Das könnte Ihnen auch gefallen

- Cash Flow Estimation and Risk AnalysisDokument60 SeitenCash Flow Estimation and Risk AnalysisAJ100% (2)

- 1-Capital BudgetingDokument29 Seiten1-Capital Budgetingjingyi zouNoch keine Bewertungen

- Session 06Dokument27 SeitenSession 06Jaya RoyNoch keine Bewertungen

- Session 3 Project AnalysisDokument37 SeitenSession 3 Project Analysismaud balesNoch keine Bewertungen

- FINA2010 Financial Management: Lecture 5: Capital Budgeting IIDokument54 SeitenFINA2010 Financial Management: Lecture 5: Capital Budgeting IImoonNoch keine Bewertungen

- Project Finance: Valuing Unlevered ProjectsDokument41 SeitenProject Finance: Valuing Unlevered ProjectsKelsey GaoNoch keine Bewertungen

- Capital Budgeting Cash FlowsDokument13 SeitenCapital Budgeting Cash FlowsNagaeshwary Murugan100% (1)

- MBS Corporate Finance 2023 Slide Set 3Dokument104 SeitenMBS Corporate Finance 2023 Slide Set 3PGNoch keine Bewertungen

- Chapter 5Dokument20 SeitenChapter 5Gunda AvinashNoch keine Bewertungen

- BDHCH 9Dokument37 SeitenBDHCH 9tzsyxxwht100% (1)

- 03 Cash Flows and Investment DecisionDokument24 Seiten03 Cash Flows and Investment DecisionMofdy MinaNoch keine Bewertungen

- Hongkong Capital BudgetDokument77 SeitenHongkong Capital BudgetZoloft Zithromax ProzacNoch keine Bewertungen

- Additional Aspects in Capital BudgetingDokument12 SeitenAdditional Aspects in Capital BudgetingDebashishNoch keine Bewertungen

- Basic Capital BudgetingDokument42 SeitenBasic Capital BudgetingMay Abia100% (2)

- Session 78 - Cashflows of Capital BudgetingDokument32 SeitenSession 78 - Cashflows of Capital Budgeting11219203nguyen.nhungNoch keine Bewertungen

- Chapter - 3Dokument45 SeitenChapter - 3Samia ElsayedNoch keine Bewertungen

- Cash Flow Estimation and Risk AnalysisDokument52 SeitenCash Flow Estimation and Risk AnalysisHeather Cabahug100% (1)

- Estimation of Project Cash FlowsDokument27 SeitenEstimation of Project Cash Flowsdpu_bansal83241Noch keine Bewertungen

- Capital BudgetingDokument23 SeitenCapital BudgetingchanfunyanNoch keine Bewertungen

- CB and Cash Flow (FM Keown10e Chap10Dokument70 SeitenCB and Cash Flow (FM Keown10e Chap10Hasrul HashomNoch keine Bewertungen

- Project Costs & Benefits EstimationDokument11 SeitenProject Costs & Benefits Estimationdestinyrocks88Noch keine Bewertungen

- Cap Budgeting-Cash FlowsDokument55 SeitenCap Budgeting-Cash FlowsthinkestanNoch keine Bewertungen

- Lecture 3Dokument52 SeitenLecture 3Liyazhi LiuNoch keine Bewertungen

- Capital BudgetingDokument6 SeitenCapital BudgetingJaylin DizonNoch keine Bewertungen

- Chapter - 4, CF Free Cash Flow CU (Ismat)Dokument27 SeitenChapter - 4, CF Free Cash Flow CU (Ismat)Anik ChakmaNoch keine Bewertungen

- BU7300 - Corporate Finance Capital Budgeting Week 1Dokument21 SeitenBU7300 - Corporate Finance Capital Budgeting Week 1Moony TamimiNoch keine Bewertungen

- Finc361 - Lecture - 11 - Capital Budgeting PDFDokument57 SeitenFinc361 - Lecture - 11 - Capital Budgeting PDFLondonFencer2012Noch keine Bewertungen

- Cost Estimation: (CHAPTER-3)Dokument43 SeitenCost Estimation: (CHAPTER-3)fentaw melkieNoch keine Bewertungen

- Ins3007 S4 SVDokument32 SeitenIns3007 S4 SVnguyễnthùy dươngNoch keine Bewertungen

- Business Valuation Model for New Product Launch NPV AnalysisDokument18 SeitenBusiness Valuation Model for New Product Launch NPV AnalysisAninda DuttaNoch keine Bewertungen

- Engineering Economics: Overview and Application in Process Engineering IndustryDokument13 SeitenEngineering Economics: Overview and Application in Process Engineering Industrynickhardy_ajNoch keine Bewertungen

- Making Investment Decisions With The Net Present Value RuleDokument60 SeitenMaking Investment Decisions With The Net Present Value Rulecynthiaaa sNoch keine Bewertungen

- Chapter 6: Making Capital Investment Decisions: Corporate FinanceDokument36 SeitenChapter 6: Making Capital Investment Decisions: Corporate FinanceAsif Abdullah KhanNoch keine Bewertungen

- CASH FLOW ESTIMATION Week 6Dokument30 SeitenCASH FLOW ESTIMATION Week 6adulmi325Noch keine Bewertungen

- 04 - Capital Budgeting Cash FlowDokument19 Seiten04 - Capital Budgeting Cash FlowRodrigo RamosNoch keine Bewertungen

- CHAPTER 2 (A) - Analyzing Project Cash FlowsDokument70 SeitenCHAPTER 2 (A) - Analyzing Project Cash FlowsSarnisha Murugeshwaran (Shazzisha)Noch keine Bewertungen

- Making Capital Investment Decisions: Mcgraw-Hill/IrwinDokument23 SeitenMaking Capital Investment Decisions: Mcgraw-Hill/IrwinMSA-ACCA100% (2)

- Session 10 Chapter 10 Making Capital InvestmentDecisionDokument35 SeitenSession 10 Chapter 10 Making Capital InvestmentDecisionLili YaniNoch keine Bewertungen

- Advance Corporate Finance NotesDokument108 SeitenAdvance Corporate Finance Notesellenzh.0206Noch keine Bewertungen

- F9FM-Session05 d08jkbnDokument30 SeitenF9FM-Session05 d08jkbnErclanNoch keine Bewertungen

- S7-Capital BudgetingDokument78 SeitenS7-Capital BudgetingShaheer BaigNoch keine Bewertungen

- Chapter 7 Capital Budgeting and Cashflow (Autosaved)Dokument53 SeitenChapter 7 Capital Budgeting and Cashflow (Autosaved)Kim ThoaNoch keine Bewertungen

- Investment Decision MethodDokument44 SeitenInvestment Decision MethodashwathNoch keine Bewertungen

- Fonderia Di Torino SDokument15 SeitenFonderia Di Torino SYrnob RokieNoch keine Bewertungen

- Capital BudgetingDokument45 SeitenCapital BudgetingdawncpainNoch keine Bewertungen

- Capital Budgeting - SOCDokument29 SeitenCapital Budgeting - SOCVEDANT SAININoch keine Bewertungen

- Capital Budteting JainDokument56 SeitenCapital Budteting JainShivam VermaNoch keine Bewertungen

- Project Feasibility & Finance PrinciplesDokument27 SeitenProject Feasibility & Finance PrinciplesHimanshu DuttaNoch keine Bewertungen

- International Capital Budgeting DecisionsDokument32 SeitenInternational Capital Budgeting DecisionsVenance NDALICHAKONoch keine Bewertungen

- Cash Flow & TaxesDokument11 SeitenCash Flow & TaxesPartha ChakaravartiNoch keine Bewertungen

- Finance NotesDokument14 SeitenFinance NotesVARUN MONGANoch keine Bewertungen

- Chapter 8 Corporate FinanceDokument34 SeitenChapter 8 Corporate FinancediaNoch keine Bewertungen

- Capital Budgeting Part IDokument53 SeitenCapital Budgeting Part IIris BalucanNoch keine Bewertungen

- Incremental AnalysisDokument25 SeitenIncremental AnalysisAngel MallariNoch keine Bewertungen

- Capital Budgeting - Part 1Dokument6 SeitenCapital Budgeting - Part 1Aurelia RijiNoch keine Bewertungen

- Read The Following Case Situation Carefully and Answer The Questions That FollowDokument7 SeitenRead The Following Case Situation Carefully and Answer The Questions That FollowBhuwan PandeyNoch keine Bewertungen

- The Basics of Capital BudgetingDokument56 SeitenThe Basics of Capital BudgetingRanin, Manilac Melissa SNoch keine Bewertungen

- EBF 2054 Capital BudgetingDokument48 SeitenEBF 2054 Capital BudgetingizzatiNoch keine Bewertungen

- Applied Corporate Finance. What is a Company worth?Von EverandApplied Corporate Finance. What is a Company worth?Bewertung: 3 von 5 Sternen3/5 (2)

- The Entrepreneur’S Dictionary of Business and Financial TermsVon EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNoch keine Bewertungen

- Harvard Referencing PDFDokument4 SeitenHarvard Referencing PDFAhmad Nur ArifNoch keine Bewertungen

- Ebs429 Assignment1Dokument1 SeiteEbs429 Assignment1NNadiah IsaNoch keine Bewertungen

- Cement PlantDokument232 SeitenCement PlantAnonymous iI88Lt100% (1)

- Materials 11 00011 PDFDokument17 SeitenMaterials 11 00011 PDFNNadiah IsaNoch keine Bewertungen

- Receiving 2019 PDFDokument1 SeiteReceiving 2019 PDFNNadiah IsaNoch keine Bewertungen

- Cement PlantDokument232 SeitenCement PlantAnonymous iI88Lt100% (1)

- PP1 Term Mini ProjectDokument15 SeitenPP1 Term Mini ProjectNNadiah IsaNoch keine Bewertungen

- Anomaly Map For Au: Upper PartDokument1 SeiteAnomaly Map For Au: Upper PartNNadiah IsaNoch keine Bewertungen

- Parts and Functions of Conveyor SystemsDokument30 SeitenParts and Functions of Conveyor SystemsArsh BhandariNoch keine Bewertungen

- EBS 341-Lab Briefing-19 Feb 2019Dokument71 SeitenEBS 341-Lab Briefing-19 Feb 2019NNadiah Isa100% (1)

- 2017 2018 Eup 222 Sem 1 Project Finance Topic Outcome 1Dokument32 Seiten2017 2018 Eup 222 Sem 1 Project Finance Topic Outcome 1NNadiah IsaNoch keine Bewertungen

- (Iii) For Load 30kgDokument7 Seiten(Iii) For Load 30kgNNadiah IsaNoch keine Bewertungen

- 2a CHP1-4 (E) (Material Properties)Dokument34 Seiten2a CHP1-4 (E) (Material Properties)NNadiah IsaNoch keine Bewertungen

- 2017 2018 Eup 222 Sem 1 Project Finance Topic Outcome 1Dokument32 Seiten2017 2018 Eup 222 Sem 1 Project Finance Topic Outcome 1NNadiah IsaNoch keine Bewertungen

- Definition of PiDokument9 SeitenDefinition of PiNNadiah IsaNoch keine Bewertungen

- Composite MaterialsDokument29 SeitenComposite MaterialsNNadiah Isa100% (1)

- Definition of PiDokument9 SeitenDefinition of PiNNadiah IsaNoch keine Bewertungen

- Hydroelectric Assembly GuideDokument12 SeitenHydroelectric Assembly GuideNNadiah IsaNoch keine Bewertungen

- Questions FinanceDokument3 SeitenQuestions Financeanish narayanNoch keine Bewertungen

- ABMFABM2 q2 Mod1 Bank-Reconciliation-StatementDokument29 SeitenABMFABM2 q2 Mod1 Bank-Reconciliation-StatementRachel Sao-a100% (1)

- Basic Accounting TermsDokument17 SeitenBasic Accounting TermsNEONTechNoch keine Bewertungen

- Roc Forms & Secretarial PracticeDokument22 SeitenRoc Forms & Secretarial PracticesriinairNoch keine Bewertungen

- IntAcc1 - Midterm Examination - 1st Sem 2019 2020 PDFDokument9 SeitenIntAcc1 - Midterm Examination - 1st Sem 2019 2020 PDFAndrea Nicole BanzonNoch keine Bewertungen

- IFRS 16 - SummaryDokument4 SeitenIFRS 16 - SummaryJean LeongNoch keine Bewertungen

- Accounting Equation and Profit DeterminationDokument19 SeitenAccounting Equation and Profit DeterminationNor LailyNoch keine Bewertungen

- CapstruDokument28 SeitenCapstruRiyan RismayanaNoch keine Bewertungen

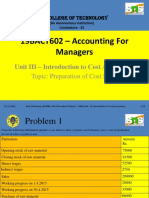

- 19BACT602 - Accounting For Managers: Unit III - Introduction To Cost AccountingDokument12 Seiten19BACT602 - Accounting For Managers: Unit III - Introduction To Cost AccountingReetaNoch keine Bewertungen

- Cost of The Project: M/S Sarala Fly Ash BricksDokument6 SeitenCost of The Project: M/S Sarala Fly Ash BricksGOUTAM GOSWAMINoch keine Bewertungen

- Kanisa Savings and Credit Co-Operative Society LTD.: Fy2017 Annual Report and Financial Statements 24TH MARCH 2018Dokument56 SeitenKanisa Savings and Credit Co-Operative Society LTD.: Fy2017 Annual Report and Financial Statements 24TH MARCH 2018Louis KakindaNoch keine Bewertungen

- Britannia Annual Report 2016-17 PDFDokument232 SeitenBritannia Annual Report 2016-17 PDFAditya ramaiahNoch keine Bewertungen

- Percentage Taxes: Line of Business/ Activity Tax Base Tax RateDokument2 SeitenPercentage Taxes: Line of Business/ Activity Tax Base Tax RateMae MaupoNoch keine Bewertungen

- Introduction and Overview of IBCDokument3 SeitenIntroduction and Overview of IBCArushi JindalNoch keine Bewertungen

- Intermediate Accounting Millan Solution Manual PDFDokument3 SeitenIntermediate Accounting Millan Solution Manual PDFRoldan Hiano Manganip13% (8)

- FINAL-Investment in AssociateDokument16 SeitenFINAL-Investment in AssociateJessa75% (4)

- Financial Measures: (Amazon, 2021)Dokument6 SeitenFinancial Measures: (Amazon, 2021)najeeb shajudheenNoch keine Bewertungen

- Business Finance ConceptDokument55 SeitenBusiness Finance ConceptBir MallaNoch keine Bewertungen

- Govt College Teaching Plans for Financial, Management SubjectsDokument4 SeitenGovt College Teaching Plans for Financial, Management SubjectsGFGC BCANoch keine Bewertungen

- Investment options analysis in IndiaDokument54 SeitenInvestment options analysis in IndiaSagrika SagarNoch keine Bewertungen

- The Manufacturers Life Insurance Co., Plaintiff-Internal Revenue, Defendant-AppelleeDokument6 SeitenThe Manufacturers Life Insurance Co., Plaintiff-Internal Revenue, Defendant-AppelleeJade ClementeNoch keine Bewertungen

- Eacc1614 Test 2 Memo 2021 AdjDokument10 SeitenEacc1614 Test 2 Memo 2021 AdjshabanguntandoyenkosiNoch keine Bewertungen

- Exercises Chapter 11Dokument3 SeitenExercises Chapter 11Fatima BeenaNoch keine Bewertungen

- Motilal Oswal Securities Ltd. Summer Internship ReportDokument104 SeitenMotilal Oswal Securities Ltd. Summer Internship ReportSathavara Ketul100% (2)

- SME Loan KYC Supplemental FormDokument2 SeitenSME Loan KYC Supplemental FormPagalan LorjunNoch keine Bewertungen

- AFT 2073 Financial Management: Group Tutorial: L1 Lect Name: Sir Ahmad Ridhuwan Bin Abdullah Group MemberDokument25 SeitenAFT 2073 Financial Management: Group Tutorial: L1 Lect Name: Sir Ahmad Ridhuwan Bin Abdullah Group MemberwawanNoch keine Bewertungen

- Ashok Leyland Valuation - ReportDokument17 SeitenAshok Leyland Valuation - Reportbharath_ndNoch keine Bewertungen

- Question Paper 11 Accounts Time: 3Hrs Max Marks: 80Dokument5 SeitenQuestion Paper 11 Accounts Time: 3Hrs Max Marks: 80manish jangidNoch keine Bewertungen

- Exercise SolutionsDokument114 SeitenExercise SolutionsCarolyn ImaniNoch keine Bewertungen

- Residency StatusDokument13 SeitenResidency StatusPhương NguyễnNoch keine Bewertungen