Das könnte Ihnen auch gefallen

- Fin Acc Valix PDFDokument58 SeitenFin Acc Valix PDFKyla Renz de LeonNoch keine Bewertungen

- 4 InventoriesDokument5 Seiten4 InventoriesandreamrieNoch keine Bewertungen

- Financial Asset at Amortized CostDokument14 SeitenFinancial Asset at Amortized CostLorenzo Diaz DipadNoch keine Bewertungen

- BPS Prelim Exam KADokument19 SeitenBPS Prelim Exam KASheena Calderon100% (1)

- Investment in Associate ReviewerDokument18 SeitenInvestment in Associate ReviewerAl-Rafzahir Bandingan80% (5)

- Retake: Financial Accounting and ReportingDokument21 SeitenRetake: Financial Accounting and ReportingJan ryanNoch keine Bewertungen

- This Study Resource Was: Logo HereDokument5 SeitenThis Study Resource Was: Logo HereMarcus MonocayNoch keine Bewertungen

- FAR - RQ - Investment in AssociatesDokument2 SeitenFAR - RQ - Investment in AssociatesKriane Kei50% (2)

- Identify The Choice That Best Completes The Statement or Answers The QuestionDokument8 SeitenIdentify The Choice That Best Completes The Statement or Answers The QuestionGabrielle100% (1)

- Pas 16. G4 1Dokument29 SeitenPas 16. G4 1Arvin Garbo50% (2)

- Investments in Debt and Equity SecuritiesDokument41 SeitenInvestments in Debt and Equity SecuritiesMonica Monica0% (1)

- 74827448-Ch17 Investment TestbankDokument44 Seiten74827448-Ch17 Investment TestbankkonyatanNoch keine Bewertungen

- Instructions: Choose The Letter That Corresponds To Your Answer and Write Them On A Crosswise YellowDokument8 SeitenInstructions: Choose The Letter That Corresponds To Your Answer and Write Them On A Crosswise YellowRoseNoch keine Bewertungen

- 9.2 Investment in AssociateDokument6 Seiten9.2 Investment in AssociateJorufel PapasinNoch keine Bewertungen

- FAR - Biological Assets and Agricultural ProduceDokument2 SeitenFAR - Biological Assets and Agricultural ProduceMariella Catacutan67% (3)

- Polytechnic University of The Philippines College of Accountancy Junior Philippine Institute of AccountantsDokument15 SeitenPolytechnic University of The Philippines College of Accountancy Junior Philippine Institute of AccountantsYassi CurtisNoch keine Bewertungen

- Financial Accounting and ReportingDokument3 SeitenFinancial Accounting and ReportingJAPNoch keine Bewertungen

- Pas 16 PpeDokument2 SeitenPas 16 PpeRitchel Casile100% (1)

- CH 08Dokument52 SeitenCH 08Cyrus Zack100% (5)

- IA1 Financial Assets at Fair ValueDokument11 SeitenIA1 Financial Assets at Fair ValueSteffanie OlivarNoch keine Bewertungen

- Investment in Equity Securities 1Dokument11 SeitenInvestment in Equity Securities 1dfsdfdsfNoch keine Bewertungen

- PA1 M 1404 InventoriesDokument30 SeitenPA1 M 1404 InventoriesShaina Santiago Alejo100% (1)

- Cag QuestionsDokument24 SeitenCag QuestionsJason Dave VidadNoch keine Bewertungen

- Drill - ReceivablesDokument7 SeitenDrill - ReceivablesMark Domingo MendozaNoch keine Bewertungen

- Lecture Notes On Receivable FinancingDokument5 SeitenLecture Notes On Receivable Financingjudel ArielNoch keine Bewertungen

- FAR First Pre BoardDokument18 SeitenFAR First Pre BoardKIM RAGANoch keine Bewertungen

- Accounting - Answer Key Quiz - Receivable FinancingDokument2 SeitenAccounting - Answer Key Quiz - Receivable FinancingNavsNoch keine Bewertungen

- 5.0 Receivable FInancing AccountingDokument51 Seiten5.0 Receivable FInancing Accountingeloudum100% (2)

- Chapter 14Dokument8 SeitenChapter 14einnajeniale75% (4)

- Camilon Francisco PPEDokument21 SeitenCamilon Francisco PPEGrace GamillaNoch keine Bewertungen

- P1.110 Investment Property.Dokument1 SeiteP1.110 Investment Property.aleish0301100% (1)

- K12 Philippines Whereabouts PDFDokument37 SeitenK12 Philippines Whereabouts PDFsichhahaNoch keine Bewertungen

- Ppe 2Dokument7 SeitenPpe 2Lara Lewis Achilles50% (2)

- This Study Resource Was: Invesment in Equity Securities UploadedDokument4 SeitenThis Study Resource Was: Invesment in Equity Securities UploadedmerryNoch keine Bewertungen

- Investment in Equity SecuritiesDokument11 SeitenInvestment in Equity SecuritiesnikNoch keine Bewertungen

- Intacc PpeDokument32 SeitenIntacc PpeIris MnemosyneNoch keine Bewertungen

- Accounting For Investments - Test BankDokument21 SeitenAccounting For Investments - Test BankIsh Selin100% (1)

- Handouts For Inventories: A. This Fact Must Be DisclosedDokument7 SeitenHandouts For Inventories: A. This Fact Must Be DisclosedDenver Legarda100% (1)

- 100% Key Answers For The 2 First Quizzes - ACT1104Dokument34 Seiten100% Key Answers For The 2 First Quizzes - ACT1104moncarla lagonNoch keine Bewertungen

- Conceptual Framework and Accounting Standards: Janesene N. Sol MWF 1:00-2:00 PMDokument4 SeitenConceptual Framework and Accounting Standards: Janesene N. Sol MWF 1:00-2:00 PMJanesene SolNoch keine Bewertungen

- IA 2 Quiz#2 - Reclassification of FA - Investment Property - Answer KeyDokument7 SeitenIA 2 Quiz#2 - Reclassification of FA - Investment Property - Answer KeychingchongNoch keine Bewertungen

- InventoriesDokument64 SeitenInventoriesJoey WassigNoch keine Bewertungen

- Finals Answer KeyDokument11 SeitenFinals Answer Keymarx marolinaNoch keine Bewertungen

- This Study Resource Was: Problem 1Dokument2 SeitenThis Study Resource Was: Problem 1Michelle J UrbodaNoch keine Bewertungen

- CH 17 JWBDokument38 SeitenCH 17 JWBFarisa MachmudNoch keine Bewertungen

- Allapacan Company Bought 20Dokument18 SeitenAllapacan Company Bought 20Carl Yry BitzNoch keine Bewertungen

- CH 09Dokument52 SeitenCH 09Cyrus Zack100% (6)

- #18 Reclassification of Financial AssetsDokument3 Seiten#18 Reclassification of Financial AssetsZaaavnn VannnnnNoch keine Bewertungen

- InventoriesDokument9 SeitenInventoriesDon John David100% (2)

- Which One of The Following Should Be Excluded Form InventoriesDokument1 SeiteWhich One of The Following Should Be Excluded Form InventoriesJAHNHANNALEI MARTICIONoch keine Bewertungen

- 50cb2fca 1597910723873pdf PDF FreeDokument10 Seiten50cb2fca 1597910723873pdf PDF FreefarandiNoch keine Bewertungen

- Examination About Investment 2Dokument2 SeitenExamination About Investment 2BLACKPINKLisaRoseJisooJennieNoch keine Bewertungen

- P1 CompreDokument3 SeitenP1 CompreCris Tarrazona CasipleNoch keine Bewertungen

- MidtermS2 InventoriesDokument11 SeitenMidtermS2 InventoriesQueenie Dayagro0% (2)

- Investments: IFRS Questions Are Available at The End of This ChapterDokument44 SeitenInvestments: IFRS Questions Are Available at The End of This Chapteralexstets4553Noch keine Bewertungen

- Chapter 21 - Reclassification of Financial Asset PDFDokument9 SeitenChapter 21 - Reclassification of Financial Asset PDFTurksNoch keine Bewertungen

- Compre ReviewerDokument33 SeitenCompre Reviewermarinel pioquidNoch keine Bewertungen

- Quiz in Fin Man AssetsDokument7 SeitenQuiz in Fin Man AssetsCherseaLizetteRoyPicaNoch keine Bewertungen

- Cpa Review School of The Philippines ManilaDokument6 SeitenCpa Review School of The Philippines ManilaAljur SalamedaNoch keine Bewertungen

- 1st Midterm Quiz QuestionnaireDokument11 Seiten1st Midterm Quiz QuestionnaireAthena Fatmah AmpuanNoch keine Bewertungen

- AK Mock BA 118.1 2nd LEDokument6 SeitenAK Mock BA 118.1 2nd LEBromanineNoch keine Bewertungen

- AK Mock BA 141 1st LEDokument2 SeitenAK Mock BA 141 1st LEBromanineNoch keine Bewertungen

- AK Mock BA 99.2 1st LEDokument4 SeitenAK Mock BA 99.2 1st LEBromanineNoch keine Bewertungen

- Mock Board Answer KeyDokument2 SeitenMock Board Answer KeyBromanineNoch keine Bewertungen

- Partners (Because TAC TCC PAC (New)Dokument5 SeitenPartners (Because TAC TCC PAC (New)BromanineNoch keine Bewertungen

- University of The Philippines VisayasDokument2 SeitenUniversity of The Philippines VisayasBromanineNoch keine Bewertungen

- 5ea7fb0c57f53 SEC Form 17A Dec2019Dokument222 Seiten5ea7fb0c57f53 SEC Form 17A Dec2019BromanineNoch keine Bewertungen

- Agamata Answer KeyDokument5 SeitenAgamata Answer KeyBromanineNoch keine Bewertungen

- (Pfrs/Ifrs 16) LeasesDokument11 Seiten(Pfrs/Ifrs 16) LeasesBromanineNoch keine Bewertungen

- Revised CPALE Syllabus - EditableDokument19 SeitenRevised CPALE Syllabus - EditableBromanineNoch keine Bewertungen

- Abatement: "A Reduction in The Assessment of Tax, Penalty or Interest When It Is Determined The Assessment Is Incorrect"Dokument1 SeiteAbatement: "A Reduction in The Assessment of Tax, Penalty or Interest When It Is Determined The Assessment Is Incorrect"BromanineNoch keine Bewertungen

- Technical AnalysisDokument34 SeitenTechnical AnalysisBromanine100% (1)

- Opening BalancesDokument37 SeitenOpening BalancesBromanineNoch keine Bewertungen

- Single Entry and Error CorrectionDokument2 SeitenSingle Entry and Error CorrectionBromanine0% (1)

- 6th Practice Qs 99.2Dokument3 Seiten6th Practice Qs 99.2BromanineNoch keine Bewertungen

- Audit of CashDokument4 SeitenAudit of CashBromanineNoch keine Bewertungen

- PRTC Oct2019 1st PB Answer Key PDFDokument2 SeitenPRTC Oct2019 1st PB Answer Key PDFBromanineNoch keine Bewertungen

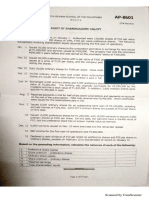

- AP 8603 - Audit of Property, Plant and EquipmentDokument6 SeitenAP 8603 - Audit of Property, Plant and EquipmentBromanineNoch keine Bewertungen

- Hyperinflation and Current CostDokument3 SeitenHyperinflation and Current CostBromanineNoch keine Bewertungen

- AP 8601 - Audit of Shareholders' EquityDokument8 SeitenAP 8601 - Audit of Shareholders' EquityBromanineNoch keine Bewertungen

- Sec Reportorial RequirementsDokument2 SeitenSec Reportorial RequirementsBromanineNoch keine Bewertungen

- Maths-Term End Examination-2020-2021 (2020-2021, MATHS)Dokument6 SeitenMaths-Term End Examination-2020-2021 (2020-2021, MATHS)Venkat Balaji0% (1)

- Abdukes App PaoerDokument49 SeitenAbdukes App PaoerAbdulkerim ReferaNoch keine Bewertungen

- Fish Immune System and Vaccines-Springer (2022) - 1Dokument293 SeitenFish Immune System and Vaccines-Springer (2022) - 1Rodolfo Velazco100% (1)

- Enter Pre NaurDokument82 SeitenEnter Pre NaurNeha singhalNoch keine Bewertungen

- Machine Tools Design: InstructorsDokument31 SeitenMachine Tools Design: InstructorsAladdin AdelNoch keine Bewertungen

- Project Documentation - Sensorflex 30G Data SheetDokument15 SeitenProject Documentation - Sensorflex 30G Data SheetOmar HectorNoch keine Bewertungen

- Factor Affecting Child Dental Behaviour PedoDokument19 SeitenFactor Affecting Child Dental Behaviour PedoFourthMolar.comNoch keine Bewertungen

- Youth Policy Manual: How To Develop A National Youth StrategyDokument94 SeitenYouth Policy Manual: How To Develop A National Youth StrategyCristinaDumitriuAxyNoch keine Bewertungen

- Sumit YadavDokument85 SeitenSumit Yadavanuj3026Noch keine Bewertungen

- Automatic Water Level Indicator and Controller by Using ARDUINODokument10 SeitenAutomatic Water Level Indicator and Controller by Using ARDUINOSounds of PeaceNoch keine Bewertungen

- Lingua Franca Core: The Outcome of The Current Times: Yue ShuDokument4 SeitenLingua Franca Core: The Outcome of The Current Times: Yue ShuThaiNoch keine Bewertungen

- Theories of EmotionDokument11 SeitenTheories of EmotionNoman ANoch keine Bewertungen

- Natureview Case StudyDokument3 SeitenNatureview Case StudySheetal RaniNoch keine Bewertungen

- Fontenot Opinion and OrderDokument190 SeitenFontenot Opinion and OrderInjustice WatchNoch keine Bewertungen

- The Convergent Parallel DesignDokument8 SeitenThe Convergent Parallel Designghina88% (8)

- Panama Canal - FinalDokument25 SeitenPanama Canal - FinalTeeksh Nagwanshi50% (2)

- Online Book Store System: Bachelor of Computer EngineeringDokument31 SeitenOnline Book Store System: Bachelor of Computer Engineeringkalpesh mayekarNoch keine Bewertungen

- IEEE 802.1adDokument7 SeitenIEEE 802.1adLe Viet HaNoch keine Bewertungen

- Analyzing Text - Yuli RizkiantiDokument12 SeitenAnalyzing Text - Yuli RizkiantiErikaa RahmaNoch keine Bewertungen

- Education Under The Philippine RepublicDokument25 SeitenEducation Under The Philippine RepublicShanice Del RosarioNoch keine Bewertungen

- Cropanzano, Mitchell - Social Exchange Theory PDFDokument28 SeitenCropanzano, Mitchell - Social Exchange Theory PDFNikolina B.Noch keine Bewertungen

- Derivative Pakistan PerspectiveDokument99 SeitenDerivative Pakistan PerspectiveUrooj KhanNoch keine Bewertungen

- CrossFit Wod Tracking JournalDokument142 SeitenCrossFit Wod Tracking JournalJavier Estelles Muñoz0% (1)

- SOAL ASSEMEN PAKET A BAHASA INGGRIS NewDokument3 SeitenSOAL ASSEMEN PAKET A BAHASA INGGRIS Newmtsn4 clpNoch keine Bewertungen

- Sample Information For Attempted MurderDokument3 SeitenSample Information For Attempted MurderIrin200Noch keine Bewertungen

- Baccolini, Raffaela - CH 8 Finding Utopia in Dystopia Feminism, Memory, Nostalgia and HopeDokument16 SeitenBaccolini, Raffaela - CH 8 Finding Utopia in Dystopia Feminism, Memory, Nostalgia and HopeMelissa de SáNoch keine Bewertungen

- Andrea Falcon - Aristotle On How Animals MoveDokument333 SeitenAndrea Falcon - Aristotle On How Animals MoveLigia G. DinizNoch keine Bewertungen

- FICCI-BCG Report On Railway Station RedevelopmentDokument47 SeitenFICCI-BCG Report On Railway Station RedevelopmentRahul MehrotraNoch keine Bewertungen

- Lecture 1. Introducing Second Language AcquisitionDokument18 SeitenLecture 1. Introducing Second Language AcquisitionДиляра КаримоваNoch keine Bewertungen

- Effects of Monetory PolicyDokument5 SeitenEffects of Monetory PolicyMoniya SinghNoch keine Bewertungen

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNVon Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNBewertung: 4.5 von 5 Sternen4.5/5 (3)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisVon EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisBewertung: 5 von 5 Sternen5/5 (6)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaVon EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaBewertung: 3.5 von 5 Sternen3.5/5 (8)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaVon EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaBewertung: 4.5 von 5 Sternen4.5/5 (14)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successVon EverandReady, Set, Growth hack:: A beginners guide to growth hacking successBewertung: 4.5 von 5 Sternen4.5/5 (93)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyVon EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyBewertung: 3 von 5 Sternen3/5 (1)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamVon EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNoch keine Bewertungen

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthVon EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthBewertung: 4 von 5 Sternen4/5 (20)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialVon EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNoch keine Bewertungen

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingVon EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingBewertung: 4.5 von 5 Sternen4.5/5 (17)

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursVon EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursBewertung: 5 von 5 Sternen5/5 (13)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialVon EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialBewertung: 4.5 von 5 Sternen4.5/5 (32)

- Creating Shareholder Value: A Guide For Managers And InvestorsVon EverandCreating Shareholder Value: A Guide For Managers And InvestorsBewertung: 4.5 von 5 Sternen4.5/5 (8)

- The Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsVon EverandThe Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsNoch keine Bewertungen

- Product-Led Growth: How to Build a Product That Sells ItselfVon EverandProduct-Led Growth: How to Build a Product That Sells ItselfBewertung: 5 von 5 Sternen5/5 (1)

- Mastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsVon EverandMastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsBewertung: 4.5 von 5 Sternen4.5/5 (21)

- Value: The Four Cornerstones of Corporate FinanceVon EverandValue: The Four Cornerstones of Corporate FinanceBewertung: 4.5 von 5 Sternen4.5/5 (18)

- Valley Girls: Lessons From Female Founders in the Silicon Valley and BeyondVon EverandValley Girls: Lessons From Female Founders in the Silicon Valley and BeyondNoch keine Bewertungen

- Mind over Money: The Psychology of Money and How to Use It BetterVon EverandMind over Money: The Psychology of Money and How to Use It BetterBewertung: 4 von 5 Sternen4/5 (24)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursVon EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursBewertung: 4.5 von 5 Sternen4.5/5 (8)

- Finance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Von EverandFinance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Bewertung: 4 von 5 Sternen4/5 (5)

- Buffett's 2-Step Stock Market Strategy: Know When To Buy A Stock, Become A Millionaire, Get The Highest ReturnsVon EverandBuffett's 2-Step Stock Market Strategy: Know When To Buy A Stock, Become A Millionaire, Get The Highest ReturnsBewertung: 5 von 5 Sternen5/5 (1)

- The Value of a Whale: On the Illusions of Green CapitalismVon EverandThe Value of a Whale: On the Illusions of Green CapitalismBewertung: 5 von 5 Sternen5/5 (2)