Das könnte Ihnen auch gefallen

- Taxation PDFDokument14 SeitenTaxation PDFAimee DiazNoch keine Bewertungen

- Statement of Financial Accounting Standards No. 2: Accounting For Research and Development CostsDokument19 SeitenStatement of Financial Accounting Standards No. 2: Accounting For Research and Development CostsKath ONoch keine Bewertungen

- TRAINDokument18 SeitenTRAINAimee DiazNoch keine Bewertungen

- N - S - F D: AME Core Ollow IrectionsDokument5 SeitenN - S - F D: AME Core Ollow IrectionsMinnie PhuNoch keine Bewertungen

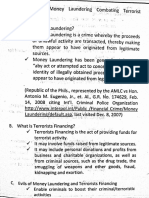

- RFBT - AMLA Notes (Picture) PDFDokument9 SeitenRFBT - AMLA Notes (Picture) PDFAimee DiazNoch keine Bewertungen

- 2017 MAS LabelDokument26 Seiten2017 MAS LabelAimeeNoch keine Bewertungen

- Basic Philippine Tax PrinciplesDokument1 SeiteBasic Philippine Tax PrinciplesAimee DiazNoch keine Bewertungen

- Guidelines On Estate and Donor's TaxDokument14 SeitenGuidelines On Estate and Donor's Taxkatreena ysabelle89% (9)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Over 140 everyday products made from petroleumDokument1 SeiteOver 140 everyday products made from petroleumDerouich2019Noch keine Bewertungen

- Grammar Unit Test - 1 RevisionDokument10 SeitenGrammar Unit Test - 1 RevisionSobithaa SivakumarNoch keine Bewertungen

- Cancer Is A Fungus ... and It Is Curable - David Icke WebsiteDokument9 SeitenCancer Is A Fungus ... and It Is Curable - David Icke WebsiteIvan100% (2)

- The Monkey and The CrocodileDokument4 SeitenThe Monkey and The Crocodile32Novita Marfid Pratiwi XI MIA 1Noch keine Bewertungen

- Delhi Travel GuideDokument14 SeitenDelhi Travel GuideoceanvastNoch keine Bewertungen

- Fao Safe at SeaDokument54 SeitenFao Safe at Seajohan darwitNoch keine Bewertungen

- Peanut Machine For Mablea Food ProducersDokument23 SeitenPeanut Machine For Mablea Food ProducersAnthonette DimayugaNoch keine Bewertungen

- Cheat Code Harvest Moon Animal ParadeDokument41 SeitenCheat Code Harvest Moon Animal ParadenischeeaNoch keine Bewertungen

- Ebook Fibre Analysis of Animal Feed GBDokument31 SeitenEbook Fibre Analysis of Animal Feed GBTatjana BrankovićNoch keine Bewertungen

- Tle 10 2ND Quarter Reviewer MaterialDokument16 SeitenTle 10 2ND Quarter Reviewer MaterialRalph Louis Rosario89% (9)

- Menu Menu Planning and BeveragesDokument11 SeitenMenu Menu Planning and Beveragesnotzi6942018890420Noch keine Bewertungen

- Powerpoint PresentationDokument3 SeitenPowerpoint PresentationMd MejbahNoch keine Bewertungen

- The 6 Most Common Fruits in the PhilippinesDokument4 SeitenThe 6 Most Common Fruits in the PhilippinesMa. Lexieni LabordoNoch keine Bewertungen

- TLE6-Agri-FisheryQ2 - (Week 6) - Modules 10 & 11Dokument35 SeitenTLE6-Agri-FisheryQ2 - (Week 6) - Modules 10 & 11Honeylet CauilanNoch keine Bewertungen

- Nutmeg and Derivatives: FO:MISC/94/7 Working PaperDokument140 SeitenNutmeg and Derivatives: FO:MISC/94/7 Working PaperBindar AdrianNoch keine Bewertungen

- Chapter IDokument16 SeitenChapter Iiyai_coolNoch keine Bewertungen

- CLOCHARD, Thessaloniki - Menu, Prices & Restaurant Reviews - TripadvisorDokument1 SeiteCLOCHARD, Thessaloniki - Menu, Prices & Restaurant Reviews - TripadvisorEdlira Zambaku MemushajNoch keine Bewertungen

- Lca InductionDokument40 SeitenLca InductionnualabradyNoch keine Bewertungen

- Fruit Beverages: Product Price ListDokument19 SeitenFruit Beverages: Product Price ListVinesh Nandikol100% (3)

- Food Chain Stage 3 Draft 1Dokument5 SeitenFood Chain Stage 3 Draft 1api-281198656Noch keine Bewertungen

- UNIT 01:ill-Gotten Gains Never Prosper: Think, Pair, Share P 52Dokument5 SeitenUNIT 01:ill-Gotten Gains Never Prosper: Think, Pair, Share P 52fadila75% (4)

- Food Fraud Mitigation GuidanceDokument36 SeitenFood Fraud Mitigation GuidanceGabriela Fdez88% (8)

- SP 1582795277Dokument7 SeitenSP 1582795277muznah kidwaiNoch keine Bewertungen

- From The Beginning of TimeDokument25 SeitenFrom The Beginning of TimeMamta100% (1)

- Wait For Me To Come Home PDFDokument831 SeitenWait For Me To Come Home PDFMik Sath100% (1)

- GRADES 1 To 12 Daily Lesson Log Monday Tuesday Wednesday Thursday FridayDokument17 SeitenGRADES 1 To 12 Daily Lesson Log Monday Tuesday Wednesday Thursday FridayMsuhJnafil RasNoch keine Bewertungen

- Ielts Fever Listening Practice Test 1 PDFDokument6 SeitenIelts Fever Listening Practice Test 1 PDFPlanet E Notes50% (2)

- Fish CrackerDokument5 SeitenFish CrackerFath Bond100% (1)

- Waterways Issue2 2015Dokument84 SeitenWaterways Issue2 2015Waterways MagazineNoch keine Bewertungen

- Classification of FoodDokument19 SeitenClassification of FoodMuhammad HannanNoch keine Bewertungen