Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- 5-The Mathematics of Investment-1924-William L.hartDokument321 Seiten5-The Mathematics of Investment-1924-William L.hartmartin160464100% (6)

- Conceptions and Dimensions of DevelopmentDokument19 SeitenConceptions and Dimensions of DevelopmentGrace Talamera-Sandico100% (1)

- Assignment 1 A FaDokument3 SeitenAssignment 1 A Faeater PeopleNoch keine Bewertungen

- Entrepreneurship Development Project - CinemasDokument92 SeitenEntrepreneurship Development Project - CinemaspranjalNoch keine Bewertungen

- RTC Bukidnon Writ PossessionDokument6 SeitenRTC Bukidnon Writ PossessionAngelei Tecson Tigulo100% (1)

- Non Banking Financial Companies: by Sudev Jyothisi FN-92 Scms-CochinDokument32 SeitenNon Banking Financial Companies: by Sudev Jyothisi FN-92 Scms-CochinSUDEVJYOTHISINoch keine Bewertungen

- Leading Financial Services Firm Destimoney SecuritiesDokument3 SeitenLeading Financial Services Firm Destimoney SecuritiesSwapnil100% (1)

- EI Fund Transfer Intnl TT Form V3.0Dokument1 SeiteEI Fund Transfer Intnl TT Form V3.0Tosin SimeonNoch keine Bewertungen

- Icici Ipo1Dokument5 SeitenIcici Ipo1GreatAkxNoch keine Bewertungen

- Agi Claim Form 3117 - 221213 - 223631Dokument2 SeitenAgi Claim Form 3117 - 221213 - 223631Rohit Singh ChauhanNoch keine Bewertungen

- Notice: Ocean Transportation Intermediary Licenses: Impex Transport Inc.Dokument1 SeiteNotice: Ocean Transportation Intermediary Licenses: Impex Transport Inc.Justia.comNoch keine Bewertungen

- HR termination letterDokument1 SeiteHR termination letterAjeet ThakurNoch keine Bewertungen

- Cotización (VHT System. Model. VHC-100M 1set CIF)Dokument3 SeitenCotización (VHT System. Model. VHC-100M 1set CIF)andres gonzalezNoch keine Bewertungen

- Mortgage Deed SavarkundlaDokument8 SeitenMortgage Deed Savarkundladkumar471Noch keine Bewertungen

- Ibs Mib Al-Idrus 1 31/03/21Dokument7 SeitenIbs Mib Al-Idrus 1 31/03/21warfear88Noch keine Bewertungen

- Impact of New Financial Products On Financial PerfDokument9 SeitenImpact of New Financial Products On Financial PerfResearch SolutionsNoch keine Bewertungen

- PCI DSS NotificationDokument2 SeitenPCI DSS NotificationRajaNoch keine Bewertungen

- 2 Fin. Intermediaries & InnovationDokument29 Seiten2 Fin. Intermediaries & InnovationIbna Mursalin ShakilNoch keine Bewertungen

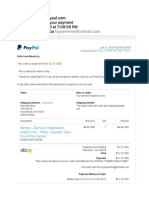

- Receipt For Your PaymentDokument2 SeitenReceipt For Your PaymentMime MendozaNoch keine Bewertungen

- Satyam Scam Who Is Responsible?Dokument3 SeitenSatyam Scam Who Is Responsible?ravish419Noch keine Bewertungen

- State Bank of India savings account statement for Mr. Rachaprolu AtchaiahDokument12 SeitenState Bank of India savings account statement for Mr. Rachaprolu AtchaiahRajesh pvkNoch keine Bewertungen

- Indonesian Energy and Basic Materials Company DataDokument36 SeitenIndonesian Energy and Basic Materials Company Datasas2000idNoch keine Bewertungen

- CIBIL Google Credit Distributed 2021Dokument60 SeitenCIBIL Google Credit Distributed 2021Abhishek MurarkaNoch keine Bewertungen

- BC NEIA Booklet English 01-08-2019Dokument14 SeitenBC NEIA Booklet English 01-08-2019abhiroopboseNoch keine Bewertungen

- Clarifying Debate on Bank Deposits, Loans and Fractional ReservesDokument19 SeitenClarifying Debate on Bank Deposits, Loans and Fractional ReservesAlex MingNoch keine Bewertungen

- Merchant BankingDokument19 SeitenMerchant BankingMiral PatelNoch keine Bewertungen

- Online Shopping CoimbatoreDokument4 SeitenOnline Shopping CoimbatoreKarthikeyan NNoch keine Bewertungen

- 3/25/2012 Prof. Nijumon K John, Christ University, BangaloreDokument13 Seiten3/25/2012 Prof. Nijumon K John, Christ University, BangaloreAshish JainNoch keine Bewertungen

- Voucher 2023 03 01Dokument1 SeiteVoucher 2023 03 01Mir Mazhar Ali MagsiNoch keine Bewertungen

- The "Debt-Trap" Narrative Around Chinese Loans Shows Africa's Weak Economic DiplomacyDokument6 SeitenThe "Debt-Trap" Narrative Around Chinese Loans Shows Africa's Weak Economic DiplomacyThavamNoch keine Bewertungen