Das könnte Ihnen auch gefallen

- Senarai Produk SawitDokument16 SeitenSenarai Produk SawitYuliana PohanNoch keine Bewertungen

- VIV Asia 2019 - Floor Plan 3D PDFDokument1 SeiteVIV Asia 2019 - Floor Plan 3D PDFYuliana PohanNoch keine Bewertungen

- Fysal From SelkoDokument2 SeitenFysal From SelkoYuliana PohanNoch keine Bewertungen

- Oxistat TdsDokument1 SeiteOxistat TdsYuliana PohanNoch keine Bewertungen

- Proteferm As A Pellet BinderDokument2 SeitenProteferm As A Pellet BinderYuliana PohanNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Cary Conger Debunks Adam Ledford's Sac City Street Improvement Project Explanation Letter in The January 8, 2013 Sac SunDokument3 SeitenCary Conger Debunks Adam Ledford's Sac City Street Improvement Project Explanation Letter in The January 8, 2013 Sac SunthesacnewsNoch keine Bewertungen

- Chapter - 18 PFPDokument4 SeitenChapter - 18 PFPaliNoch keine Bewertungen

- Basics of Income Tax of India PDFDokument19 SeitenBasics of Income Tax of India PDFJai VermaNoch keine Bewertungen

- Aec10 - Business Taxation Solution Tabag CH4Dokument8 SeitenAec10 - Business Taxation Solution Tabag CH4EdeksupligNoch keine Bewertungen

- Trend Analysis RevisedDokument3 SeitenTrend Analysis RevisedVandita KhudiaNoch keine Bewertungen

- Bill 10352986Dokument1 SeiteBill 10352986Sunil NainNoch keine Bewertungen

- 201 East 4th Street, Suite 800 Cincinnati OH 45202 513.852.4899Dokument1 Seite201 East 4th Street, Suite 800 Cincinnati OH 45202 513.852.4899Tera's TarotNoch keine Bewertungen

- Sesi 7 - Skyview Manor CaseDokument3 SeitenSesi 7 - Skyview Manor CasestevenNoch keine Bewertungen

- TAXATIONDokument2 SeitenTAXATIONJoshua BrownNoch keine Bewertungen

- The University of Lahore College of Law Fee Structure Fall 2021 Bachelor of Law BallbDokument1 SeiteThe University of Lahore College of Law Fee Structure Fall 2021 Bachelor of Law BallbAli SohuNoch keine Bewertungen

- Nepali Talim Youtube Channel: Calculation of Salary Tax For Social Security Listed OrgDokument20 SeitenNepali Talim Youtube Channel: Calculation of Salary Tax For Social Security Listed OrgsamNoch keine Bewertungen

- Credit Note: (Original For Recipient)Dokument2 SeitenCredit Note: (Original For Recipient)Swetha WariNoch keine Bewertungen

- Digital Order: Feb. 26 2022: Details For Order # D01-7940294-2662636Dokument1 SeiteDigital Order: Feb. 26 2022: Details For Order # D01-7940294-2662636AssignmentHelp OnlineNoch keine Bewertungen

- Case 5-33 (Pittman) - 1Dokument12 SeitenCase 5-33 (Pittman) - 1MOHAK ANANDNoch keine Bewertungen

- Tandem Activity GE Allowable DeductionsDokument6 SeitenTandem Activity GE Allowable DeductionsErin CruzNoch keine Bewertungen

- IRS Issues Guidance On State Tax Payments To Help TaxpayersDokument2 SeitenIRS Issues Guidance On State Tax Payments To Help TaxpayersMeaghan BellavanceNoch keine Bewertungen

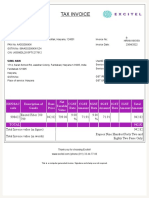

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Dokument1 SeiteTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)VJ VOXNoch keine Bewertungen

- Taxation Review Course Syllabus PDFDokument21 SeitenTaxation Review Course Syllabus PDFJordan ChavezNoch keine Bewertungen

- RSM Itrv 2019-20Dokument1 SeiteRSM Itrv 2019-20Rajesh KumarNoch keine Bewertungen

- Shambhu Med.Dokument1 SeiteShambhu Med.Rajeev KejriwalNoch keine Bewertungen

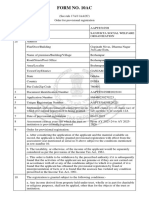

- Form No. 10acDokument2 SeitenForm No. 10acAditya NayakNoch keine Bewertungen

- Agatha Is Planning To Start A New Business Venture and PDFDokument1 SeiteAgatha Is Planning To Start A New Business Venture and PDFDoreenNoch keine Bewertungen

- Allowable Deductions Itemized Deductions (Sec 34, NIRC)Dokument9 SeitenAllowable Deductions Itemized Deductions (Sec 34, NIRC)Angela ParadoNoch keine Bewertungen

- PDF DocumentDokument1 SeitePDF DocumentAngelo DiloneNoch keine Bewertungen

- The Following Information Is Available For Bott Company Additional Information ForDokument1 SeiteThe Following Information Is Available For Bott Company Additional Information ForTaimur TechnologistNoch keine Bewertungen

- InvoiceDokument1 SeiteInvoiceNiraj kumarNoch keine Bewertungen

- Income Tax AuthoritiesDokument3 SeitenIncome Tax AuthoritiesWaqas AjmeryNoch keine Bewertungen

- HGDokument3 SeitenHGGreg MarilynNoch keine Bewertungen

- Payslip Daily Rate: 373.00Dokument48 SeitenPayslip Daily Rate: 373.00Nichole John ErnietaNoch keine Bewertungen

- CIR v. AcesiteDokument5 SeitenCIR v. AcesitePaul Joshua SubaNoch keine Bewertungen