Das könnte Ihnen auch gefallen

- Decision MakingDokument28 SeitenDecision MakingJem ColebraNoch keine Bewertungen

- Short-Term Financing - Extra CreditDokument7 SeitenShort-Term Financing - Extra CreditEnola HolmesNoch keine Bewertungen

- CVP AnalysisDokument17 SeitenCVP AnalysisDave AguilaNoch keine Bewertungen

- Corporate Officers: 2. All Are Methods of Voting Except: Methods of VotingDokument44 SeitenCorporate Officers: 2. All Are Methods of Voting Except: Methods of VotingNicolas BrentNoch keine Bewertungen

- Responsibility Accounting: Acctg 205: Management ScienceDokument34 SeitenResponsibility Accounting: Acctg 205: Management ScienceEliseNoch keine Bewertungen

- Sunu 2Dokument1 SeiteSunu 2ahmedNoch keine Bewertungen

- Accounting For LaborDokument1 SeiteAccounting For LaborkwekwkNoch keine Bewertungen

- Summarized Notes: Let'S Go!Dokument7 SeitenSummarized Notes: Let'S Go!Naiv Yer NagaliNoch keine Bewertungen

- Short Term Decision Making (OK Na!)Dokument12 SeitenShort Term Decision Making (OK Na!)daemonspadechocoy100% (1)

- Problems On Working CapitalDokument2 SeitenProblems On Working CapitalDeepakNoch keine Bewertungen

- AE 23 - Short Term Decisions - Accounting InformationsDokument13 SeitenAE 23 - Short Term Decisions - Accounting InformationsAzureBlazeNoch keine Bewertungen

- ReceivablesDokument17 SeitenReceivablesJaspreet GillNoch keine Bewertungen

- Shutting Down or Continuing To Operate A Plant - Hallas CompanyDokument3 SeitenShutting Down or Continuing To Operate A Plant - Hallas CompanyFernando III PerezNoch keine Bewertungen

- 2Dokument13 Seiten2Ashish BhallaNoch keine Bewertungen

- Our Lady of The Pillar College - CauayanDokument5 SeitenOur Lady of The Pillar College - CauayanLu CioNoch keine Bewertungen

- Operating Budget DiscussionDokument3 SeitenOperating Budget DiscussionDavin DavinNoch keine Bewertungen

- De Leon Solman 2014 2 CostDokument95 SeitenDe Leon Solman 2014 2 CostJohn Laurence LoplopNoch keine Bewertungen

- Session 3 - Deductions From Gross Income - Principles and Regular Itemized DeductionsDokument9 SeitenSession 3 - Deductions From Gross Income - Principles and Regular Itemized DeductionsMitzi WamarNoch keine Bewertungen

- Multiple Choice Questions Plus Solutions Flexible Budget and Standard CostingDokument5 SeitenMultiple Choice Questions Plus Solutions Flexible Budget and Standard Costingnhu nhuNoch keine Bewertungen

- Problems On Pricing DecisionsDokument15 SeitenProblems On Pricing DecisionsMae-shane SagayoNoch keine Bewertungen

- Cost Accounting Procedure For Spoiled GoodsDokument3 SeitenCost Accounting Procedure For Spoiled GoodszachNoch keine Bewertungen

- Finman Midterms Part 1Dokument7 SeitenFinman Midterms Part 1JerichoNoch keine Bewertungen

- Financial Management BSATDokument9 SeitenFinancial Management BSATEma Dupilas GuianalanNoch keine Bewertungen

- CVP Multiple Product DiscussionDokument5 SeitenCVP Multiple Product DiscussionheyheyNoch keine Bewertungen

- QCH 16Dokument4 SeitenQCH 16hppddlNoch keine Bewertungen

- Job Order Costing HandoutsDokument8 SeitenJob Order Costing HandoutsHannah Jane Arevalo LafuenteNoch keine Bewertungen

- Mock Deparmentals MASQDokument6 SeitenMock Deparmentals MASQHannah Joyce MirandaNoch keine Bewertungen

- 18 x12 ABC ADokument12 Seiten18 x12 ABC AKM MacatangayNoch keine Bewertungen

- Ifrs 5 Acca AnswersDokument2 SeitenIfrs 5 Acca AnswersMonirul Islam MoniirrNoch keine Bewertungen

- Corporate Governance Business Ethics Risk Management and Internal Control CH 1 2 PDFDokument11 SeitenCorporate Governance Business Ethics Risk Management and Internal Control CH 1 2 PDFEu NiceNoch keine Bewertungen

- High Low Method: - Method For Estimating Fixed and Variable Cost. - Variable CostDokument7 SeitenHigh Low Method: - Method For Estimating Fixed and Variable Cost. - Variable CostshompaNoch keine Bewertungen

- Mas-07: Responsibility Accounting & Transfer PricingDokument7 SeitenMas-07: Responsibility Accounting & Transfer PricingClint AbenojaNoch keine Bewertungen

- Cost ManagementDokument4 SeitenCost ManagementTrọng ĐỗNoch keine Bewertungen

- High Low MethodDokument4 SeitenHigh Low MethodMwandoza MnyiphapheiNoch keine Bewertungen

- Joint Product CostingDokument3 SeitenJoint Product CostingClint-Daniel AbenojaNoch keine Bewertungen

- Financial Accounting Questions and Solutions Chapter 3Dokument7 SeitenFinancial Accounting Questions and Solutions Chapter 3bazil360Noch keine Bewertungen

- Activitybased Costing May 20 GMSISUCCESSDokument29 SeitenActivitybased Costing May 20 GMSISUCCESSChetan BasraNoch keine Bewertungen

- Saint Theresa College of Tandag, Inc. Tandag City Strategic Cost Management - Summer Class Dit 1Dokument4 SeitenSaint Theresa College of Tandag, Inc. Tandag City Strategic Cost Management - Summer Class Dit 1Esheikell ChenNoch keine Bewertungen

- Quizzes in Cost AccountingDokument31 SeitenQuizzes in Cost AccountingRicalyn BugarinNoch keine Bewertungen

- Mas Ho No. 2 Relevant CostingDokument7 SeitenMas Ho No. 2 Relevant CostingRenz Francis LimNoch keine Bewertungen

- MSC-Audited FS With Notes - 2014 - CaseDokument12 SeitenMSC-Audited FS With Notes - 2014 - CaseMikaela SalvadorNoch keine Bewertungen

- Job and Batch CostingDokument7 SeitenJob and Batch CostingDeepak R GoradNoch keine Bewertungen

- GOVBUSMAN MODULE 6 - Chapter 7Dokument6 SeitenGOVBUSMAN MODULE 6 - Chapter 7Gian TolentinoNoch keine Bewertungen

- Master in Managerial Advisory Services: Easy QuestionsDokument13 SeitenMaster in Managerial Advisory Services: Easy QuestionsKervin Rey JacksonNoch keine Bewertungen

- Chapter 1-Introduction To Cost AccountingDokument25 SeitenChapter 1-Introduction To Cost AccountingjepsyutNoch keine Bewertungen

- Exam On Strategic ManagementDokument11 SeitenExam On Strategic Managementeulhiemae arongNoch keine Bewertungen

- Cost AccountingDokument6 SeitenCost Accountingulquira grimamajowNoch keine Bewertungen

- Chapter 20 - AnswerDokument4 SeitenChapter 20 - AnsweragnesNoch keine Bewertungen

- 1.3 Responsibility Accounting Problems AnswersDokument5 Seiten1.3 Responsibility Accounting Problems AnswersAsnarizah PakinsonNoch keine Bewertungen

- Chapter 6: Self-Test Taxation Discussion QuestionsDokument9 SeitenChapter 6: Self-Test Taxation Discussion QuestionsUnnamed homosapienNoch keine Bewertungen

- FARAP 4404 Property Plant EquipmentDokument11 SeitenFARAP 4404 Property Plant EquipmentJohn Ray RonaNoch keine Bewertungen

- Ac2102 TPDokument6 SeitenAc2102 TPNors PataytayNoch keine Bewertungen

- Accounting For Joint Products and by ProductsDokument13 SeitenAccounting For Joint Products and by ProductsSteffi CabalunaNoch keine Bewertungen

- ACC102-Chapter10new 000Dokument28 SeitenACC102-Chapter10new 000Mikee FactoresNoch keine Bewertungen

- Differential Analysis: The Key To Decision MakingDokument25 SeitenDifferential Analysis: The Key To Decision MakingJhinglee Sacupayo Gocela100% (1)

- Ac102 ch11Dokument19 SeitenAc102 ch11Yenny Torro100% (1)

- Chapter 7 ReviewDokument8 SeitenChapter 7 ReviewRenzo RamosNoch keine Bewertungen

- Session 08: Tactical Decision MakingDokument18 SeitenSession 08: Tactical Decision MakingFrancisco Pedro SantosNoch keine Bewertungen

- Variable Costing: A Decision-Making Perspective: True-False StatementsDokument8 SeitenVariable Costing: A Decision-Making Perspective: True-False StatementsJanina Marie GarciaNoch keine Bewertungen

- Responsibility Accounting Decision MakingDokument32 SeitenResponsibility Accounting Decision MakingChokie NavarroNoch keine Bewertungen

- BP MidtermDokument4 SeitenBP MidtermGelyn CruzNoch keine Bewertungen

- A. B. C. D. E. F. G. H. I. J.: Speeches For All OccassionsDokument1 SeiteA. B. C. D. E. F. G. H. I. J.: Speeches For All OccassionsGelyn CruzNoch keine Bewertungen

- Ais 1Dokument48 SeitenAis 1Gelyn CruzNoch keine Bewertungen

- Chapter 24Dokument20 SeitenChapter 24Gelyn CruzNoch keine Bewertungen

- CRC-ACE PW-TaxDokument14 SeitenCRC-ACE PW-TaxGelyn CruzNoch keine Bewertungen

- Chapter 12Dokument27 SeitenChapter 12Gelyn CruzNoch keine Bewertungen

- Chapter 8Dokument6 SeitenChapter 8Gelyn CruzNoch keine Bewertungen

- Bsa 1Dokument110 SeitenBsa 1Gelyn CruzNoch keine Bewertungen

- Accounting Information SystemDokument48 SeitenAccounting Information SystemGelyn CruzNoch keine Bewertungen

- Reaction PaperDokument3 SeitenReaction PaperGelyn CruzNoch keine Bewertungen

- MS - EconomicsDokument16 SeitenMS - EconomicsGelyn CruzNoch keine Bewertungen

- Research Questionnaire: TH TH THDokument4 SeitenResearch Questionnaire: TH TH THGelyn CruzNoch keine Bewertungen

- Phase I-Risk Assessment Planning The AudDokument21 SeitenPhase I-Risk Assessment Planning The AudGelyn CruzNoch keine Bewertungen

- John Gokongwei1Dokument4 SeitenJohn Gokongwei1Gelyn CruzNoch keine Bewertungen

- Test Bank Chapter 1 Managerial AccountingDokument9 SeitenTest Bank Chapter 1 Managerial AccountingGelyn CruzNoch keine Bewertungen

- Responsibility Acctg, Transfer Pricing & GP AnalysisDokument21 SeitenResponsibility Acctg, Transfer Pricing & GP AnalysisGelyn CruzNoch keine Bewertungen

- 1iab SampleDokument52 Seiten1iab SampleGelyn CruzNoch keine Bewertungen

- Auditing Theory TEST BANKDokument23 SeitenAuditing Theory TEST BANKGelyn CruzNoch keine Bewertungen

- Thesis Pattern ItDokument1 SeiteThesis Pattern ItGelyn CruzNoch keine Bewertungen

- Chapter 11 Cash Flow Estimation and Risk Analysis PDFDokument80 SeitenChapter 11 Cash Flow Estimation and Risk Analysis PDFGelyn Cruz100% (1)

- Thesis It To Be FinalizeDokument29 SeitenThesis It To Be FinalizeGelyn CruzNoch keine Bewertungen

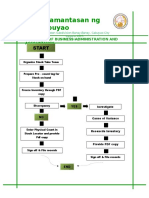

- Pamantasan NG Cabuyao: College of Business Administration and AccountancyDokument1 SeitePamantasan NG Cabuyao: College of Business Administration and AccountancyGelyn CruzNoch keine Bewertungen

- Module HandbookDokument307 SeitenModule HandbookHenry So E DiarkoNoch keine Bewertungen

- W. H. Elliott & Sons Co., Inc. v. Charles J. Gotthardt, 305 F.2d 544, 1st Cir. (1962)Dokument6 SeitenW. H. Elliott & Sons Co., Inc. v. Charles J. Gotthardt, 305 F.2d 544, 1st Cir. (1962)Scribd Government DocsNoch keine Bewertungen

- Chapter5 Project PlanningDokument38 SeitenChapter5 Project PlanningSanchit BatraNoch keine Bewertungen

- Intellectual Capital Is The Collective Brainpower or Shared Knowledge of A WorkforceDokument3 SeitenIntellectual Capital Is The Collective Brainpower or Shared Knowledge of A WorkforceKatherine Rosette ChanNoch keine Bewertungen

- Fixed Cost Vs Variable CostDokument24 SeitenFixed Cost Vs Variable Costsrk_soumyaNoch keine Bewertungen

- Journal of Intellectual CapitalDokument14 SeitenJournal of Intellectual Capitalcicik watiNoch keine Bewertungen

- Appendix 32 BrgyDokument4 SeitenAppendix 32 BrgyJovelyn SeseNoch keine Bewertungen

- Mian Muhammad Ateeq SheikhDokument2 SeitenMian Muhammad Ateeq SheikhAashq LoveNoch keine Bewertungen

- DO-178B Compliance: Turn An Overhead Expense Into A Competitive AdvantageDokument12 SeitenDO-178B Compliance: Turn An Overhead Expense Into A Competitive Advantagedamianpri84Noch keine Bewertungen

- Mplus FormDokument4 SeitenMplus Formmohd fairusNoch keine Bewertungen

- MIT CASE Competition 2014 PresentationDokument15 SeitenMIT CASE Competition 2014 PresentationJonathan D SmithNoch keine Bewertungen

- Ecommerce in IndiaDokument24 SeitenEcommerce in Indiaintellectarun100% (2)

- Sip ReportDokument114 SeitenSip Reportprincy chauhanNoch keine Bewertungen

- J2EE Design PatternDokument36 SeitenJ2EE Design Patternsunny_ratra100% (1)

- SEB - ISO - XML Message For Payment InitiationDokument75 SeitenSEB - ISO - XML Message For Payment InitiationbpvsvNoch keine Bewertungen

- The Merchant of Venice CrosswordDokument2 SeitenThe Merchant of Venice CrosswordAnonymous lTXTx1fNoch keine Bewertungen

- Far 7 Flashcards - QuizletDokument31 SeitenFar 7 Flashcards - QuizletnikoladjonajNoch keine Bewertungen

- Natalie ResumeDokument1 SeiteNatalie Resumeapi-430414382Noch keine Bewertungen

- Report Sample-Supplier Factory AuditDokument24 SeitenReport Sample-Supplier Factory AuditCarlosSánchezNoch keine Bewertungen

- Final Quiz and SeatworkDokument3 SeitenFinal Quiz and SeatworkMikaela SungaNoch keine Bewertungen

- Counter-Brand and Alter-Brand Communities: The Impact of Web 2.0 On Tribal Marketing ApproachesDokument16 SeitenCounter-Brand and Alter-Brand Communities: The Impact of Web 2.0 On Tribal Marketing ApproachesJosefBaldacchinoNoch keine Bewertungen

- 17 SDDDokument6 Seiten17 SDDioi123Noch keine Bewertungen

- Daclag Vs MacahiligDokument2 SeitenDaclag Vs MacahiligkimuchosNoch keine Bewertungen

- Marko Dameski Market Leader Test 2 1608569513366Dokument12 SeitenMarko Dameski Market Leader Test 2 1608569513366krkaNoch keine Bewertungen

- Invoice INV-0030Dokument1 SeiteInvoice INV-0030Threshing FlowNoch keine Bewertungen

- Quality ImprovementDokument5 SeitenQuality Improvementzul0867Noch keine Bewertungen

- HSEObservationStatistics 15dec2023 112923Dokument8 SeitenHSEObservationStatistics 15dec2023 112923Bhagat DeepakNoch keine Bewertungen

- Financial Management: Week 10Dokument10 SeitenFinancial Management: Week 10sanjeev parajuliNoch keine Bewertungen

- BaanERP 5.0b OLE User ManualDokument38 SeitenBaanERP 5.0b OLE User ManualZealongaNoch keine Bewertungen

- Bank Statement Apr2022 Jan2023 - WPW 14 26 - 004Dokument13 SeitenBank Statement Apr2022 Jan2023 - WPW 14 26 - 004Adarsh RavindraNoch keine Bewertungen