Das könnte Ihnen auch gefallen

- Small Finance Banks: New Category of Differentiated Banks: PerspectivesDokument8 SeitenSmall Finance Banks: New Category of Differentiated Banks: PerspectivesUnitti ChauhanNoch keine Bewertungen

- A Report OnDokument26 SeitenA Report OnNihar HindochaNoch keine Bewertungen

- BK Swain DocumentDokument11 SeitenBK Swain DocumentSatyashil RangareNoch keine Bewertungen

- Role and Future of Small Finance BankDokument36 SeitenRole and Future of Small Finance BankVicky BangdeNoch keine Bewertungen

- Smfgu271114 PDFDokument10 SeitenSmfgu271114 PDFHarsh JainNoch keine Bewertungen

- About Corporation Bank IndiaDokument4 SeitenAbout Corporation Bank IndiaPriyanka SawantNoch keine Bewertungen

- Comparitive Analysis of Public Sector and Private Sectors Banks PDFDokument67 SeitenComparitive Analysis of Public Sector and Private Sectors Banks PDFAnonymous y3E7ia100% (1)

- Reserve Bank of India Draft Guidelines For Licensing of "Small Banks" in The Private Sector July 17, 2014 I. PreambleDokument6 SeitenReserve Bank of India Draft Guidelines For Licensing of "Small Banks" in The Private Sector July 17, 2014 I. PreamblejagadeeshNoch keine Bewertungen

- Small Finance Bank and Financial Inclusion - A Case Study of Ujjivan Small Finance BankDokument10 SeitenSmall Finance Bank and Financial Inclusion - A Case Study of Ujjivan Small Finance BankNavneet LohchabNoch keine Bewertungen

- BFSI Sector in IndiaDokument3 SeitenBFSI Sector in IndiaKenneth GallowayNoch keine Bewertungen

- A Study On The Merger AND Acquisition of HDFC Bank and Equitas Small Finance BankDokument23 SeitenA Study On The Merger AND Acquisition of HDFC Bank and Equitas Small Finance BankashilNoch keine Bewertungen

- A Study On Credit Risk ManagementDokument44 SeitenA Study On Credit Risk ManagementShabreen Sultana100% (1)

- Corporation Bank Report FinalDokument61 SeitenCorporation Bank Report FinalJasmandeep brarNoch keine Bewertungen

- Banking Law Reserach PaperDokument23 SeitenBanking Law Reserach Papersarayu alluNoch keine Bewertungen

- Universal Banks in IndiaDokument33 SeitenUniversal Banks in Indianamita patharkarNoch keine Bewertungen

- 0 - A Study On Competency Mapping in Ujjivan Small Finance BankDokument8 Seiten0 - A Study On Competency Mapping in Ujjivan Small Finance BankPRANUNoch keine Bewertungen

- Preface: of Public Sector and Private Sector Banks"Dokument47 SeitenPreface: of Public Sector and Private Sector Banks"madhuri100% (1)

- ICICI Go Global Case PDFDokument15 SeitenICICI Go Global Case PDFSAGAR BALAGARNoch keine Bewertungen

- Credit Appraisal SystemDokument58 SeitenCredit Appraisal Systemsatapathy_smruti12100% (10)

- Economy Banking System in IndiaDokument21 SeitenEconomy Banking System in Indiakrishan palNoch keine Bewertungen

- Executive Summary: NPA Management in State Bank of IndiaDokument62 SeitenExecutive Summary: NPA Management in State Bank of IndiaFurkhan Ahmed SamNoch keine Bewertungen

- Study On Loans and AdvancesDokument58 SeitenStudy On Loans and AdvancesUday Gowda100% (1)

- Mrunal Banking: RRB Amendment Bill, Small Banks-Payment BanksDokument10 SeitenMrunal Banking: RRB Amendment Bill, Small Banks-Payment BanksPrateek BayalNoch keine Bewertungen

- Credit Appraisal SystemDokument54 SeitenCredit Appraisal SystemÂShu KaLràNoch keine Bewertungen

- Structure of Banking System in IndiaDokument34 SeitenStructure of Banking System in IndiaAyushi SinghNoch keine Bewertungen

- Evolution of The Indian Banking IndustryDokument6 SeitenEvolution of The Indian Banking IndustryNeha ChandnaNoch keine Bewertungen

- Evolution of The Indian Banking IndustryDokument7 SeitenEvolution of The Indian Banking IndustryfasahmadNoch keine Bewertungen

- BankDokument9 SeitenBankakashgulati007Noch keine Bewertungen

- Indian Banking IndustryDokument12 SeitenIndian Banking Industrysimranarora2007Noch keine Bewertungen

- Non-Banking Financial InstitutionsDokument4 SeitenNon-Banking Financial Institutionscool_vardahNoch keine Bewertungen

- CITIBANKDokument28 SeitenCITIBANKAnirudh SinghNoch keine Bewertungen

- Winter Project On Banking: Idbi BankDokument18 SeitenWinter Project On Banking: Idbi BankMudit JiNoch keine Bewertungen

- Non-Performing Assets: Status & Impact A Comparative Study of Public & Private Sector BanksDokument15 SeitenNon-Performing Assets: Status & Impact A Comparative Study of Public & Private Sector Bankszakir hussainNoch keine Bewertungen

- Role of Co-Operative Banks: My ResearchDokument4 SeitenRole of Co-Operative Banks: My Researchsimran yadavNoch keine Bewertungen

- Comparative Study On Seavices of Public Sector and Private Sector Banks OptDokument49 SeitenComparative Study On Seavices of Public Sector and Private Sector Banks OptWashik Malik100% (1)

- Economics ProjectDokument15 SeitenEconomics ProjectAniket taywadeNoch keine Bewertungen

- BankingDokument8 SeitenBankingDivya NathNoch keine Bewertungen

- A Study 0f Financial PerformanceDokument84 SeitenA Study 0f Financial Performanceseema mundaleNoch keine Bewertungen

- Uco Introduction N HistoryDokument18 SeitenUco Introduction N HistorySumit PoddarNoch keine Bewertungen

- BASIC Bank Limited: Serving People For ProgressDokument15 SeitenBASIC Bank Limited: Serving People For ProgressMD Shariful IslamNoch keine Bewertungen

- Introduction of Banking SystemDokument10 SeitenIntroduction of Banking SystemMasy1210% (1)

- A Study of Credit Assessment in Dena BankDokument48 SeitenA Study of Credit Assessment in Dena BankDeepali MahilagiriNoch keine Bewertungen

- Impact of Recent Mergers in Public Sector BanksDokument18 SeitenImpact of Recent Mergers in Public Sector BanksAnkita Das100% (3)

- Synopsis ON Credit Risk Management IN: Pooja Arora 140423533Dokument6 SeitenSynopsis ON Credit Risk Management IN: Pooja Arora 140423533Pooja AroraNoch keine Bewertungen

- Project On Icici 123Dokument28 SeitenProject On Icici 123hazaribag vigilanceNoch keine Bewertungen

- Types of BankingDokument10 SeitenTypes of BankingJinu SajiNoch keine Bewertungen

- Thesis On Cooperative BanksDokument8 SeitenThesis On Cooperative Bankscristinafranklinnewark100% (2)

- Co Operative BankDokument7 SeitenCo Operative Bankவிதை SOUNDAR CholaNoch keine Bewertungen

- Project Report 1Dokument57 SeitenProject Report 1john_muellor63% (8)

- Rural DevelopmentsDokument88 SeitenRural DevelopmentsVyom K ShahNoch keine Bewertungen

- Project - Loans and AdvancesDokument60 SeitenProject - Loans and AdvancesRajendra Gawate75% (12)

- Functions: Commercial BankDokument12 SeitenFunctions: Commercial BanksupriyakharadeNoch keine Bewertungen

- BANKING AWAREESS: Different Types of Bank: 1. Commercial BanksDokument12 SeitenBANKING AWAREESS: Different Types of Bank: 1. Commercial BanksKumar KushNoch keine Bewertungen

- Report On Home Loan Schemes Provided by HDFC Vs Icici BankDokument73 SeitenReport On Home Loan Schemes Provided by HDFC Vs Icici BankAakriti Chauhan100% (1)

- Banking India: Accepting Deposits for the Purpose of LendingVon EverandBanking India: Accepting Deposits for the Purpose of LendingNoch keine Bewertungen

- Regional Rural Banks of India: Evolution, Performance and ManagementVon EverandRegional Rural Banks of India: Evolution, Performance and ManagementNoch keine Bewertungen

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Von EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Noch keine Bewertungen

- Major Bank Fraud Cases: A Critical ReviewVon EverandMajor Bank Fraud Cases: A Critical ReviewBewertung: 4.5 von 5 Sternen4.5/5 (6)

- Islamic Banking And Finance for Beginners!Von EverandIslamic Banking And Finance for Beginners!Bewertung: 2 von 5 Sternen2/5 (1)

- Marketing of Consumer Financial Products: Insights From Service MarketingVon EverandMarketing of Consumer Financial Products: Insights From Service MarketingNoch keine Bewertungen

- MNC Term Paper - Group 8Dokument15 SeitenMNC Term Paper - Group 8Pranav KaushalNoch keine Bewertungen

- NABARD Macro CreditDokument12 SeitenNABARD Macro CreditPranav KaushalNoch keine Bewertungen

- Indivisual Assignment - Small Finance BanksDokument12 SeitenIndivisual Assignment - Small Finance BanksPranav KaushalNoch keine Bewertungen

- Group Assignment - Group 4Dokument24 SeitenGroup Assignment - Group 4Pranav Kaushal100% (1)

- Editing CodingDokument20 SeitenEditing CodingPranav KaushalNoch keine Bewertungen

- Paper 90Dokument14 SeitenPaper 90Pranav KaushalNoch keine Bewertungen

- Sovereign Credit Default Swaps and The MacroeconomyDokument11 SeitenSovereign Credit Default Swaps and The MacroeconomyPranav KaushalNoch keine Bewertungen

- Session 3Dokument10 SeitenSession 3Pranav KaushalNoch keine Bewertungen

- Fish! A Re Markable Way T o Boos T Morale and I Mprove Re S Ult SDokument38 SeitenFish! A Re Markable Way T o Boos T Morale and I Mprove Re S Ult SHieu VuNoch keine Bewertungen

- Internationalization of Emerging Indian MultinationalsDokument9 SeitenInternationalization of Emerging Indian MultinationalsPranav KaushalNoch keine Bewertungen

- Suprcapacitors Enable Energy Harvesters To Power IoTDokument5 SeitenSuprcapacitors Enable Energy Harvesters To Power IoTPranav KaushalNoch keine Bewertungen

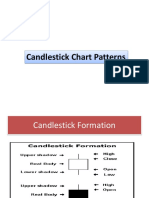

- Candlestick Chart PatternsDokument20 SeitenCandlestick Chart PatternsPranav Kaushal100% (2)

- Part One: Overture and Pageantry: TenderlyDokument3 SeitenPart One: Overture and Pageantry: TenderlyEneas Augusto100% (1)

- Tally MCQ 1Dokument11 SeitenTally MCQ 1rs0100100% (4)

- Business Plan On HIRING A MAIDDokument21 SeitenBusiness Plan On HIRING A MAIDharsha100% (1)

- PGEresponseDokument37 SeitenPGEresponseABC10Noch keine Bewertungen

- Recruitment, Selection, Induction, Training and Development ProcessDokument4 SeitenRecruitment, Selection, Induction, Training and Development ProcessMayurRawoolNoch keine Bewertungen

- Configuring and Managing JDBC Data Sources For Oracle WebLogic Server 11.1Dokument148 SeitenConfiguring and Managing JDBC Data Sources For Oracle WebLogic Server 11.1mdalaminNoch keine Bewertungen

- Mandy Craven: Career ObjectiveDokument2 SeitenMandy Craven: Career ObjectiveMandy CravenNoch keine Bewertungen

- FAR-Midterm ExamDokument19 SeitenFAR-Midterm ExamTxos Vaj100% (1)

- Salary Slip & Transfer Confirmation: Date: Period: Bank: Account # Name: Title: Dept: Emp #Dokument2 SeitenSalary Slip & Transfer Confirmation: Date: Period: Bank: Account # Name: Title: Dept: Emp #Adheesh SanthoshNoch keine Bewertungen

- Defining Social InnovationDokument15 SeitenDefining Social InnovationFasyaAfifNoch keine Bewertungen

- TOA Reviewer (UE) - Bank Reconcilation PDFDokument1 SeiteTOA Reviewer (UE) - Bank Reconcilation PDFjhallylipmaNoch keine Bewertungen

- TRDokument18 SeitenTRharshal49Noch keine Bewertungen

- Ibs Bukit Pasir, BP 1 31/03/22Dokument5 SeitenIbs Bukit Pasir, BP 1 31/03/22Design ZeroNoch keine Bewertungen

- Online Shopping and Its ImpactDokument33 SeitenOnline Shopping and Its ImpactAkhil MohananNoch keine Bewertungen

- DO Section 5-6Dokument46 SeitenDO Section 5-6Gianita SimatupangNoch keine Bewertungen

- Examples Transfer PricingDokument15 SeitenExamples Transfer PricingRajat RathNoch keine Bewertungen

- 10 Steps To Precision Maintenance Reliability SuccessDokument11 Seiten10 Steps To Precision Maintenance Reliability SuccessElvis DiazNoch keine Bewertungen

- 4b18 PDFDokument5 Seiten4b18 PDFAnonymous lN5DHnehwNoch keine Bewertungen

- Saji DDDD DDDDDokument37 SeitenSaji DDDD DDDDTalha Iftekhar Khan SwatiNoch keine Bewertungen

- Macro 03Dokument381 SeitenMacro 03subroto36100% (1)

- ICI Vol 43 29-11-16Dokument32 SeitenICI Vol 43 29-11-16PIG MITCONNoch keine Bewertungen

- MNM3702 Full Notes - Stuvia PDFDokument57 SeitenMNM3702 Full Notes - Stuvia PDFMichaelNoch keine Bewertungen

- Classical Approach To Analyse Consumer BehaviourDokument12 SeitenClassical Approach To Analyse Consumer BehaviourKerty Herwyn GuerelNoch keine Bewertungen

- Sky Roofing - PresentationDokument10 SeitenSky Roofing - PresentationViswanathan RamasamyNoch keine Bewertungen

- Civil Code of The Philippines Common CarriersDokument4 SeitenCivil Code of The Philippines Common CarriersKathrynne NepomucenoNoch keine Bewertungen

- Marketing IndividualDokument2 SeitenMarketing Individualsinyi0Noch keine Bewertungen

- Business Viability CalculatorDokument3 SeitenBusiness Viability CalculatorKiyo AiNoch keine Bewertungen

- Bpo Management SystemDokument12 SeitenBpo Management SystembaskarbalachandranNoch keine Bewertungen

- GST Proposal Presentation 1Dokument47 SeitenGST Proposal Presentation 1pmenocha879986% (7)

- Export MerchandisingDokument18 SeitenExport MerchandisingNeha Suman100% (1)