Das könnte Ihnen auch gefallen

- Black Book Investment BankingDokument23 SeitenBlack Book Investment Bankingsohail shaikh75% (4)

- Investment Banking & Private EquityDokument73 SeitenInvestment Banking & Private Equitymakarandr_1100% (1)

- If You Can't Trust Your Lawyer, 138 Univ. of Pennsylvania Law Rev. 785Dokument10 SeitenIf You Can't Trust Your Lawyer, 138 Univ. of Pennsylvania Law Rev. 785richdebtNoch keine Bewertungen

- Value-Oriented Equity Investment Ideas For Sophisticated InvestorsDokument117 SeitenValue-Oriented Equity Investment Ideas For Sophisticated InvestorsValueWalkNoch keine Bewertungen

- Aluminum Household Utensil Making PlantDokument26 SeitenAluminum Household Utensil Making PlantYohannes Woldekidan100% (1)

- Office of Career Development CAREER PATH: Investment Banking / Private WealthDokument31 SeitenOffice of Career Development CAREER PATH: Investment Banking / Private WealthanupdodiaNoch keine Bewertungen

- Project On Investment BankingDokument66 SeitenProject On Investment BankingRaveena Rane0% (1)

- Investment Banking ProjectDokument65 SeitenInvestment Banking ProjectShubhangi Virkar100% (3)

- (BNP Paribas) Quantitative Option StrategyDokument5 Seiten(BNP Paribas) Quantitative Option StrategygneymanNoch keine Bewertungen

- FINANCIAL INTELLIGENCE: FUNDAMENTALS OF PRIVATE PLACEMENT PROGRAMS (PPP)Von EverandFINANCIAL INTELLIGENCE: FUNDAMENTALS OF PRIVATE PLACEMENT PROGRAMS (PPP)Bewertung: 5 von 5 Sternen5/5 (1)

- Financial Services Project 1oomksDokument53 SeitenFinancial Services Project 1oomksNakul Mehta100% (2)

- Financial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingVon EverandFinancial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingNoch keine Bewertungen

- Mutual Funds in IndiaDokument83 SeitenMutual Funds in Indiaswangi100% (2)

- Role of NBFC in Indian Financial MarketDokument40 SeitenRole of NBFC in Indian Financial MarketPranav Vira100% (1)

- Introduction of Investment BankingDokument18 SeitenIntroduction of Investment Bankingshubham100% (2)

- Private Equity: History, Governance, and OperationsVon EverandPrivate Equity: History, Governance, and OperationsNoch keine Bewertungen

- Project Report ON: "A Study of Comparative Analyis of Kotak Mahindra Bank With Its Competitor'S"Dokument63 SeitenProject Report ON: "A Study of Comparative Analyis of Kotak Mahindra Bank With Its Competitor'S"Nitesh AgrawalNoch keine Bewertungen

- Investment Banking Explained: An Insider's Guide to the Industry: An Insider's Guide to the IndustryVon EverandInvestment Banking Explained: An Insider's Guide to the Industry: An Insider's Guide to the IndustryNoch keine Bewertungen

- Asian Range Manipulation by @GFR - AnalysisDokument6 SeitenAsian Range Manipulation by @GFR - Analysisforina harissonNoch keine Bewertungen

- Internship ReportDokument40 SeitenInternship ReportRahul SoroutNoch keine Bewertungen

- Euro FreightDokument68 SeitenEuro FreightIlya KabanovNoch keine Bewertungen

- Final Project ReportDokument57 SeitenFinal Project Reportpranshu thakur100% (2)

- Sbi Mutual FundsDokument48 SeitenSbi Mutual FundsJai Bindal 1 8 3 6 4Noch keine Bewertungen

- Law of IbDokument12 SeitenLaw of Ibmanish mishraNoch keine Bewertungen

- Pranit Final Project-Investment BankingDokument54 SeitenPranit Final Project-Investment BankingPriyankaR69Noch keine Bewertungen

- University of Mumbai Investment Banking: Project Report by Tejas.S.Kamble ROLLNO:18 T.Y.Bcom - Banking & InsuranceDokument54 SeitenUniversity of Mumbai Investment Banking: Project Report by Tejas.S.Kamble ROLLNO:18 T.Y.Bcom - Banking & Insurancetejaskamble45Noch keine Bewertungen

- Project Report Keshav YadavDokument46 SeitenProject Report Keshav Yadavkeshav yadavNoch keine Bewertungen

- Submitted in The Partial Fulfillment For The Requirement of The Award of Degree ofDokument66 SeitenSubmitted in The Partial Fulfillment For The Requirement of The Award of Degree ofJyoti YadavNoch keine Bewertungen

- Investment Banking ProjectDokument28 SeitenInvestment Banking ProjectDilip Ahir0% (1)

- Investment BankDokument8 SeitenInvestment BankArun KumarNoch keine Bewertungen

- Anubhavkumar DeskDokument33 SeitenAnubhavkumar DeskAnubhav RanjanNoch keine Bewertungen

- Marketing Financial ServicesDokument5 SeitenMarketing Financial ServicesshijinallepillyNoch keine Bewertungen

- Manish KumarDokument121 SeitenManish KumarHirdesh JainNoch keine Bewertungen

- Il&Fs Project ReportDokument61 SeitenIl&Fs Project Reportmahantesh123100% (32)

- University of Mumbai Project On: Comparison of Two Mutual Fund CompaniesDokument6 SeitenUniversity of Mumbai Project On: Comparison of Two Mutual Fund CompaniesTusharJoshiNoch keine Bewertungen

- The Banking OmbudsmanDokument104 SeitenThe Banking OmbudsmanTejashree WazeNoch keine Bewertungen

- IVFA True NorthDokument8 SeitenIVFA True NorthALLtyNoch keine Bewertungen

- Work of Investment Banking (Repaired)Dokument12 SeitenWork of Investment Banking (Repaired)Shivani Singh ChandelNoch keine Bewertungen

- Project Report On Investment Banking and Financial Markets in Kotak Mahindra BankDokument10 SeitenProject Report On Investment Banking and Financial Markets in Kotak Mahindra BankBala SudhakarNoch keine Bewertungen

- In Partial Fulfillment For The Award of The Degree Of: Bachelor in Commerce (Honours)Dokument25 SeitenIn Partial Fulfillment For The Award of The Degree Of: Bachelor in Commerce (Honours)Rahul SarawgiNoch keine Bewertungen

- Yashwant Project Black BookDokument79 SeitenYashwant Project Black BookYash SutarNoch keine Bewertungen

- 1.2.3 Financial IntermediariesDokument10 Seiten1.2.3 Financial IntermediariesthelavanderprincessNoch keine Bewertungen

- C1 - Tong Quan NHDT - EnglishDokument45 SeitenC1 - Tong Quan NHDT - Englishngannguyen.31221024512Noch keine Bewertungen

- Research Paper by Naresh Kachori, Roll No.22Dokument15 SeitenResearch Paper by Naresh Kachori, Roll No.2222Naresh KachoriNoch keine Bewertungen

- Ankita Akeni Tybaf - Blackbook - Demonetization - ProjectDokument48 SeitenAnkita Akeni Tybaf - Blackbook - Demonetization - ProjectSaikumar PillamariNoch keine Bewertungen

- Banking StylesDokument14 SeitenBanking StylesRen Algarate0% (1)

- Raja ProjectDokument108 SeitenRaja ProjectDeepak AkojuNoch keine Bewertungen

- Investment Banking Research PapersDokument7 SeitenInvestment Banking Research Paperstxdpmcbkf100% (1)

- Pizzaa SwiggyDokument65 SeitenPizzaa SwiggySaurabh BhardwajNoch keine Bewertungen

- Firoz ProjectDokument104 SeitenFiroz ProjectRishi GoyalNoch keine Bewertungen

- Final Project Report On Investment BankingDokument26 SeitenFinal Project Report On Investment BankingSophia Ali78% (9)

- Akshat Mahendra: Roll No. - 32Dokument68 SeitenAkshat Mahendra: Roll No. - 32krushna vaidyaNoch keine Bewertungen

- CRM Strategies of Public & Private Life Insurance Companies in IndiaDokument9 SeitenCRM Strategies of Public & Private Life Insurance Companies in IndiaOmkar NemlekarNoch keine Bewertungen

- Nakil Investment Banking FinalDokument52 SeitenNakil Investment Banking Finalnakil_parkar7880100% (1)

- Investment Banking - Priyank SandhellDokument66 SeitenInvestment Banking - Priyank SandhellPriyank Sandhel0% (1)

- PHD Thesis On Investment BankingDokument4 SeitenPHD Thesis On Investment BankingSara Alvarez100% (2)

- Innovations in Banking and InsuranceDokument60 SeitenInnovations in Banking and InsuranceSuraj ErandeNoch keine Bewertungen

- Fund Performance: A Comparative Analysis Between Birla Sun Life and Kotak FundsDokument34 SeitenFund Performance: A Comparative Analysis Between Birla Sun Life and Kotak FundsNavin KumarNoch keine Bewertungen

- Wa0006 PDFDokument65 SeitenWa0006 PDFPooja SahaniNoch keine Bewertungen

- Study On Awarenss of Investment Risks Amongst Investors in Mumbai RegioDokument95 SeitenStudy On Awarenss of Investment Risks Amongst Investors in Mumbai Regiovickylaljain2Noch keine Bewertungen

- Sohail Copied Black Book ProjectDokument64 SeitenSohail Copied Black Book ProjectArafat NakhudaNoch keine Bewertungen

- Pratik SIP ProposalDokument4 SeitenPratik SIP ProposalSai KiranNoch keine Bewertungen

- B.K. School of Business Management Gujarat UniversityDokument77 SeitenB.K. School of Business Management Gujarat UniversityMAHESHNoch keine Bewertungen

- A Detailed Analysis of The Mutual Fund Industry & A Customer Perception StudyDokument93 SeitenA Detailed Analysis of The Mutual Fund Industry & A Customer Perception StudyNishant GuptaNoch keine Bewertungen

- Unlocking Capital: The Power of Bonds in Project FinanceVon EverandUnlocking Capital: The Power of Bonds in Project FinanceNoch keine Bewertungen

- Print Server Compatibility List 160804 PDFDokument11 SeitenPrint Server Compatibility List 160804 PDFPranav ViraNoch keine Bewertungen

- Alm Guidelines by RBIDokument10 SeitenAlm Guidelines by RBIPranav ViraNoch keine Bewertungen

- C03164Dokument1 SeiteC03164Pranav ViraNoch keine Bewertungen

- The International Capital Markets Review: Law Business ResearchDokument30 SeitenThe International Capital Markets Review: Law Business ResearchPranav ViraNoch keine Bewertungen

- C03154Dokument1 SeiteC03154Pranav ViraNoch keine Bewertungen

- Conversion-Circular 2017 PDFDokument1 SeiteConversion-Circular 2017 PDFPranav ViraNoch keine Bewertungen

- Conversion CircularDokument3 SeitenConversion CircularPranav ViraNoch keine Bewertungen

- C01466Dokument2 SeitenC01466Pranav ViraNoch keine Bewertungen

- January March 08 Co 5Dokument4 SeitenJanuary March 08 Co 5Pranav ViraNoch keine Bewertungen

- PAGESDokument7 SeitenPAGESPranav ViraNoch keine Bewertungen

- New Microsoft Word DocumentDokument19 SeitenNew Microsoft Word DocumentPranav ViraNoch keine Bewertungen

- Guidelines 256Dokument5 SeitenGuidelines 256Pranav ViraNoch keine Bewertungen

- University of Mumbai Project On Credit Appraisal With Reference To Term Loan in Bank Bachelor of CommerceDokument56 SeitenUniversity of Mumbai Project On Credit Appraisal With Reference To Term Loan in Bank Bachelor of CommercePranav ViraNoch keine Bewertungen

- Exam Coe 357Dokument2 SeitenExam Coe 357Pranav ViraNoch keine Bewertungen

- TYBBI ProjectDokument57 SeitenTYBBI ProjectPranav ViraNoch keine Bewertungen

- Investing Secrets of Warren BuffettDokument31 SeitenInvesting Secrets of Warren BuffettPranav ViraNoch keine Bewertungen

- E-Suvidha Account ActivationDokument8 SeitenE-Suvidha Account ActivationPranav ViraNoch keine Bewertungen

- Commercial Banks: Explained - HTMLDokument3 SeitenCommercial Banks: Explained - HTMLPranav ViraNoch keine Bewertungen

- Vishal Thakur FINAL PROJECTDokument36 SeitenVishal Thakur FINAL PROJECTPranav ViraNoch keine Bewertungen

- Exam Fees 152018Dokument3 SeitenExam Fees 152018Pranav ViraNoch keine Bewertungen

- Tybbi Comparative Study of Strategy Implemented in BankDokument37 SeitenTybbi Comparative Study of Strategy Implemented in BankPranav ViraNoch keine Bewertungen

- Globalization of Insurance Need For Globalization: C H A P T e R 6Dokument2 SeitenGlobalization of Insurance Need For Globalization: C H A P T e R 6Pranav ViraNoch keine Bewertungen

- Top 10 Indian Banking Companies of 2017Dokument11 SeitenTop 10 Indian Banking Companies of 2017Pranav ViraNoch keine Bewertungen

- C0113 T.Y.B.com IDOL Group Passing1Dokument3 SeitenC0113 T.Y.B.com IDOL Group Passing1Pranav ViraNoch keine Bewertungen

- 10.2.1.8 Packet Tracer - Web and Email InstructionsDokument3 Seiten10.2.1.8 Packet Tracer - Web and Email InstructionsnskpotulaNoch keine Bewertungen

- Arbitrage IndiaDokument21 SeitenArbitrage IndiaPranav ViraNoch keine Bewertungen

- Export Import Bank of India PDFDokument83 SeitenExport Import Bank of India PDFPranav ViraNoch keine Bewertungen

- Association of Mutual Funds in India: Released On 07.12.2017 NotesDokument3 SeitenAssociation of Mutual Funds in India: Released On 07.12.2017 NotesPranav ViraNoch keine Bewertungen

- Countries Capitals Currencies PDFDokument16 SeitenCountries Capitals Currencies PDFAnonymous rmvzT79AkNoch keine Bewertungen

- FINE 6200 F, Winter 2016, TuesdayDokument9 SeitenFINE 6200 F, Winter 2016, TuesdayAlex PoonNoch keine Bewertungen

- Quiz Lesson 5 Inflation ProtectionDokument5 SeitenQuiz Lesson 5 Inflation ProtectionAKNoch keine Bewertungen

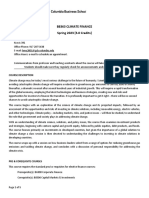

- Climate Finance Syllabus (Spring 2023)Dokument5 SeitenClimate Finance Syllabus (Spring 2023)Hamza HaiderNoch keine Bewertungen

- Strategic Management TB Chap009Dokument49 SeitenStrategic Management TB Chap009Hooi Fen OngNoch keine Bewertungen

- 08 Chapter 2Dokument34 Seiten08 Chapter 2Motiram paudelNoch keine Bewertungen

- Chapter 5 - Test BankDokument17 SeitenChapter 5 - Test Bankhipduggy100% (2)

- SBR INT MJ23 Examiner's ReportDokument15 SeitenSBR INT MJ23 Examiner's ReportBhavin PatelNoch keine Bewertungen

- New Century Loan Pools - List of Securities TrustsDokument11 SeitenNew Century Loan Pools - List of Securities Trusts83jjmack100% (1)

- Rosetta StoneDokument3 SeitenRosetta Stonedxc126700% (1)

- Replacement Theory: 20P204 - ASHWIN R 20P217 - Prithivirajan V 20P220 - Vijay Vignesh S 21P402 - Gurumoorthy DDokument20 SeitenReplacement Theory: 20P204 - ASHWIN R 20P217 - Prithivirajan V 20P220 - Vijay Vignesh S 21P402 - Gurumoorthy D21P410 - VARUN MNoch keine Bewertungen

- Studocudocument 2Dokument17 SeitenStudocudocument 2Kathleen J. GonzalesNoch keine Bewertungen

- Wikler Case Competition PowerpointDokument16 SeitenWikler Case Competition Powerpointbtlala0% (1)

- 121000008-890223086161x - Product Disclosure Sheet FinalDokument9 Seiten121000008-890223086161x - Product Disclosure Sheet FinalpubalanNoch keine Bewertungen

- Chapter 9 FINANCIAL MANAGEMENTDokument34 SeitenChapter 9 FINANCIAL MANAGEMENTLatha VarugheseNoch keine Bewertungen

- Future of Trading - RefinitivDokument8 SeitenFuture of Trading - Refinitivryan sharmaNoch keine Bewertungen

- Atlantic ComputerDokument39 SeitenAtlantic ComputerAbhijan Carter BiswasNoch keine Bewertungen

- Resume - Activity Looking Team Handling Profile in NBFC - 1Dokument3 SeitenResume - Activity Looking Team Handling Profile in NBFC - 1Sinkar ManojNoch keine Bewertungen

- Structure of The Balance Sheet and Statement of Cash Flows: Revsine/Collins/Johnson/Mittelstaedt/Soffer: Chapter 4Dokument39 SeitenStructure of The Balance Sheet and Statement of Cash Flows: Revsine/Collins/Johnson/Mittelstaedt/Soffer: Chapter 4amyNoch keine Bewertungen

- Quiz #1 PracticeDokument7 SeitenQuiz #1 PracticeSano ManjiroNoch keine Bewertungen

- Cash Flow Statement Important QuestionsDokument20 SeitenCash Flow Statement Important QuestionsSatinder SinghNoch keine Bewertungen

- Investment Analyst Cevian Capital 2017Dokument1 SeiteInvestment Analyst Cevian Capital 2017Miguel Couto RamosNoch keine Bewertungen

- ANZ Commodity Daily 841 120613Dokument5 SeitenANZ Commodity Daily 841 120613David SmithNoch keine Bewertungen

- Other Concepts and Valuation Techniques MA 05.24.23Dokument4 SeitenOther Concepts and Valuation Techniques MA 05.24.23Ivan Jay E. EsminoNoch keine Bewertungen

- 118 - Zain KhanDokument38 Seiten118 - Zain KhanDivyashree KarvirNoch keine Bewertungen