Das könnte Ihnen auch gefallen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Competition Law Critical AnalysisDokument6 SeitenCompetition Law Critical AnalysisGeetika AnandNoch keine Bewertungen

- Invoice for Dell Monitor Shipped to ArgentinaDokument1 SeiteInvoice for Dell Monitor Shipped to ArgentinaBrian Michel RomanNoch keine Bewertungen

- Innovation, Intellectual Property, and Development: A Better Set of Approaches For The 21st CenturyDokument90 SeitenInnovation, Intellectual Property, and Development: A Better Set of Approaches For The 21st CenturyCenter for Economic and Policy ResearchNoch keine Bewertungen

- Distribution Competitiveness GuideDokument12 SeitenDistribution Competitiveness GuideEilyn PimientaNoch keine Bewertungen

- Co CreateDokument34 SeitenCo CreateAbhishek SinhaNoch keine Bewertungen

- 1Dokument7 Seiten1Abhishek SinhaNoch keine Bewertungen

- India's Economy Slows Despite Stimulus MeasuresDokument3 SeitenIndia's Economy Slows Despite Stimulus MeasuresAbhishek SinhaNoch keine Bewertungen

- How Google Works: A Guide to Google SearchDokument38 SeitenHow Google Works: A Guide to Google SearchAbhishek SinhaNoch keine Bewertungen

- Interview Dos: HandshakeDokument4 SeitenInterview Dos: HandshakeRahul Kumar SinghNoch keine Bewertungen

- Chapter 9 SolutionsDokument7 SeitenChapter 9 SolutionsRose McMahon50% (2)

- Microeconomics - Tutorial Practice Attempt 6Dokument2 SeitenMicroeconomics - Tutorial Practice Attempt 6Kelyn KokNoch keine Bewertungen

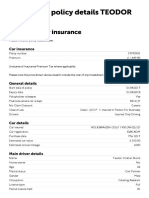

- Policy Details PageDokument2 SeitenPolicy Details PageLuci PoroNoch keine Bewertungen

- Investor Behaviour MatrixDokument23 SeitenInvestor Behaviour Matrixabhishek sharmaNoch keine Bewertungen

- Meralco - Customer Service GuideDokument22 SeitenMeralco - Customer Service Guidebaculao50% (2)

- Budget and B Udgetary C OntrolDokument6 SeitenBudget and B Udgetary C OntrolKanika DahiyaNoch keine Bewertungen

- Process CostingDokument76 SeitenProcess CostingAnonymous Lz2qH7Noch keine Bewertungen

- Markowitz Portfolio TheoryRDokument9 SeitenMarkowitz Portfolio TheoryRShafiq KhanNoch keine Bewertungen

- EOLA's Equity Distribution - v4Dokument18 SeitenEOLA's Equity Distribution - v4AR-Lion ResearchingNoch keine Bewertungen

- Biotech Sunglasses Break-Even AnalysisDokument8 SeitenBiotech Sunglasses Break-Even AnalysisKuralay TilegenNoch keine Bewertungen

- Midterm Examination in Public FinanceDokument2 SeitenMidterm Examination in Public FinanceNekki Joy LangcuyanNoch keine Bewertungen

- Chapter 34 - The Influence of Monetary and Fiscal Policy On Aggregate Demand (Compatibility Mode) PDFDokument19 SeitenChapter 34 - The Influence of Monetary and Fiscal Policy On Aggregate Demand (Compatibility Mode) PDFthanhvu78Noch keine Bewertungen

- Chapter 1: Financial Management and Financial ObjectivesDokument15 SeitenChapter 1: Financial Management and Financial ObjectivesAmir ArifNoch keine Bewertungen

- Quiz 3 SolutionsDokument6 SeitenQuiz 3 SolutionsNgsNoch keine Bewertungen

- Urban Transport in India PPP ArrangementDokument52 SeitenUrban Transport in India PPP ArrangementJailendra KashyapNoch keine Bewertungen

- What Is The Capital Asset Pricing Model?Dokument5 SeitenWhat Is The Capital Asset Pricing Model?Anne Kristine OniaNoch keine Bewertungen

- McDonald's PresentationDokument21 SeitenMcDonald's PresentationAli75% (4)

- Emory Endeavors in History Vol 3 2010Dokument125 SeitenEmory Endeavors in History Vol 3 2010Maggie PeltierNoch keine Bewertungen

- 01 Service Sheet 129Dokument4 Seiten01 Service Sheet 129bernzikNoch keine Bewertungen

- Chapter2 Exercise and TestDokument22 SeitenChapter2 Exercise and TestMichelle LamNoch keine Bewertungen

- CH 11 - CF Estimation Mini Case Sols Word 1514edDokument13 SeitenCH 11 - CF Estimation Mini Case Sols Word 1514edHari CahyoNoch keine Bewertungen

- Tugas Kelompok Manajemen KeuanganDokument9 SeitenTugas Kelompok Manajemen Keuangan2j9yp89bkgNoch keine Bewertungen

- Financial Reeporting: February 2022 EditionDokument169 SeitenFinancial Reeporting: February 2022 EditionAnu GraphicsNoch keine Bewertungen

- Understanding the Difference Between Positive and Normative EconomicsDokument21 SeitenUnderstanding the Difference Between Positive and Normative EconomicsKevin Fernandez MendioroNoch keine Bewertungen

- COL Retail Sample ExamDokument31 SeitenCOL Retail Sample ExamFernanda Raquel0% (1)

- Sale of City of Watertown Owned Properties March 2022Dokument2 SeitenSale of City of Watertown Owned Properties March 2022NewzjunkyNoch keine Bewertungen