Das könnte Ihnen auch gefallen

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsVon EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNoch keine Bewertungen

- BHEL - Rock Solid - RBS - Jan2011Dokument8 SeitenBHEL - Rock Solid - RBS - Jan2011Jitender KumarNoch keine Bewertungen

- Format: Format For Submission of Proposal For Administrative Approval (A/A) & Expenditure Sanction (E/S) During 2018-19Dokument10 SeitenFormat: Format For Submission of Proposal For Administrative Approval (A/A) & Expenditure Sanction (E/S) During 2018-19Runness RajkumarNoch keine Bewertungen

- Stock Decoder - Skipper Ltd-202402261647087215913Dokument1 SeiteStock Decoder - Skipper Ltd-202402261647087215913patelankurrhpmNoch keine Bewertungen

- Project 2Dokument2 SeitenProject 2Bảo Anh NguyễnNoch keine Bewertungen

- 3StatementModelTemplate Full Version1Dokument16 Seiten3StatementModelTemplate Full Version1Dawit TilahunNoch keine Bewertungen

- My KPI DashboardDokument16 SeitenMy KPI Dashboardjessy_pattyNoch keine Bewertungen

- 09 - KPI DashboardDokument18 Seiten09 - KPI DashboardCharlesNoch keine Bewertungen

- LBSL Weekly Stock Market Report 11 July 2019Dokument11 SeitenLBSL Weekly Stock Market Report 11 July 2019Mohammad YusufNoch keine Bewertungen

- Semiconductor Crisis An Opportunity For India - Defence News - The Financial ExpressDokument11 SeitenSemiconductor Crisis An Opportunity For India - Defence News - The Financial ExpressruchijainswmNoch keine Bewertungen

- EMI Calculator - Prepayment OptionDokument15 SeitenEMI Calculator - Prepayment OptionPrateekSorteNoch keine Bewertungen

- Cost-Volume-Profit Relationships: Mcgraw-Hill /irwinDokument82 SeitenCost-Volume-Profit Relationships: Mcgraw-Hill /irwinXu FengNoch keine Bewertungen

- Report Analysis SIDBI - 2016-2018 - : Vivek V Indian Institute of Management, KashipurDokument12 SeitenReport Analysis SIDBI - 2016-2018 - : Vivek V Indian Institute of Management, KashipurVivek VvkNoch keine Bewertungen

- Nestle - FM - Sumit - 230704 - 192257Dokument11 SeitenNestle - FM - Sumit - 230704 - 192257Bilal SafatNoch keine Bewertungen

- Annual Computation of Taxable Salary FY 2021-22Dokument1 SeiteAnnual Computation of Taxable Salary FY 2021-22Irfan RazaNoch keine Bewertungen

- Feasibility Study AnalisticDokument4 SeitenFeasibility Study AnalisticAntopuntodewoNoch keine Bewertungen

- Axis Long Term Equity Fund Direct Plan Growth Option: y y y R y T y T y H R T y UDokument1 SeiteAxis Long Term Equity Fund Direct Plan Growth Option: y y y R y T y T y H R T y Ukishore13Noch keine Bewertungen

- EMI CalculatorDokument15 SeitenEMI Calculatorasifamin85Noch keine Bewertungen

- Adventure Cycles DashboardDokument2 SeitenAdventure Cycles DashboardUpadrasta HarishNoch keine Bewertungen

- Stockbit - Komunitas Saham IndonesiaDokument1 SeiteStockbit - Komunitas Saham IndonesiaDaveWaliNoch keine Bewertungen

- Aehr Test SystemsDokument1 SeiteAehr Test SystemsYS FongNoch keine Bewertungen

- Monthlycollegebudget-Rebecca ConnorDokument1 SeiteMonthlycollegebudget-Rebecca Connorapi-481104706Noch keine Bewertungen

- EMI Calculator - Prepayment OptionDokument16 SeitenEMI Calculator - Prepayment Optionyashwanthakur96Noch keine Bewertungen

- Investment Thesis by Prateek LalDokument2 SeitenInvestment Thesis by Prateek LalPrateek LalNoch keine Bewertungen

- Bai 2Dokument4 SeitenBai 2Lan HuỳnhNoch keine Bewertungen

- Nippon India Gold Savings Fund - Direct Plan - GrowthDokument1 SeiteNippon India Gold Savings Fund - Direct Plan - GrowthKeval ShahNoch keine Bewertungen

- DR Reddy LabsDokument6 SeitenDR Reddy LabsAdarsh ChavelNoch keine Bewertungen

- Productivity Apps: Year Month DivisionDokument18 SeitenProductivity Apps: Year Month DivisionAustin AndersonNoch keine Bewertungen

- Lafarge AR 2017Dokument173 SeitenLafarge AR 2017Junwen LeeNoch keine Bewertungen

- EMI Calculator - Prepayment OptionDokument18 SeitenEMI Calculator - Prepayment Optionpranil deshmukhNoch keine Bewertungen

- ITC LTD.: Presented ByDokument12 SeitenITC LTD.: Presented BypavanNoch keine Bewertungen

- Productivity Apps: Revenue CashDokument17 SeitenProductivity Apps: Revenue CashGuruchell ChellguruNoch keine Bewertungen

- Parag Parikh Long TermDokument1 SeiteParag Parikh Long TermYogi173Noch keine Bewertungen

- 0% Interest CalculationDokument2 Seiten0% Interest CalculationGet DigitalizeNoch keine Bewertungen

- EMI Calculator - Prepayment OptionDokument15 SeitenEMI Calculator - Prepayment OptionHilal bhatNoch keine Bewertungen

- Eva Tree ModelDokument11 SeitenEva Tree Modelwelcome2jungleNoch keine Bewertungen

- V-Mart Retail: Demand Pick-Up Likely From H2, BUYDokument3 SeitenV-Mart Retail: Demand Pick-Up Likely From H2, BUYshalabh_hscNoch keine Bewertungen

- Talwalkars Better Value Fitness Limited BSE 533200 FinancialsDokument36 SeitenTalwalkars Better Value Fitness Limited BSE 533200 FinancialsraushanatscribdNoch keine Bewertungen

- Monthly Report With Dummy DataDokument1 SeiteMonthly Report With Dummy Datasenthil velNoch keine Bewertungen

- Himanshu Parihar 211510023747 SocratesDokument7 SeitenHimanshu Parihar 211510023747 SocratesHimanshu PariharNoch keine Bewertungen

- Client: PT Jambi Prima Coal Closing Date: 31 Desember 2018Dokument7 SeitenClient: PT Jambi Prima Coal Closing Date: 31 Desember 2018Umar MukhtarNoch keine Bewertungen

- Business Strategy For The Petrochemicals & Plastics Sector: October 8, 2015Dokument36 SeitenBusiness Strategy For The Petrochemicals & Plastics Sector: October 8, 2015afs araeNoch keine Bewertungen

- Finace TestDokument6 SeitenFinace TestMichael AzerNoch keine Bewertungen

- Etf Wealth RCH 0416fDokument2 SeitenEtf Wealth RCH 0416fMatt EbrahimiNoch keine Bewertungen

- 79 - Forbes ReportDokument11 Seiten79 - Forbes ReportMarcelo BuchNoch keine Bewertungen

- Uraian Tahun 0 1 2 3 4 5 6 7 8 9 10 Benefit: Lampiran 1 Tabel Hasil Kuesioner Data Finansial Usahatani Kakao Di Desa KareDokument2 SeitenUraian Tahun 0 1 2 3 4 5 6 7 8 9 10 Benefit: Lampiran 1 Tabel Hasil Kuesioner Data Finansial Usahatani Kakao Di Desa KareAditya Hadi SNoch keine Bewertungen

- SecB Grp11 CFDokument9 SeitenSecB Grp11 CFswapnil anandNoch keine Bewertungen

- Sssar2010low 120222214841 Phpapp02 PDFDokument31 SeitenSssar2010low 120222214841 Phpapp02 PDFKhaela MercaderNoch keine Bewertungen

- Project Far Group C (g2)Dokument3 SeitenProject Far Group C (g2)jalilah jamaludinNoch keine Bewertungen

- Bal Krishna SoniDokument6 SeitenBal Krishna SoniPreetam JainNoch keine Bewertungen

- Sales Growth Rate: Richard L. Keyser Chairman and Chief Executive OfficerDokument57 SeitenSales Growth Rate: Richard L. Keyser Chairman and Chief Executive OfficerchabucaNoch keine Bewertungen

- Hariharan A - F21143 - HCL - Capital BudgetingDokument3 SeitenHariharan A - F21143 - HCL - Capital BudgetingJoseph JohnNoch keine Bewertungen

- Practice Case Study A (Template)Dokument16 SeitenPractice Case Study A (Template)Jomarie EmilianoNoch keine Bewertungen

- Feasibility Studies The M-One Resto & Coffee: Gross SalesDokument2 SeitenFeasibility Studies The M-One Resto & Coffee: Gross SalesAntopuntodewoNoch keine Bewertungen

- Project 2Dokument3 SeitenProject 2Mai HàNoch keine Bewertungen

- Goodwill Finance FM FinalDokument231 SeitenGoodwill Finance FM Finalmeenal_smNoch keine Bewertungen

- Investor Presentation - December 2021Dokument9 SeitenInvestor Presentation - December 2021Yasir Hafeez Tariq, M.Phil. Scholar, Institute of Management Studies, UoPNoch keine Bewertungen

- Emolument Comp Report - Investment Professional, Associate Director - VP - PrincipalDokument9 SeitenEmolument Comp Report - Investment Professional, Associate Director - VP - PrincipalMason DukeNoch keine Bewertungen

- Daily Revenue Report DT Business Bay: 02 March 2021Dokument1 SeiteDaily Revenue Report DT Business Bay: 02 March 2021Jeric VendiolaNoch keine Bewertungen

- Axis Focused 25 FundDokument1 SeiteAxis Focused 25 FundYogi173Noch keine Bewertungen

- Retainage Release Invoices in Oracle AP - ErpSchoolsDokument9 SeitenRetainage Release Invoices in Oracle AP - ErpSchoolsK.rajesh Kumar ReddyNoch keine Bewertungen

- Fundraising Blueprint Plan TemplateDokument3 SeitenFundraising Blueprint Plan Templateoxade21Noch keine Bewertungen

- FM 8th Edition Chapter 12 - Risk and ReturnDokument20 SeitenFM 8th Edition Chapter 12 - Risk and ReturnKa Io ChaoNoch keine Bewertungen

- EnglishtoMath##1Dokument8 SeitenEnglishtoMath##1zubairNoch keine Bewertungen

- Case Study-1 SHEENADokument2 SeitenCase Study-1 SHEENARushikesh Dandagwhal100% (1)

- Harish NatarajanDokument10 SeitenHarish NatarajanbananiacorpNoch keine Bewertungen

- StartUp India - Case AnalysisDokument3 SeitenStartUp India - Case AnalysisIrshad AzeezNoch keine Bewertungen

- Bradford Snell The Street Car ConspiracyDokument4 SeitenBradford Snell The Street Car ConspiracyDaniel DavarNoch keine Bewertungen

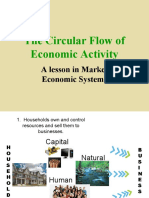

- Circular FlowDokument21 SeitenCircular FlowSheryl BorromeoNoch keine Bewertungen

- Putting English Unit14Dokument13 SeitenPutting English Unit14Dung LeNoch keine Bewertungen

- Introduction To Business - 5Dokument11 SeitenIntroduction To Business - 5Md. Rayhanul IslamNoch keine Bewertungen

- Gat PreparationDokument21 SeitenGat PreparationHAFIZ IMRAN AKHTERNoch keine Bewertungen

- Business Level StrategyDokument28 SeitenBusiness Level StrategyMohammad Raihanul HasanNoch keine Bewertungen

- RWJ 08Dokument38 SeitenRWJ 08Kunal PuriNoch keine Bewertungen

- 8508Dokument10 Seiten8508Danyal ChaudharyNoch keine Bewertungen

- Scarcity and ChoiceDokument4 SeitenScarcity and ChoicearuprofNoch keine Bewertungen

- IOW Casting Company NPV Excel SolutionDokument15 SeitenIOW Casting Company NPV Excel Solutionalka murarka100% (1)

- Closure in Valuation: Estimating Terminal Value: Problem 1Dokument3 SeitenClosure in Valuation: Estimating Terminal Value: Problem 1Silviu TrebuianNoch keine Bewertungen

- 5-Minute Chocolate Balls PDFDokument10 Seiten5-Minute Chocolate Balls PDFDiana ArunNoch keine Bewertungen

- Agriculture Subsidies and DevelopmentDokument2 SeitenAgriculture Subsidies and Developmentbluerockwalla100% (2)

- Direct Mail Success SecretsDokument0 SeitenDirect Mail Success SecretsunpinkpantherNoch keine Bewertungen

- Ch.10 - The Statement of Cash Flows - MHDokument59 SeitenCh.10 - The Statement of Cash Flows - MHSamZhao100% (1)

- Super Injunction BookDokument3 SeitenSuper Injunction BookReckless Kobold0% (1)

- Masan Group CorporationDokument31 SeitenMasan Group Corporationhồ nam longNoch keine Bewertungen

- Break Even Point ExplanationDokument2 SeitenBreak Even Point ExplanationEdgar IbarraNoch keine Bewertungen

- Ans Mini Case 2 - A171 - LecturerDokument14 SeitenAns Mini Case 2 - A171 - LecturerXue Yin Lew100% (1)

- Tennis Ball Activity - Diminishing Returns - Notes - 3Dokument1 SeiteTennis Ball Activity - Diminishing Returns - Notes - 3Raghvi AryaNoch keine Bewertungen

- Respond To Business OpportunitiesDokument21 SeitenRespond To Business OpportunitiesRissabelle CoscaNoch keine Bewertungen

- Supervisory Development Final ProjectDokument12 SeitenSupervisory Development Final ProjectCarolinaNoch keine Bewertungen

- The Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessVon EverandThe Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessBewertung: 5 von 5 Sternen5/5 (456)

- Summary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessVon EverandSummary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessNoch keine Bewertungen

- Summary of 12 Rules for Life: An Antidote to ChaosVon EverandSummary of 12 Rules for Life: An Antidote to ChaosBewertung: 4.5 von 5 Sternen4.5/5 (294)

- Summary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesVon EverandSummary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesBewertung: 5 von 5 Sternen5/5 (1636)

- Can't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsVon EverandCan't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsBewertung: 4.5 von 5 Sternen4.5/5 (386)

- Summary of The New Menopause by Mary Claire Haver MD: Navigating Your Path Through Hormonal Change with Purpose, Power, and FactsVon EverandSummary of The New Menopause by Mary Claire Haver MD: Navigating Your Path Through Hormonal Change with Purpose, Power, and FactsNoch keine Bewertungen

- Mindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessVon EverandMindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessBewertung: 4.5 von 5 Sternen4.5/5 (328)

- The Whole-Brain Child by Daniel J. Siegel, M.D., and Tina Payne Bryson, PhD. - Book Summary: 12 Revolutionary Strategies to Nurture Your Child’s Developing MindVon EverandThe Whole-Brain Child by Daniel J. Siegel, M.D., and Tina Payne Bryson, PhD. - Book Summary: 12 Revolutionary Strategies to Nurture Your Child’s Developing MindBewertung: 4.5 von 5 Sternen4.5/5 (57)

- Summary of The Algebra of Wealth by Scott Galloway: A Simple Formula for Financial SecurityVon EverandSummary of The Algebra of Wealth by Scott Galloway: A Simple Formula for Financial SecurityNoch keine Bewertungen

- Essentialism by Greg McKeown - Book Summary: The Disciplined Pursuit of LessVon EverandEssentialism by Greg McKeown - Book Summary: The Disciplined Pursuit of LessBewertung: 4.5 von 5 Sternen4.5/5 (188)

- The Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaVon EverandThe Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesVon EverandThe War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesBewertung: 4.5 von 5 Sternen4.5/5 (274)

- The One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsVon EverandThe One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsBewertung: 4.5 von 5 Sternen4.5/5 (709)

- Summary of The Galveston Diet by Mary Claire Haver MD: The Doctor-Developed, Patient-Proven Plan to Burn Fat and Tame Your Hormonal SymptomsVon EverandSummary of The Galveston Diet by Mary Claire Haver MD: The Doctor-Developed, Patient-Proven Plan to Burn Fat and Tame Your Hormonal SymptomsNoch keine Bewertungen

- Summary of Atomic Habits by James ClearVon EverandSummary of Atomic Habits by James ClearBewertung: 5 von 5 Sternen5/5 (170)

- How To Win Friends and Influence People by Dale Carnegie - Book SummaryVon EverandHow To Win Friends and Influence People by Dale Carnegie - Book SummaryBewertung: 5 von 5 Sternen5/5 (557)

- Steal Like an Artist by Austin Kleon - Book Summary: 10 Things Nobody Told You About Being CreativeVon EverandSteal Like an Artist by Austin Kleon - Book Summary: 10 Things Nobody Told You About Being CreativeBewertung: 4.5 von 5 Sternen4.5/5 (128)

- Summary of Miracle Morning Millionaires: What the Wealthy Do Before 8AM That Will Make You Rich by Hal Elrod and David OsbornVon EverandSummary of Miracle Morning Millionaires: What the Wealthy Do Before 8AM That Will Make You Rich by Hal Elrod and David OsbornBewertung: 5 von 5 Sternen5/5 (201)

- Summary of Eat to Beat Disease by Dr. William LiVon EverandSummary of Eat to Beat Disease by Dr. William LiBewertung: 5 von 5 Sternen5/5 (52)

- Summary of Million Dollar Weekend by Noah Kagan and Tahl Raz: The Surprisingly Simple Way to Launch a 7-Figure Business in 48 HoursVon EverandSummary of Million Dollar Weekend by Noah Kagan and Tahl Raz: The Surprisingly Simple Way to Launch a 7-Figure Business in 48 HoursNoch keine Bewertungen

- Good to Great by Jim Collins - Book Summary: Why Some Companies Make the Leap...And Others Don'tVon EverandGood to Great by Jim Collins - Book Summary: Why Some Companies Make the Leap...And Others Don'tBewertung: 4.5 von 5 Sternen4.5/5 (64)

- Blink by Malcolm Gladwell - Book Summary: The Power of Thinking Without ThinkingVon EverandBlink by Malcolm Gladwell - Book Summary: The Power of Thinking Without ThinkingBewertung: 4.5 von 5 Sternen4.5/5 (114)

- Make It Stick by Peter C. Brown, Henry L. Roediger III, Mark A. McDaniel - Book Summary: The Science of Successful LearningVon EverandMake It Stick by Peter C. Brown, Henry L. Roediger III, Mark A. McDaniel - Book Summary: The Science of Successful LearningBewertung: 4.5 von 5 Sternen4.5/5 (55)

- Extreme Ownership by Jocko Willink and Leif Babin - Book Summary: How U.S. Navy SEALS Lead And WinVon EverandExtreme Ownership by Jocko Willink and Leif Babin - Book Summary: How U.S. Navy SEALS Lead And WinBewertung: 4.5 von 5 Sternen4.5/5 (75)

- Summary of When Things Fall Apart: Heart Advice for Difficult Times by Pema ChödrönVon EverandSummary of When Things Fall Apart: Heart Advice for Difficult Times by Pema ChödrönBewertung: 4.5 von 5 Sternen4.5/5 (22)

- Summary of Supercommunicators by Charles Duhigg: How to Unlock the Secret Language of ConnectionVon EverandSummary of Supercommunicators by Charles Duhigg: How to Unlock the Secret Language of ConnectionNoch keine Bewertungen

- The 5 Second Rule by Mel Robbins - Book Summary: Transform Your Life, Work, and Confidence with Everyday CourageVon EverandThe 5 Second Rule by Mel Robbins - Book Summary: Transform Your Life, Work, and Confidence with Everyday CourageBewertung: 4.5 von 5 Sternen4.5/5 (329)

- Book Summary of The Code of The Extraordinary Mind by Vishen LakhianiVon EverandBook Summary of The Code of The Extraordinary Mind by Vishen LakhianiBewertung: 4.5 von 5 Sternen4.5/5 (124)