Das könnte Ihnen auch gefallen

- Gross To Net Salaries in EuropeDokument2 SeitenGross To Net Salaries in Europepolymath100% (6)

- Model Scottish Budget 2018/19 (June 2018)Dokument10 SeitenModel Scottish Budget 2018/19 (June 2018)msp-archiveNoch keine Bewertungen

- Nationality Detailed LondonDokument8 SeitenNationality Detailed LondonOe FreeglutenNoch keine Bewertungen

- OCDE Country Risk Analysis of PeruDokument4 SeitenOCDE Country Risk Analysis of PeruNicole GonzalesNoch keine Bewertungen

- Webinar On Latin America Project UpdateDokument47 SeitenWebinar On Latin America Project UpdateAdriana GarayNoch keine Bewertungen

- Market Analysis IVD ColombiaDokument6 SeitenMarket Analysis IVD ColombiaThimo KleinNoch keine Bewertungen

- Felony Affair Sales EstimatesDokument2 SeitenFelony Affair Sales EstimatesSEYOUNG LeeNoch keine Bewertungen

- Interim Report For The 4 Quarter and Year-End 2020: 1 January To 31 December 2020Dokument9 SeitenInterim Report For The 4 Quarter and Year-End 2020: 1 January To 31 December 2020Elias TalaniNoch keine Bewertungen

- COVID-19: Global Shutdown Impacts Business EconomicsDokument9 SeitenCOVID-19: Global Shutdown Impacts Business Economicsvnv servicesNoch keine Bewertungen

- Angler Gaming PLC Q3 Report 2020 FINALDokument9 SeitenAngler Gaming PLC Q3 Report 2020 FINALEmil Elias TalaniNoch keine Bewertungen

- 7-Risk and Real Options in Capital BudgetingDokument38 Seiten7-Risk and Real Options in Capital BudgetingSameerbaskarNoch keine Bewertungen

- Emergency Response Master Budget FormatDokument51 SeitenEmergency Response Master Budget FormatNaveed UllahNoch keine Bewertungen

- Geothermal Power Generation in The World 2015-2020 Update ReportDokument17 SeitenGeothermal Power Generation in The World 2015-2020 Update ReportergtewfgergNoch keine Bewertungen

- A Map of Forex TradersDokument5 SeitenA Map of Forex TradersLooseNoch keine Bewertungen

- Financial Model 1Dokument1 SeiteFinancial Model 1ahmedmostafaibrahim22Noch keine Bewertungen

- 2016 - Exercícios Resolvidos TIR VPLDokument5 Seiten2016 - Exercícios Resolvidos TIR VPLIVAN CHAVEZNoch keine Bewertungen

- Intrastat Threshold TableDokument1 SeiteIntrastat Threshold TableJulian LiciNoch keine Bewertungen

- S07 Desfelurs V3Dokument2 SeitenS07 Desfelurs V3Khushi singhalNoch keine Bewertungen

- Prob1 Afar QuizDokument7 SeitenProb1 Afar Quizryan rosalesNoch keine Bewertungen

- Calculate expected loss for loan portfolioDokument6 SeitenCalculate expected loss for loan portfoliodevilsnitchNoch keine Bewertungen

- Atheist Pop StatsDokument6 SeitenAtheist Pop Statsrictus11Noch keine Bewertungen

- Loan Schedule: Comparable CompaniesDokument30 SeitenLoan Schedule: Comparable CompaniesIrene Mae GuerraNoch keine Bewertungen

- Taller 2Dokument2 SeitenTaller 2dalozanosNoch keine Bewertungen

- Simulasi PL Quotation MR RudyDokument7 SeitenSimulasi PL Quotation MR RudySandi IrNoch keine Bewertungen

- Acc 2112: Accounting Theory and Practice Assignment (February 2021)Dokument6 SeitenAcc 2112: Accounting Theory and Practice Assignment (February 2021)Ranson MerciecaNoch keine Bewertungen

- Slide Show MKTGDokument26 SeitenSlide Show MKTGAzad MohammedNoch keine Bewertungen

- Operation Expenses and Sales Analysis for Stationery Business Over 5 YearsDokument31 SeitenOperation Expenses and Sales Analysis for Stationery Business Over 5 YearsJanine PadillaNoch keine Bewertungen

- Intercompany Sale of Merchandise - AdditionalDokument4 SeitenIntercompany Sale of Merchandise - AdditionalJaimell LimNoch keine Bewertungen

- Cash Flows 1Dokument2 SeitenCash Flows 1ssembatya reaganNoch keine Bewertungen

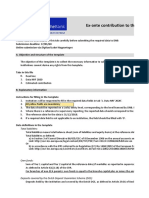

- Ex-Ante Contribution To The National Resolution Fund - 2020 Contribution PeriodDokument10 SeitenEx-Ante Contribution To The National Resolution Fund - 2020 Contribution PeriodgrobbebolNoch keine Bewertungen

- Angler Gaming Reports Record Q1 RevenuesDokument9 SeitenAngler Gaming Reports Record Q1 RevenuesAnton HenrikssonNoch keine Bewertungen

- Accounting worksheet analysisDokument2 SeitenAccounting worksheet analysisIshanNoch keine Bewertungen

- Stats VictimsDokument1 SeiteStats Victimsmatheourvoy00Noch keine Bewertungen

- Mahyoro Ace Cash Flow Statemet 2020-2021Dokument4 SeitenMahyoro Ace Cash Flow Statemet 2020-2021ssembatya reaganNoch keine Bewertungen

- Supershop Fianal For Balance SheetDokument21 SeitenSupershop Fianal For Balance SheetMohammad Osman GoniNoch keine Bewertungen

- Table2 5Dokument3 SeitenTable2 5Alexander 'Tory' HinchliffeNoch keine Bewertungen

- Fundamental of Business & Finance Term Project Financial ReportDokument6 SeitenFundamental of Business & Finance Term Project Financial ReportAfaq BhuttaNoch keine Bewertungen

- Offshore Wind Industry Market Forecast to Exceed 60GW by 2020Dokument3 SeitenOffshore Wind Industry Market Forecast to Exceed 60GW by 2020bijo_menacheryNoch keine Bewertungen

- 7.MLM 0689 TribeQa Booklet TheFinancialsDokument33 Seiten7.MLM 0689 TribeQa Booklet TheFinancialstribeqaNoch keine Bewertungen

- RR 02-40Dokument137 SeitenRR 02-40Nikki ChuaNoch keine Bewertungen

- Feasibility Final V2Dokument7 SeitenFeasibility Final V2Sohail MahmoodNoch keine Bewertungen

- 7457 Uslugi I Cenovnik Na Erdem Klinka IstanbulDokument3 Seiten7457 Uslugi I Cenovnik Na Erdem Klinka Istanbuljove11Noch keine Bewertungen

- Glo DGF Ocean Market UpdateDokument23 SeitenGlo DGF Ocean Market UpdateKicki AnderssonNoch keine Bewertungen

- Subject Code:: Prepared byDokument6 SeitenSubject Code:: Prepared byDarmmini MiniNoch keine Bewertungen

- Taxes and Economic GrowthDokument24 SeitenTaxes and Economic GrowthSadamNoch keine Bewertungen

- Pricelist 2020: Risk Management SoftwareDokument1 SeitePricelist 2020: Risk Management SoftwareJimmy SilvaNoch keine Bewertungen

- Resources and Enforcement Actions of EU Data Protection AuthoritiesDokument31 SeitenResources and Enforcement Actions of EU Data Protection AuthoritiesDuckifiyNoch keine Bewertungen

- Financial Plan: and Economic ChallengesDokument5 SeitenFinancial Plan: and Economic ChallengesEmmanuel AkoloNoch keine Bewertungen

- No. Marketplace Product Design Quantity Marking (GBP) Total Quantity Profit (GBP)Dokument2 SeitenNo. Marketplace Product Design Quantity Marking (GBP) Total Quantity Profit (GBP)Deden Dodik GinanjarNoch keine Bewertungen

- Church of SwedenDokument9 SeitenChurch of SwedenBeatrice AnaelyNoch keine Bewertungen

- Is Venezuela Approaching To Default?: Prof. Luis AngaritaDokument12 SeitenIs Venezuela Approaching To Default?: Prof. Luis AngaritaattilioucvNoch keine Bewertungen

- CFS Lecture 2 Part 2Dokument7 SeitenCFS Lecture 2 Part 2R VNoch keine Bewertungen

- Assignmnet ROEDokument6 SeitenAssignmnet ROEmadam iqraNoch keine Bewertungen

- Note On Tax Rebate On Takaful Contribution 2019 20 SalariedDokument1 SeiteNote On Tax Rebate On Takaful Contribution 2019 20 SalariedRoy Estate (Sajila Roy)Noch keine Bewertungen

- Financial ProjectionDokument55 SeitenFinancial ProjectionVinayak SilverlineswapNoch keine Bewertungen

- PR 117 Part 2Dokument9 SeitenPR 117 Part 2viswadevassociates.tvmNoch keine Bewertungen

- Partnership Liquidation by Instalment (Safe Payment)Dokument3 SeitenPartnership Liquidation by Instalment (Safe Payment)Krizzia MayNoch keine Bewertungen

- Latihan Perpetual PT CEMERLANGDokument28 SeitenLatihan Perpetual PT CEMERLANGSamsul PangestuNoch keine Bewertungen

- Cosmetology & Barber School Revenues World Summary: Market Values & Financials by CountryVon EverandCosmetology & Barber School Revenues World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- Food Service Contractor Revenues World Summary: Market Values & Financials by CountryVon EverandFood Service Contractor Revenues World Summary: Market Values & Financials by CountryNoch keine Bewertungen

- ACCAF7 CourseNotes2015 2ndhalfDokument174 SeitenACCAF7 CourseNotes2015 2ndhalfMayank Gupta100% (1)

- PT Usaha Agro Indonesia Audit ReportDokument106 SeitenPT Usaha Agro Indonesia Audit ReportAdri Ayah BaimNoch keine Bewertungen

- Fundamentals of Advanced Accounting 8th Edition Hoyle Solutions Manual 1Dokument36 SeitenFundamentals of Advanced Accounting 8th Edition Hoyle Solutions Manual 1toddvaldezamzxfwnrtq100% (25)

- Celex 32021L2101 en TXTDokument14 SeitenCelex 32021L2101 en TXTlNoch keine Bewertungen

- Consultation of The Code Response Paper 23 Mar 2012 Annex 2Dokument202 SeitenConsultation of The Code Response Paper 23 Mar 2012 Annex 2BubblyDeliciousNoch keine Bewertungen

- XADVAC2 Notes To BuscomDokument4 SeitenXADVAC2 Notes To Buscomonay dogNoch keine Bewertungen

- Consolidation TheoriesDokument5 SeitenConsolidation TheoriesAyan RoyNoch keine Bewertungen

- Audit of CFSDokument30 SeitenAudit of CFSDhivyaNoch keine Bewertungen

- Lecture Notes ON Business Law and Business Environment MBA I Semester (Autonomous-R16)Dokument98 SeitenLecture Notes ON Business Law and Business Environment MBA I Semester (Autonomous-R16)Prakash ReddyNoch keine Bewertungen

- Tendernotice 2Dokument10 SeitenTendernotice 2arunghandwalNoch keine Bewertungen

- Understanding Transfer Pricing in 38 charsDokument18 SeitenUnderstanding Transfer Pricing in 38 charsMD Hafizul Islam HafizNoch keine Bewertungen

- MFRS11 Joint Arrangements MFRS12 Disclosure of Interests in Other Entities MFRS5 Non-Current Assets Held For Sale &Dokument20 SeitenMFRS11 Joint Arrangements MFRS12 Disclosure of Interests in Other Entities MFRS5 Non-Current Assets Held For Sale &cynthiama7777Noch keine Bewertungen

- ConsolidationDokument3 SeitenConsolidationkonyatanNoch keine Bewertungen

- Calang vs. People (G.R. No. 190696 August 3, 2010) - Case DigestDokument2 SeitenCalang vs. People (G.R. No. 190696 August 3, 2010) - Case DigestAmir Nazri KaibingNoch keine Bewertungen

- Due Diligence Data Room ChecklistDokument10 SeitenDue Diligence Data Room ChecklistanishsinglaNoch keine Bewertungen

- 2GO: H1 ResultsDokument99 Seiten2GO: H1 ResultsBusinessWorldNoch keine Bewertungen

- Associates and Joint Ventures: Chapter AimDokument41 SeitenAssociates and Joint Ventures: Chapter AimJacx 'sNoch keine Bewertungen

- Letter of Comfort - ENDokument2 SeitenLetter of Comfort - ENmarce_sarria100% (3)

- Corporate Structure FormationDokument22 SeitenCorporate Structure FormationSHASHANK RAJ RP100% (2)

- Lecture 02Dokument29 SeitenLecture 02ArrowNoch keine Bewertungen

- Global Information Systems: Group 1Dokument24 SeitenGlobal Information Systems: Group 1Jonnalyn CañadaNoch keine Bewertungen

- G.R. No. 83896Dokument5 SeitenG.R. No. 83896yannie11Noch keine Bewertungen

- CA Intermediate Paper-2Dokument334 SeitenCA Intermediate Paper-2Anand_Agrawal19100% (2)

- Nature and Formation of A CompanyDokument15 SeitenNature and Formation of A CompanyCOLLINS MWANGI NJOROGENoch keine Bewertungen

- New Company Law AssignmentDokument11 SeitenNew Company Law AssignmentAshish pariharNoch keine Bewertungen

- CH 16Dokument12 SeitenCH 16DaleClemence09100% (1)

- Summary of IFRS 12Dokument3 SeitenSummary of IFRS 12Dwight BentNoch keine Bewertungen

- The Companies Act, 2013: Learning OutcomesDokument40 SeitenThe Companies Act, 2013: Learning OutcomesYogesh sharmaNoch keine Bewertungen

- Provision For Consolidation of Financial StatementDokument7 SeitenProvision For Consolidation of Financial StatementAshokNoch keine Bewertungen

- MRTP Act, 1969Dokument46 SeitenMRTP Act, 1969avijitnlsNoch keine Bewertungen