Das könnte Ihnen auch gefallen

- Power Markets and Economics: Energy Costs, Trading, EmissionsVon EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNoch keine Bewertungen

- Metro Pacific Inv. Corp: Providing Clarity On The Negative News FlowsDokument2 SeitenMetro Pacific Inv. Corp: Providing Clarity On The Negative News FlowsJNoch keine Bewertungen

- 2016 06 03 PH S Mpi PDFDokument4 Seiten2016 06 03 PH S Mpi PDFJNoch keine Bewertungen

- No Quick Turnaround Seen For The San Gabriel: First Gen CorporationDokument2 SeitenNo Quick Turnaround Seen For The San Gabriel: First Gen CorporationJohn Kyle LluzNoch keine Bewertungen

- 2010 09 30 PH S DMCDokument3 Seiten2010 09 30 PH S DMCaaronsayNoch keine Bewertungen

- Raising Estimates On Higher Earnings Contribution From Power BusinessDokument4 SeitenRaising Estimates On Higher Earnings Contribution From Power BusinessJNoch keine Bewertungen

- Mpi Files For Php83Bil Ipo of Hospital Group, Adding Mpi To Coling The Shots Stock PicksDokument5 SeitenMpi Files For Php83Bil Ipo of Hospital Group, Adding Mpi To Coling The Shots Stock PicksJNoch keine Bewertungen

- 2018 04 26 PH S Mpi PDFDokument6 Seiten2018 04 26 PH S Mpi PDFJNoch keine Bewertungen

- 2020 10 19 PH S Tel PDFDokument7 Seiten2020 10 19 PH S Tel PDFJNoch keine Bewertungen

- CHP Col ResearchDokument10 SeitenCHP Col ResearchJun GomezNoch keine Bewertungen

- 9M16 Earnings Beat Estimates As Coal Mining Outperforms: Share DataDokument4 Seiten9M16 Earnings Beat Estimates As Coal Mining Outperforms: Share DataJajahinaNoch keine Bewertungen

- Toll Road Demand Weakened in April With Shift To ECQ, Power Demand Remained FirmDokument5 SeitenToll Road Demand Weakened in April With Shift To ECQ, Power Demand Remained FirmJajahinaNoch keine Bewertungen

- Kogas Ar 2020Dokument11 SeitenKogas Ar 2020Vinaya NaralasettyNoch keine Bewertungen

- 1Q21 Core Operating Performance Beats Estimates: International Container Terminal Services IncDokument8 Seiten1Q21 Core Operating Performance Beats Estimates: International Container Terminal Services IncJajahinaNoch keine Bewertungen

- Note For Investment Operation CommitteeDokument4 SeitenNote For Investment Operation CommitteeAyushi somaniNoch keine Bewertungen

- Increasing Estimates On Improving Earnings Outlook: First Gen CorporationDokument7 SeitenIncreasing Estimates On Improving Earnings Outlook: First Gen Corporationskynyrd75Noch keine Bewertungen

- Aboitiz Equity Ventures: Emerging Powerhouse: Field NotesDokument4 SeitenAboitiz Equity Ventures: Emerging Powerhouse: Field NotesJNoch keine Bewertungen

- MD & Ceo CFO CRO CIO: Note For Investment Operation CommitteeDokument4 SeitenMD & Ceo CFO CRO CIO: Note For Investment Operation CommitteeAyushi somaniNoch keine Bewertungen

- ACEN Expands Domestic Solar Power Generation Capacity: AC Energy Philippines, IncDokument5 SeitenACEN Expands Domestic Solar Power Generation Capacity: AC Energy Philippines, IncJajahinaNoch keine Bewertungen

- 1Q21 Net Income Above Expectation: Semirara Mining CorporationDokument8 Seiten1Q21 Net Income Above Expectation: Semirara Mining CorporationJajahinaNoch keine Bewertungen

- 1Q21 Core Earnings Lag Forecasts: Metro Pacific Investments CorporationDokument8 Seiten1Q21 Core Earnings Lag Forecasts: Metro Pacific Investments CorporationJajahinaNoch keine Bewertungen

- 2019 10 14 PH S Phen PDFDokument4 Seiten2019 10 14 PH S Phen PDFJNoch keine Bewertungen

- Havells India Ltd. - INDSECDokument12 SeitenHavells India Ltd. - INDSECResearch ReportsNoch keine Bewertungen

- 9M21 Net Income Exceed Estimates: Semirara Mining CorporationDokument8 Seiten9M21 Net Income Exceed Estimates: Semirara Mining CorporationJajahinaNoch keine Bewertungen

- Q1FY23 - Result Update: Future Growth IntactDokument10 SeitenQ1FY23 - Result Update: Future Growth IntactResearch ReportsNoch keine Bewertungen

- 9M21 Core Earnings Beat Forecast As Earnings On The Strength of The Power Generation BusinessDokument7 Seiten9M21 Core Earnings Beat Forecast As Earnings On The Strength of The Power Generation BusinessJajahinaNoch keine Bewertungen

- Profits Pulled Down by COVID-19 Pandemic: Cosco Capital, IncDokument7 SeitenProfits Pulled Down by COVID-19 Pandemic: Cosco Capital, Incacd1355Noch keine Bewertungen

- Elecon Engineering Limited - in Line With Our EstimatesDokument4 SeitenElecon Engineering Limited - in Line With Our EstimatesruchikdoshiNoch keine Bewertungen

- Earnings Analysis - PXDokument7 SeitenEarnings Analysis - PXgwapongkabayoNoch keine Bewertungen

- Ambuja Cements: NeutralDokument8 SeitenAmbuja Cements: Neutral张迪Noch keine Bewertungen

- 2014 02 06 PH S Mpi PDFDokument4 Seiten2014 02 06 PH S Mpi PDFJNoch keine Bewertungen

- Metro Pacific Inv. Corp: A No Surprise Quarter: Earnings AnalysisDokument3 SeitenMetro Pacific Inv. Corp: A No Surprise Quarter: Earnings AnalysisJNoch keine Bewertungen

- 1Q20 Core Earnings in Line With Forecast: Metro Pacific Investments CorporationDokument8 Seiten1Q20 Core Earnings in Line With Forecast: Metro Pacific Investments CorporationJNoch keine Bewertungen

- PGOLD Sees A Slower Performance in 2H20: Puregold Price Club, IncDokument7 SeitenPGOLD Sees A Slower Performance in 2H20: Puregold Price Club, IncJNoch keine Bewertungen

- 2020 09 21 PH S SCC PDFDokument7 Seiten2020 09 21 PH S SCC PDFElcano MirandaNoch keine Bewertungen

- 3Q17 Earning Eng FinalDokument18 Seiten3Q17 Earning Eng FinalarakeelNoch keine Bewertungen

- 2023 07 27 PH e PgoldDokument6 Seiten2023 07 27 PH e PgoldexcA1996Noch keine Bewertungen

- SharekhanTopPicks 041210Dokument7 SeitenSharekhanTopPicks 041210mathaiyan,arunNoch keine Bewertungen

- Profit Lags As Chengdu Revenue Recognition Delayed, Mall Recovery StallsDokument8 SeitenProfit Lags As Chengdu Revenue Recognition Delayed, Mall Recovery StallsJajahinaNoch keine Bewertungen

- Foodothe 20090319Dokument12 SeitenFoodothe 20090319nareshsbcNoch keine Bewertungen

- 1Q21 Operating EBITDA Below COL Estimates On Lower-Than-Expected RevenuesDokument8 Seiten1Q21 Operating EBITDA Below COL Estimates On Lower-Than-Expected RevenuesJajahinaNoch keine Bewertungen

- Mahindra & Mahindra: CMP: INR672 TP: INR810 (+20%)Dokument14 SeitenMahindra & Mahindra: CMP: INR672 TP: INR810 (+20%)Yash DoshiNoch keine Bewertungen

- Bhel-3qfy11 Ru-210111Dokument12 SeitenBhel-3qfy11 Ru-210111kshintlNoch keine Bewertungen

- Korea Gas Corporation: Results of Fiscal Year 2019Dokument10 SeitenKorea Gas Corporation: Results of Fiscal Year 2019Vinaya NaralasettyNoch keine Bewertungen

- 1Q21 Core Income Up 9.1% Y/y On Higher Data-Related Revenues, in Line With EstimatesDokument8 Seiten1Q21 Core Income Up 9.1% Y/y On Higher Data-Related Revenues, in Line With EstimatesJajahinaNoch keine Bewertungen

- Breaking Events: Building MaterialsDokument5 SeitenBreaking Events: Building Materialsapi-26443191Noch keine Bewertungen

- LKP Moldtek 01feb08Dokument2 SeitenLKP Moldtek 01feb08nillchopraNoch keine Bewertungen

- HSL - Commodities Pack Report - 2021-202108182348310059173Dokument16 SeitenHSL - Commodities Pack Report - 2021-202108182348310059173SHAIK AHMEDNoch keine Bewertungen

- Nickel StudyDokument7 SeitenNickel StudyILSEN N. DAETNoch keine Bewertungen

- 2011 10 18 PH S Mpi PDFDokument4 Seiten2011 10 18 PH S Mpi PDFJNoch keine Bewertungen

- Balance Sheet Strong Enough To Handle The Worst: Bloomberry Resorts CorporationDokument7 SeitenBalance Sheet Strong Enough To Handle The Worst: Bloomberry Resorts CorporationJajahinaNoch keine Bewertungen

- Airtel AnalysisDokument15 SeitenAirtel AnalysisPriyanshi JainNoch keine Bewertungen

- 2022 12 21 PH S TelDokument7 Seiten2022 12 21 PH S TelIouNoch keine Bewertungen

- Mahindra & Mahindra: 3 August 2009Dokument8 SeitenMahindra & Mahindra: 3 August 2009Chandni OzaNoch keine Bewertungen

- Singapore Exchange Limited: Firing On All CylindersDokument6 SeitenSingapore Exchange Limited: Firing On All CylindersCalebNoch keine Bewertungen

- Wipro: CMP: INR243 TP: INR260 (+7%) Largely in Line Lower ETR Drives A Beat in ProfitabilityDokument14 SeitenWipro: CMP: INR243 TP: INR260 (+7%) Largely in Line Lower ETR Drives A Beat in ProfitabilityPramod KulkarniNoch keine Bewertungen

- 2020 09 24 PH S Mpi PDFDokument7 Seiten2020 09 24 PH S Mpi PDFJNoch keine Bewertungen

- 9M16 Net Income Up 5.8% On Higher Earnings Contribution From SubsidiariesDokument4 Seiten9M16 Net Income Up 5.8% On Higher Earnings Contribution From SubsidiariesJajahinaNoch keine Bewertungen

- Aboitiz Equity Ventures: 3Q10 Core Net Income Rises 116.7%, 9M10 Results Above Consensus EstimateDokument3 SeitenAboitiz Equity Ventures: 3Q10 Core Net Income Rises 116.7%, 9M10 Results Above Consensus EstimateJNoch keine Bewertungen

- Positives Already Priced In, Share Dilution To Drag Short-Term EPSDokument7 SeitenPositives Already Priced In, Share Dilution To Drag Short-Term EPSJajahinaNoch keine Bewertungen

- Revising Estimates On Normalized Loan Growth Outlook Maintain BUY RatingDokument6 SeitenRevising Estimates On Normalized Loan Growth Outlook Maintain BUY RatingJM CrNoch keine Bewertungen

- AGUILA 420 User Manual ENDokument32 SeitenAGUILA 420 User Manual ENJM CrNoch keine Bewertungen

- LTG Group, Inc.: Trading SignalsDokument3 SeitenLTG Group, Inc.: Trading SignalsJM CrNoch keine Bewertungen

- 200224-RESEARCHREP WeeklyMarketBlueprint24Feb20to28Feb20Dokument4 Seiten200224-RESEARCHREP WeeklyMarketBlueprint24Feb20to28Feb20JM CrNoch keine Bewertungen

- US: Dow Jones: Recommendaton: Support: ResistanceDokument4 SeitenUS: Dow Jones: Recommendaton: Support: ResistanceJM CrNoch keine Bewertungen

- 200224-RESEARCHREP WeeklyMarketBlueprint24Feb20to28Feb20Dokument4 Seiten200224-RESEARCHREP WeeklyMarketBlueprint24Feb20to28Feb20JM CrNoch keine Bewertungen

- 2018 02 14 PH S BloomDokument7 Seiten2018 02 14 PH S BloomJM CrNoch keine Bewertungen

- Phil Tech GuideDokument3 SeitenPhil Tech GuideJM CrNoch keine Bewertungen

- 2017 Profits of Most Companies Missed Expectations: Slow and Below Expected Earnings GrowthDokument9 Seiten2017 Profits of Most Companies Missed Expectations: Slow and Below Expected Earnings GrowthJM CrNoch keine Bewertungen

- TechSpotlight Jan 17, 2018Dokument6 SeitenTechSpotlight Jan 17, 2018JM CrNoch keine Bewertungen

- PLDT Inc.: Trading SignalsDokument3 SeitenPLDT Inc.: Trading SignalsJM CrNoch keine Bewertungen

- Weekly Market Snapshot: Philippine EquitiesDokument2 SeitenWeekly Market Snapshot: Philippine EquitiesJM CrNoch keine Bewertungen

- Stock Screen: Riding The Momentum Value Play Yield Seeker Unloved PseiDokument7 SeitenStock Screen: Riding The Momentum Value Play Yield Seeker Unloved PseiJM CrNoch keine Bewertungen

- RESEARCHREP 14feb18Dokument5 SeitenRESEARCHREP 14feb18JM CrNoch keine Bewertungen

- 2018 02 02 PH DDokument5 Seiten2018 02 02 PH DJM CrNoch keine Bewertungen

- Focus Items: Philippine Equity ResearchDokument6 SeitenFocus Items: Philippine Equity ResearchJM CrNoch keine Bewertungen

- AP: Reducing Estimates On Potential Delays in Operation of Power ProjectDokument8 SeitenAP: Reducing Estimates On Potential Delays in Operation of Power ProjectJM CrNoch keine Bewertungen

- RESEARCHREP 01feb18Dokument6 SeitenRESEARCHREP 01feb18JM CrNoch keine Bewertungen

- RESEARCHREP 02feb18Dokument6 SeitenRESEARCHREP 02feb18JM CrNoch keine Bewertungen

- JG Summit Holdings, Inc.: Trading SignalsDokument3 SeitenJG Summit Holdings, Inc.: Trading SignalsJM CrNoch keine Bewertungen

- Other News:: THU 01 FEB 2018Dokument4 SeitenOther News:: THU 01 FEB 2018JM CrNoch keine Bewertungen

- TechSpotlight Jan 17, 2018Dokument6 SeitenTechSpotlight Jan 17, 2018JM CrNoch keine Bewertungen

- RLC: Adjusting Estimates For Rights Offering, Reiterate BUY RatingDokument4 SeitenRLC: Adjusting Estimates For Rights Offering, Reiterate BUY RatingJM CrNoch keine Bewertungen

- Ayala Land Inc.: Trading SignalsDokument3 SeitenAyala Land Inc.: Trading SignalsJM CrNoch keine Bewertungen

- Tech Outlook 1st Half 2018Dokument34 SeitenTech Outlook 1st Half 2018JM CrNoch keine Bewertungen

- Dnp3 Master Ethernet ManualDokument145 SeitenDnp3 Master Ethernet ManualJM CrNoch keine Bewertungen

- AP Us History - How To Write A DBQ 1Dokument9 SeitenAP Us History - How To Write A DBQ 1JM CrNoch keine Bewertungen

- Licenses Building CriteriaDokument10 SeitenLicenses Building CriteriaLee RobuzaNoch keine Bewertungen

- Lessons Learned TemplateDokument1 SeiteLessons Learned TemplateJM CrNoch keine Bewertungen

- CBN Exchange Control ManualDokument133 SeitenCBN Exchange Control ManualAhmad Invaluable AdenijiNoch keine Bewertungen

- Financial Management ProjectDokument6 SeitenFinancial Management ProjectShahid AbbasNoch keine Bewertungen

- Unit I 17082019Dokument93 SeitenUnit I 17082019mananNoch keine Bewertungen

- Tax RTP 2019 PDFDokument40 SeitenTax RTP 2019 PDFvenkateshNoch keine Bewertungen

- Important Notes For AccountingDokument66 SeitenImportant Notes For AccountingSana KhursheedNoch keine Bewertungen

- Morepen Laboratories Press Release Q1 PDFDokument5 SeitenMorepen Laboratories Press Release Q1 PDFgaurav chaudharyNoch keine Bewertungen

- Managerial Economics Q4Dokument2 SeitenManagerial Economics Q4Willy DangueNoch keine Bewertungen

- CamlinDokument48 SeitenCamlinJugal ShahNoch keine Bewertungen

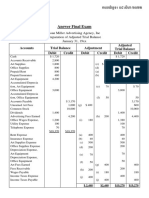

- Answer Final Exam (POA)Dokument2 SeitenAnswer Final Exam (POA)Phâk Tèr ÑgNoch keine Bewertungen

- Accounting For Managers Question BankDokument5 SeitenAccounting For Managers Question BankbhfunNoch keine Bewertungen

- Going International Analysis Project - Tea From Vietnam To PakistanDokument17 SeitenGoing International Analysis Project - Tea From Vietnam To PakistanThanhTung HoangNoch keine Bewertungen

- BCGDokument138 SeitenBCGANKUSHSINGH2690Noch keine Bewertungen

- ISAK 35 Non Profit Oriented EntitiesDokument48 SeitenISAK 35 Non Profit Oriented Entitiesnabila dhiyaNoch keine Bewertungen

- Revised Conceptual Framework: Rsoriano/JmaglinaoDokument2 SeitenRevised Conceptual Framework: Rsoriano/JmaglinaoMerliza JusayanNoch keine Bewertungen

- GHR JobsDokument1 SeiteGHR JobsaliNoch keine Bewertungen

- 2 Statement of Comprehensive IncomeDokument27 Seiten2 Statement of Comprehensive IncomeMichael Lalim Jr.Noch keine Bewertungen

- Financial Analysis of Fauji Cement LTDDokument27 SeitenFinancial Analysis of Fauji Cement LTDMBA...KIDNoch keine Bewertungen

- 2009 AnnualReport EmailDokument145 Seiten2009 AnnualReport EmailDaniel Smart OdogwuNoch keine Bewertungen

- Npos vs. PoDokument4 SeitenNpos vs. Pocindycanlas_07Noch keine Bewertungen

- Ratio Analysis - BBA ClassDokument27 SeitenRatio Analysis - BBA ClassSophiya PrabinNoch keine Bewertungen

- Annual ReportDokument220 SeitenAnnual ReportAnushree VijNoch keine Bewertungen

- FABM1 - Lesson-13 - Concepts & PrinciplesDokument31 SeitenFABM1 - Lesson-13 - Concepts & PrinciplesBP CabreraNoch keine Bewertungen

- Identify The Choice That Best Completes The Statement or Answers The QuestionDokument5 SeitenIdentify The Choice That Best Completes The Statement or Answers The QuestionErine ContranoNoch keine Bewertungen

- Tutorial 9 QsDokument7 SeitenTutorial 9 QsDylan Rabin PereiraNoch keine Bewertungen

- BSCDokument31 SeitenBSCRashed MiaNoch keine Bewertungen

- A Level Accounting Papers Nov2010Dokument145 SeitenA Level Accounting Papers Nov2010frieda20093835Noch keine Bewertungen

- Pritam Ajay Puro: Mar 2008 - Till Date Intelenet Global Services Pvt. LTDDokument3 SeitenPritam Ajay Puro: Mar 2008 - Till Date Intelenet Global Services Pvt. LTDdeepaku1Noch keine Bewertungen

- Juan Antonio Perez Search Warrant NDGADokument22 SeitenJuan Antonio Perez Search Warrant NDGADan LehrNoch keine Bewertungen

- CFA MindmapDokument98 SeitenCFA MindmapHongjun Yin92% (12)

- Lupin, 4th February, 2013Dokument11 SeitenLupin, 4th February, 2013Angel BrokingNoch keine Bewertungen