A Key Tool For Execution of Lean PrinciplesDokument5 SeitenValue Stream Mapping VSM A Key Tool For Execution of Lean PrinciplesJustformedia JustformediaNoch keine Bewertungen

- Chap 17Dokument29 SeitenChap 17N.S.RavikumarNoch keine Bewertungen

- IGNOU MBA MS-05 Solved AssignmentDokument16 SeitenIGNOU MBA MS-05 Solved AssignmenttobinsNoch keine Bewertungen

- Heckscher-Ohlin Theory (Factor Proportions Theory)Dokument4 SeitenHeckscher-Ohlin Theory (Factor Proportions Theory)Mikeairah BlanquiscoNoch keine Bewertungen

- Data Transfer Workbench - SAP HelpDokument21 SeitenData Transfer Workbench - SAP HelpAnuradha SreedharagaddaNoch keine Bewertungen

- Arthurrooney 1995Dokument11 SeitenArthurrooney 1995Teodora Maria Deseaga100% (1)

- Assignment MarketingDokument10 SeitenAssignment MarketingAinul MardhiahNoch keine Bewertungen

- Chapter 1 What Is PRDokument17 SeitenChapter 1 What Is PROnetaa Martin MartinNoch keine Bewertungen