Das könnte Ihnen auch gefallen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Hybrid Vehicle ToyotaDokument30 SeitenHybrid Vehicle ToyotaAdf TrendNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

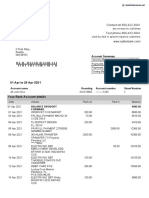

- Sutton Bank StatementDokument2 SeitenSutton Bank StatementNadiia AvetisianNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- 617 NP BookletDokument77 Seiten617 NP BookletDexie Cabañelez ManahanNoch keine Bewertungen

- Understanding EntrepreneurshipDokument277 SeitenUnderstanding Entrepreneurshiphannaatnafu100% (1)

- Joint Venture AgreementDokument7 SeitenJoint Venture AgreementFirman HamdanNoch keine Bewertungen

- Frost & SullivanDokument25 SeitenFrost & SullivanAnonymous JyOeaZNiGBNoch keine Bewertungen

- HR PoliciesDokument129 SeitenHR PoliciesAjeet ThounaojamNoch keine Bewertungen

- Strategy Management For HotelDokument14 SeitenStrategy Management For HotelkamleshmistriNoch keine Bewertungen

- Algorithmic Market Making StrategiesDokument34 SeitenAlgorithmic Market Making Strategiessahand100% (1)

- Red Bull FinalDokument28 SeitenRed Bull FinalYousaf Haroon Yousafzai0% (1)

- Askari Aviation Services Marketing ReportDokument66 SeitenAskari Aviation Services Marketing Reportsyed usman wazir100% (1)

- Core Complexities Bharat SyntheticsDokument4 SeitenCore Complexities Bharat SyntheticsRohit SharmaNoch keine Bewertungen

- Consumer BehaviorDokument18 SeitenConsumer Behaviormayur6790Noch keine Bewertungen

- Business ResearchDokument8 SeitenBusiness ResearchDhrumil GadariaNoch keine Bewertungen

- Simple GST Invoice Format in ExcelDokument2 SeitenSimple GST Invoice Format in ExcelsadnNoch keine Bewertungen

- Triton Valves LTDDokument5 SeitenTriton Valves LTDspvengi100% (1)

- Health Mitra PamphletDokument2 SeitenHealth Mitra Pamphletharshavardhanak23Noch keine Bewertungen

- Market Visit Ing ReportDokument3 SeitenMarket Visit Ing ReportMr. JahirNoch keine Bewertungen

- Sustainable Space Exploration?Dokument11 SeitenSustainable Space Exploration?Linda BillingsNoch keine Bewertungen

- RMC 17-02Dokument4 SeitenRMC 17-02racheltanuy6557Noch keine Bewertungen

- Dadar To Nasik Road TrainsDokument1 SeiteDadar To Nasik Road TrainsAbhishek MojadNoch keine Bewertungen

- Understanding CTC and Your Salary BreakupDokument2 SeitenUnderstanding CTC and Your Salary Breakupshannbaby22Noch keine Bewertungen

- Appendix 'A' To NITDokument8 SeitenAppendix 'A' To NITAbhishekNoch keine Bewertungen

- SWOT AnalysisDokument12 SeitenSWOT AnalysisSam LaiNoch keine Bewertungen

- TYS 2007 To 2019 AnswersDokument380 SeitenTYS 2007 To 2019 Answersshakthee sivakumarNoch keine Bewertungen

- Outward Remittance Form PDFDokument2 SeitenOutward Remittance Form PDFAbhishek GuptaNoch keine Bewertungen

- Vertical and Horizontal IntegrationDokument11 SeitenVertical and Horizontal IntegrationDone and DustedNoch keine Bewertungen

- Assignment 1Dokument13 SeitenAssignment 1Muhammad Asim Hafeez ThindNoch keine Bewertungen

- Tata Vistara - Agency PitchDokument27 SeitenTata Vistara - Agency PitchNishant Prakash0% (1)

- Aggregate Demand and Aggregate Supply PDFDokument18 SeitenAggregate Demand and Aggregate Supply PDFAsif WarsiNoch keine Bewertungen