Das könnte Ihnen auch gefallen

- New IAR Key Audit MattersDokument4 SeitenNew IAR Key Audit Mattersjulie anne mae mendozaNoch keine Bewertungen

- BIR EFPS Quick GuideDokument2 SeitenBIR EFPS Quick Guidejulie anne mae mendozaNoch keine Bewertungen

- Mendoza Written ReportDokument6 SeitenMendoza Written Reportjulie anne mae mendozaNoch keine Bewertungen

- Y 1H"? J:fr?i"k: p6,135,933 p6,140,433 C. p6,10g, 333Dokument1 SeiteY 1H"? J:fr?i"k: p6,135,933 p6,140,433 C. p6,10g, 333julie anne mae mendozaNoch keine Bewertungen

- Bus - Strat. ReviewerDokument21 SeitenBus - Strat. Reviewerjulie anne mae mendozaNoch keine Bewertungen

- Administrative and Finance Department Accounting DivisionDokument10 SeitenAdministrative and Finance Department Accounting Divisionjulie anne mae mendozaNoch keine Bewertungen

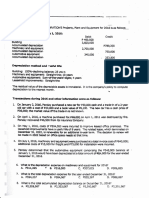

- Amunt: Foilows:-FanualyDokument1 SeiteAmunt: Foilows:-Fanualyjulie anne mae mendozaNoch keine Bewertungen

- Recipe Ham & Cheese Pizza CupcakeDokument3 SeitenRecipe Ham & Cheese Pizza Cupcakejulie anne mae mendozaNoch keine Bewertungen

- Audit Rev 1Dokument1 SeiteAudit Rev 1julie anne mae mendozaNoch keine Bewertungen

- AutobiographyDokument2 SeitenAutobiographyjulie anne mae mendoza83% (6)

- Work SchedDokument1 SeiteWork Schedjulie anne mae mendozaNoch keine Bewertungen

- D. All of The Above Are RequiredDokument2 SeitenD. All of The Above Are Requiredjulie anne mae mendozaNoch keine Bewertungen

- Assignment in MathDokument4 SeitenAssignment in Mathjulie anne mae mendozaNoch keine Bewertungen

- Painting: Ranch Cliffs (Fig 4-12)Dokument15 SeitenPainting: Ranch Cliffs (Fig 4-12)julie anne mae mendoza100% (1)

- Ojt DTRDokument1 SeiteOjt DTRjulie anne mae mendozaNoch keine Bewertungen

- SculptureDokument13 SeitenSculpturejulie anne mae mendozaNoch keine Bewertungen

- Waiver Form: Signature of Student Over Printed NameDokument1 SeiteWaiver Form: Signature of Student Over Printed Namejulie anne mae mendozaNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- 09 WA500-3 Shop ManualDokument1.335 Seiten09 WA500-3 Shop ManualCristhian Gutierrez Tamayo93% (14)

- Tradingview ShortcutsDokument2 SeitenTradingview Shortcutsrprasannaa2002Noch keine Bewertungen

- 3125 Vitalogic 4000 PDFDokument444 Seiten3125 Vitalogic 4000 PDFvlaimirNoch keine Bewertungen

- RENCANA KERJA Serious Inspeksi#3 Maret-April 2019Dokument2 SeitenRENCANA KERJA Serious Inspeksi#3 Maret-April 2019Nur Ali SaidNoch keine Bewertungen

- Polytropic Process1Dokument4 SeitenPolytropic Process1Manash SinghaNoch keine Bewertungen

- EXTENDED PROJECT-Shoe - SalesDokument28 SeitenEXTENDED PROJECT-Shoe - Salesrhea100% (5)

- How To Create A Powerful Brand Identity (A Step-by-Step Guide) PDFDokument35 SeitenHow To Create A Powerful Brand Identity (A Step-by-Step Guide) PDFCaroline NobreNoch keine Bewertungen

- CI Principles of EconomicsDokument833 SeitenCI Principles of EconomicsJamieNoch keine Bewertungen

- Manual 40ku6092Dokument228 SeitenManual 40ku6092Marius Stefan BerindeNoch keine Bewertungen

- 5 Star Hotels in Portugal Leads 1Dokument9 Seiten5 Star Hotels in Portugal Leads 1Zahed IqbalNoch keine Bewertungen

- Engine Diesel PerfomanceDokument32 SeitenEngine Diesel PerfomancerizalNoch keine Bewertungen

- Oracle Exadata Database Machine X4-2: Features and FactsDokument17 SeitenOracle Exadata Database Machine X4-2: Features and FactsGanesh JNoch keine Bewertungen

- Exp. 5 - Terminal Characteristis and Parallel Operation of Single Phase Transformers.Dokument7 SeitenExp. 5 - Terminal Characteristis and Parallel Operation of Single Phase Transformers.AbhishEk SinghNoch keine Bewertungen

- Asphalt Plant Technical SpecificationsDokument5 SeitenAsphalt Plant Technical SpecificationsEljoy AgsamosamNoch keine Bewertungen

- Microsoft Word - Claimants Referral (Correct Dates)Dokument15 SeitenMicrosoft Word - Claimants Referral (Correct Dates)Michael FourieNoch keine Bewertungen

- TAB Procedures From An Engineering FirmDokument18 SeitenTAB Procedures From An Engineering Firmtestuser180Noch keine Bewertungen

- FIRE FIGHTING ROBOT (Mini Project)Dokument21 SeitenFIRE FIGHTING ROBOT (Mini Project)Hisham Kunjumuhammed100% (2)

- Form Three Physics Handbook-1Dokument94 SeitenForm Three Physics Handbook-1Kisaka G100% (1)

- Aitt Feb 2017 TH Sem IIIDokument6 SeitenAitt Feb 2017 TH Sem IIIMadhu KumarNoch keine Bewertungen

- Discover Mecosta 2011Dokument40 SeitenDiscover Mecosta 2011Pioneer GroupNoch keine Bewertungen

- QA/QC Checklist - Installation of MDB Panel BoardsDokument6 SeitenQA/QC Checklist - Installation of MDB Panel Boardsehtesham100% (1)

- Brand Positioning of PepsiCoDokument9 SeitenBrand Positioning of PepsiCoAbhishek DhawanNoch keine Bewertungen

- Dry Canyon Artillery RangeDokument133 SeitenDry Canyon Artillery RangeCAP History LibraryNoch keine Bewertungen

- SM Land Vs BCDADokument68 SeitenSM Land Vs BCDAelobeniaNoch keine Bewertungen

- CANELA Learning Activity - NSPE Code of EthicsDokument4 SeitenCANELA Learning Activity - NSPE Code of EthicsChristian CanelaNoch keine Bewertungen

- SAS SamplingDokument24 SeitenSAS SamplingVaibhav NataNoch keine Bewertungen

- NOP PortalDokument87 SeitenNOP PortalCarlos RicoNoch keine Bewertungen

- Web Technology PDFDokument3 SeitenWeb Technology PDFRahul Sachdeva100% (1)

- GR L-38338Dokument3 SeitenGR L-38338James PerezNoch keine Bewertungen

- 1SXP210003C0201Dokument122 Seiten1SXP210003C0201Ferenc SzabóNoch keine Bewertungen