Das könnte Ihnen auch gefallen

- Group Assignment - Group 4Dokument24 SeitenGroup Assignment - Group 4Pranav Kaushal100% (1)

- Indivisual Assignment - Small Finance BanksDokument12 SeitenIndivisual Assignment - Small Finance BanksPranav KaushalNoch keine Bewertungen

- Editing CodingDokument20 SeitenEditing CodingPranav KaushalNoch keine Bewertungen

- Session 3Dokument10 SeitenSession 3Pranav KaushalNoch keine Bewertungen

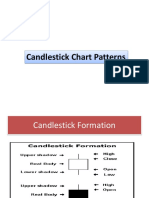

- Candlestick Chart PatternsDokument20 SeitenCandlestick Chart PatternsPranav Kaushal100% (2)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Mark Scheme Big Cat FactsDokument3 SeitenMark Scheme Big Cat FactsHuyền MyNoch keine Bewertungen

- Design & Evaluation in The Real World: Communicators & Advisory SystemsDokument13 SeitenDesign & Evaluation in The Real World: Communicators & Advisory Systemsdivya kalyaniNoch keine Bewertungen

- Diplomatic Quarter New Marriott Hotel & Executive ApartmentsDokument1 SeiteDiplomatic Quarter New Marriott Hotel & Executive Apartmentsconsultnadeem70Noch keine Bewertungen

- Pugh MatrixDokument18 SeitenPugh MatrixSulaiman Khan0% (1)

- Nutrition and Diet Therapy ExaminationDokument8 SeitenNutrition and Diet Therapy ExaminationIrwan M. Iskober100% (3)

- Chapter (1) The Accounting EquationDokument46 SeitenChapter (1) The Accounting Equationtunlinoo.067433100% (3)

- Doloran Auxilliary PrayersDokument4 SeitenDoloran Auxilliary PrayersJosh A.Noch keine Bewertungen

- Money Management Behavior and Spending Behavior Among Working Professionals in Silang, CaviteDokument8 SeitenMoney Management Behavior and Spending Behavior Among Working Professionals in Silang, CaviteAshley JoyceNoch keine Bewertungen

- FSR 2017-2018 KNL CircleDokument136 SeitenFSR 2017-2018 KNL CircleparthaNoch keine Bewertungen

- Grunig J, Grunig L. Public Relations in Strategic Management and Strategic Management of Public RelationsDokument20 SeitenGrunig J, Grunig L. Public Relations in Strategic Management and Strategic Management of Public RelationsjuanNoch keine Bewertungen

- BattleRope Ebook FinalDokument38 SeitenBattleRope Ebook FinalAnthony Dinicolantonio100% (1)

- Schmitt Allik 2005 ISDP Self Esteem - 000 PDFDokument20 SeitenSchmitt Allik 2005 ISDP Self Esteem - 000 PDFMariana KapetanidouNoch keine Bewertungen

- Week 4 CasesDokument38 SeitenWeek 4 CasesJANNNoch keine Bewertungen

- Dollar Unit SamplingDokument7 SeitenDollar Unit SamplingAndriatsirihasinaNoch keine Bewertungen

- The Concise 48 Laws of Power PDFDokument203 SeitenThe Concise 48 Laws of Power PDFkaran kamath100% (1)

- Media Kit (Viet)Dokument2 SeitenMedia Kit (Viet)Nguyen Ho Thien DuyNoch keine Bewertungen

- Reseller Handbook 2019 v1Dokument16 SeitenReseller Handbook 2019 v1Jennyfer SantosNoch keine Bewertungen

- Position Paper Guns Dont Kill People Final DraftDokument6 SeitenPosition Paper Guns Dont Kill People Final Draftapi-273319954Noch keine Bewertungen

- 479f3df10a8c0mathsproject QuadrilateralsDokument18 Seiten479f3df10a8c0mathsproject QuadrilateralsAnand PrakashNoch keine Bewertungen

- Tate J. Hedtke SPED 608 Assignment #6 Standard # 8 Cross Categorical Special Education/ Learning Disabilities Artifact SummaryDokument5 SeitenTate J. Hedtke SPED 608 Assignment #6 Standard # 8 Cross Categorical Special Education/ Learning Disabilities Artifact Summaryapi-344731850Noch keine Bewertungen

- Public Service: P2245m-PorkDokument3 SeitenPublic Service: P2245m-PorkDaniela Ellang ManuelNoch keine Bewertungen

- A Review of Cassiterite Beneficiation PraticesDokument23 SeitenA Review of Cassiterite Beneficiation PraticesLevent ErgunNoch keine Bewertungen

- Philippine Psychometricians Licensure Exam RevieweDokument1 SeitePhilippine Psychometricians Licensure Exam RevieweKristelle Mae C. Azucenas0% (1)

- 10 Problems of Philosophy EssayDokument3 Seiten10 Problems of Philosophy EssayRandy MarshNoch keine Bewertungen

- Parallels of Stoicism and KalamDokument95 SeitenParallels of Stoicism and KalamLDaggersonNoch keine Bewertungen

- Ant Colony AlgorithmDokument11 SeitenAnt Colony Algorithmjaved765Noch keine Bewertungen

- Kepimpinan BerwawasanDokument18 SeitenKepimpinan BerwawasanandrewanumNoch keine Bewertungen

- SDLC Review ChecklistDokument4 SeitenSDLC Review Checklistmayank govilNoch keine Bewertungen

- Of Bones and Buddhas Contemplation of TH PDFDokument215 SeitenOf Bones and Buddhas Contemplation of TH PDFCNoch keine Bewertungen

- K 46 Compact Spinning Machine Brochure 2530-V3 75220 Original English 75220Dokument28 SeitenK 46 Compact Spinning Machine Brochure 2530-V3 75220 Original English 75220Pradeep JainNoch keine Bewertungen