Das könnte Ihnen auch gefallen

- Regional Rural Banks of India: Evolution, Performance and ManagementVon EverandRegional Rural Banks of India: Evolution, Performance and ManagementNoch keine Bewertungen

- PDF Credit Analysis of Personal Loan HDFC Bank Specialisation ProjectDokument89 SeitenPDF Credit Analysis of Personal Loan HDFC Bank Specialisation ProjectTejas BhavsarNoch keine Bewertungen

- Central BankDokument10 SeitenCentral BankVrinda TayadeNoch keine Bewertungen

- Consumer Finance..yatith Poojari (Yp)Dokument67 SeitenConsumer Finance..yatith Poojari (Yp)Yatith PoojariNoch keine Bewertungen

- Market Structure For Retail Banking Services in MauritiusDokument19 SeitenMarket Structure For Retail Banking Services in MauritiusBenita KonglarNoch keine Bewertungen

- Overview of Credit AppraisalDokument14 SeitenOverview of Credit AppraisalAsim MahatoNoch keine Bewertungen

- Personal Load in SbiDokument42 SeitenPersonal Load in SbiNitinAgnihotriNoch keine Bewertungen

- 1302-19-672-030 SynopsisDokument17 Seiten1302-19-672-030 SynopsisMohmmedKhayyumNoch keine Bewertungen

- Icici Bank Project Summer Internship Program 2020Dokument45 SeitenIcici Bank Project Summer Internship Program 2020Bhavna PatnaikNoch keine Bewertungen

- A Study of Credit Assessment in Dena BankDokument48 SeitenA Study of Credit Assessment in Dena BankDeepali MahilagiriNoch keine Bewertungen

- Malaysia: Finance Debt Collateralized Lien Bankruptcy LiquidationDokument2 SeitenMalaysia: Finance Debt Collateralized Lien Bankruptcy LiquidationAkhil UchilNoch keine Bewertungen

- Fixed DepositDokument37 SeitenFixed DepositMinal DalviNoch keine Bewertungen

- SBI Home Loan TMV BlackbookDokument106 SeitenSBI Home Loan TMV Blackbookvishal birajdarNoch keine Bewertungen

- Presentation On Export CreditDokument21 SeitenPresentation On Export CreditArpit KhandelwalNoch keine Bewertungen

- Home Loan - A Comparitive Study at BOIDokument86 SeitenHome Loan - A Comparitive Study at BOIRuchi Prabhu100% (2)

- A Study On HDFC Bank LTDDokument17 SeitenA Study On HDFC Bank LTDbahaaraujlaNoch keine Bewertungen

- A Compartive Study On Problems and Prospect of Tax System of Nepal 2016Dokument98 SeitenA Compartive Study On Problems and Prospect of Tax System of Nepal 2016Saroj BhusalNoch keine Bewertungen

- Portfolio RevisionDokument24 SeitenPortfolio RevisionrajunscNoch keine Bewertungen

- A Project Report ON Recruitment and Selection in ICICI Bank LTDDokument8 SeitenA Project Report ON Recruitment and Selection in ICICI Bank LTDnitika_gupta219481Noch keine Bewertungen

- Blackbook Project On Indian Banking Sector 2Dokument119 SeitenBlackbook Project On Indian Banking Sector 2anilmourya5Noch keine Bewertungen

- To Study Credit Appraisal in Home Loan Fin - Final - Docx 1Dokument69 SeitenTo Study Credit Appraisal in Home Loan Fin - Final - Docx 1Swapnil BhagatNoch keine Bewertungen

- Types of Deposits Offered by BanksDokument6 SeitenTypes of Deposits Offered by Banksfarhana nasreenNoch keine Bewertungen

- MBA Finance Project On Retail Banking With Special Reference To YES BANKDokument115 SeitenMBA Finance Project On Retail Banking With Special Reference To YES BANKManjeet Singh100% (2)

- HDFC Ltd. Home Loan FeaturesDokument8 SeitenHDFC Ltd. Home Loan FeaturesVishv SharmaNoch keine Bewertungen

- HardikDokument28 SeitenHardikKeyur PatelNoch keine Bewertungen

- Kotak Mahindra BankDokument15 SeitenKotak Mahindra BankEr Dipankar SaikiaNoch keine Bewertungen

- A Project On Banking SectorDokument81 SeitenA Project On Banking SectorAkbar SinghNoch keine Bewertungen

- CMS Report 1Dokument101 SeitenCMS Report 1Kamal PurohitNoch keine Bewertungen

- PNB Roi New Supplementry Agreement-WordDokument2 SeitenPNB Roi New Supplementry Agreement-WordAnonymous XsYDXMVNoch keine Bewertungen

- Customer Satisfaction Bank LoanDokument84 SeitenCustomer Satisfaction Bank LoanAshish Khandelwal33% (3)

- Home LoanDokument19 SeitenHome LoanghanshyamNoch keine Bewertungen

- 205 - F - Icici-A Study On Credit Appraisal System at Icici BankDokument71 Seiten205 - F - Icici-A Study On Credit Appraisal System at Icici BankPeacock Live Projects0% (1)

- Non - Performing Assests (Npa'S)Dokument12 SeitenNon - Performing Assests (Npa'S)Suhit SarodeNoch keine Bewertungen

- Organization StructureDokument1 SeiteOrganization StructureShruti SharmaNoch keine Bewertungen

- Axis BankDokument117 SeitenAxis BankGufran Shaikh100% (2)

- Assessment of Working Capital LimitDokument4 SeitenAssessment of Working Capital LimitKeshav Malpani100% (8)

- Cash Flow StatmentDokument91 SeitenCash Flow StatmentSathishmuNoch keine Bewertungen

- Lit Rview Credit AppraisalDokument4 SeitenLit Rview Credit AppraisalHari KrishnanNoch keine Bewertungen

- Comprehensive Study On Financial Analysis of HDFC Bank: Prepared byDokument38 SeitenComprehensive Study On Financial Analysis of HDFC Bank: Prepared byshrutilatherNoch keine Bewertungen

- Home LoansDokument40 SeitenHome LoansPrashant K. SinghNoch keine Bewertungen

- Asset & Liability Management of Urban Co-Op BankDokument70 SeitenAsset & Liability Management of Urban Co-Op BankAbhiroop Bhattacharjee100% (1)

- Manappuram Finance: Positive All-Round Results Should Set The ToneDokument8 SeitenManappuram Finance: Positive All-Round Results Should Set The Tonevikasaggarwal01Noch keine Bewertungen

- SynopsisDokument7 SeitenSynopsisAnchalNoch keine Bewertungen

- Financial Statement Analysis of Icici BankDokument24 SeitenFinancial Statement Analysis of Icici BankPadmavati UdechaNoch keine Bewertungen

- Credit Appraisal of Project Financing and Working CapitalDokument70 SeitenCredit Appraisal of Project Financing and Working CapitalSami ZamaNoch keine Bewertungen

- Working Capital of Borrower-Bank of BarodaDokument82 SeitenWorking Capital of Borrower-Bank of BarodaRaj KopadeNoch keine Bewertungen

- THEJASWINI ProjectDokument112 SeitenTHEJASWINI Projectswamy yashuNoch keine Bewertungen

- Retail Banking of Allahabad BankDokument50 SeitenRetail Banking of Allahabad Bankaru161112Noch keine Bewertungen

- Comparative Analysis Report On Npa of Pubic & Private Sector BankDokument10 SeitenComparative Analysis Report On Npa of Pubic & Private Sector BankMBA SEM 3 2019Noch keine Bewertungen

- Project On HDFC BankDokument72 SeitenProject On HDFC Banksunit2658Noch keine Bewertungen

- An Overview of Credit Appresal Process With Special Reference To Differnent Loans Offer by Indian BankDokument86 SeitenAn Overview of Credit Appresal Process With Special Reference To Differnent Loans Offer by Indian BankAbhinandan SahooNoch keine Bewertungen

- Bhushan SIP SOM Reviesed 3Dokument52 SeitenBhushan SIP SOM Reviesed 3Akshay SherekarNoch keine Bewertungen

- J&K BankDokument92 SeitenJ&K BankSonali KaulNoch keine Bewertungen

- A Case Study On Customer Relationship Management Strategy LaveshDokument72 SeitenA Case Study On Customer Relationship Management Strategy LaveshNIKHIL SAPKALENoch keine Bewertungen

- BLACKBOOKDokument98 SeitenBLACKBOOKAbhinandan PawarNoch keine Bewertungen

- A Project On Analysis of PrepaymentsDokument118 SeitenA Project On Analysis of PrepaymentsEliza LoboNoch keine Bewertungen

- Tizita ProposalDokument21 SeitenTizita Proposalanwar jemalNoch keine Bewertungen

- Repot On SBIDokument76 SeitenRepot On SBIPrasad SawantNoch keine Bewertungen

- Project Report of Bank of RajasthanDokument97 SeitenProject Report of Bank of RajasthanAman SinghNoch keine Bewertungen

- Predicting Student Action Through Online Examination in An Online TrainingDokument7 SeitenPredicting Student Action Through Online Examination in An Online TrainingNikhil BhaleraoNoch keine Bewertungen

- Admin Panel:: Institute Info Admin Dashboard Department Level Topic Respondents Data Collecting Agent Question BankDokument2 SeitenAdmin Panel:: Institute Info Admin Dashboard Department Level Topic Respondents Data Collecting Agent Question BankNikhil BhaleraoNoch keine Bewertungen

- Unit 1 MCQDokument12 SeitenUnit 1 MCQNikhil BhaleraoNoch keine Bewertungen

- Elecronics MCQDokument7 SeitenElecronics MCQNikhil BhaleraoNoch keine Bewertungen

- Summer Internship Completion Certificate FormatDokument1 SeiteSummer Internship Completion Certificate FormatQasim Peerzada50% (2)

- 2 - A Review On Extracting Top-K Lists From The WebDokument6 Seiten2 - A Review On Extracting Top-K Lists From The WebNikhil BhaleraoNoch keine Bewertungen

- Social EntrepreneurshipDokument4 SeitenSocial EntrepreneurshipNikhil BhaleraoNoch keine Bewertungen

- Enterprise Performance Management MCQDokument20 SeitenEnterprise Performance Management MCQNikhil Bhalerao50% (2)

- An Efficient and Scalable Way Using UP-Growth and UP-Growth+ Algorithms For Finding Mining High Utility Item Sets From Transactional DatabasesDokument12 SeitenAn Efficient and Scalable Way Using UP-Growth and UP-Growth+ Algorithms For Finding Mining High Utility Item Sets From Transactional DatabasesNikhil BhaleraoNoch keine Bewertungen

- 306 FIn Financial System of India Markets & ServicesDokument6 Seiten306 FIn Financial System of India Markets & ServicesNikhil BhaleraoNoch keine Bewertungen

- Cab Service Management ReportDokument125 SeitenCab Service Management ReportUniq ManjuNoch keine Bewertungen

- TVS ProjectDokument57 SeitenTVS ProjectNikhil BhaleraoNoch keine Bewertungen

- Continuous and Transparent User Identit Verification For Secure Internet Services.Dokument4 SeitenContinuous and Transparent User Identit Verification For Secure Internet Services.Nikhil BhaleraoNoch keine Bewertungen

- Social EntrepreneurshipDokument4 SeitenSocial EntrepreneurshipNikhil BhaleraoNoch keine Bewertungen

- AnsiDokument9 SeitenAnsisajeerNoch keine Bewertungen

- Advanced GPS Location FinderDokument4 SeitenAdvanced GPS Location FinderNikhil BhaleraoNoch keine Bewertungen

- Adms and Exam ScheduleDokument3 SeitenAdms and Exam ScheduleMohammad AzimNoch keine Bewertungen

- Applications of Definite IntegralDokument128 SeitenApplications of Definite IntegralNikhil BhaleraoNoch keine Bewertungen

- 10) Linear Programming ProblemsDokument170 Seiten10) Linear Programming ProblemsNikhil Bhalerao100% (7)

- 202 Financial ManagementDokument1 Seite202 Financial ManagementNikhil BhaleraoNoch keine Bewertungen

- OSCM MCQDokument3 SeitenOSCM MCQNikhil BhaleraoNoch keine Bewertungen

- C PRogramming Model Question PaperDokument2 SeitenC PRogramming Model Question PaperNikhil BhaleraoNoch keine Bewertungen

- Decision Science-204 MCQ'sDokument5 SeitenDecision Science-204 MCQ'sNikhil BhaleraoNoch keine Bewertungen

- Sample Physics QuestionsDokument2 SeitenSample Physics QuestionsNikhil BhaleraoNoch keine Bewertungen

- Student Profile FormDokument1 SeiteStudent Profile FormNikhil BhaleraoNoch keine Bewertungen

- Group DiscussionDokument20 SeitenGroup DiscussionUdhayasankar HariharanNoch keine Bewertungen

- Arranging Finance For ExportDokument14 SeitenArranging Finance For ExportmaxsoniiNoch keine Bewertungen

- Appendix 34 - CkADADRecDokument1 SeiteAppendix 34 - CkADADRecMark Joseph BajaNoch keine Bewertungen

- Audit of Statement of Cash FlowsDokument2 SeitenAudit of Statement of Cash FlowsAndrew ManaloNoch keine Bewertungen

- Currency Translation in BPCDokument6 SeitenCurrency Translation in BPCvijay95102Noch keine Bewertungen

- 2nd PT-Business Finance-Final Exam-2022-2023Dokument3 Seiten2nd PT-Business Finance-Final Exam-2022-2023Diane GuilaranNoch keine Bewertungen

- CertificateDokument4 SeitenCertificateMilap NaiduNoch keine Bewertungen

- Key Fact Statement and MITCDokument23 SeitenKey Fact Statement and MITCSumeet ShelarNoch keine Bewertungen

- Composite Debit Balance Confirmation (With Security) (SD 23)Dokument2 SeitenComposite Debit Balance Confirmation (With Security) (SD 23)shailesh more100% (1)

- Soneri Bank Ltd. Company Profile: Key PeoplesDokument4 SeitenSoneri Bank Ltd. Company Profile: Key PeoplesAhmed ShazadNoch keine Bewertungen

- Functions of PFC (Power Finance Corporation)Dokument2 SeitenFunctions of PFC (Power Finance Corporation)nits1380Noch keine Bewertungen

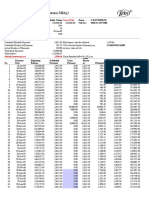

- Microsoft Excel Sheet For Calculating EMI (Equated Monthly Installment) (TYPE 1)Dokument31 SeitenMicrosoft Excel Sheet For Calculating EMI (Equated Monthly Installment) (TYPE 1)Vikas Acharya100% (1)

- Chap 1Dokument19 SeitenChap 1p4priyaNoch keine Bewertungen

- Investing in Germany 101Dokument28 SeitenInvesting in Germany 101Ernesto Diaz HernandezNoch keine Bewertungen

- Risk Management in Indian Banks: Some Emerging Issues: Dr. Krishn A.Goyal, Int. Eco. J. Res., 2010 1 (1) 102-109Dokument8 SeitenRisk Management in Indian Banks: Some Emerging Issues: Dr. Krishn A.Goyal, Int. Eco. J. Res., 2010 1 (1) 102-109Shukla JineshNoch keine Bewertungen

- Overall Performance Evaluation of Agrani Bank Limited-2016Dokument56 SeitenOverall Performance Evaluation of Agrani Bank Limited-2016SharifMahmud100% (4)

- Chap3 ALTDokument4 SeitenChap3 ALTOFORINoch keine Bewertungen

- UOB Phone Banking GuideDokument2 SeitenUOB Phone Banking GuideAldrin LapitanNoch keine Bewertungen

- Financial Services: Securities Brokerage and Investment BankingDokument16 SeitenFinancial Services: Securities Brokerage and Investment BankingSta KerNoch keine Bewertungen

- Sanction Letter FAST7651617444854859 371328176989144Dokument7 SeitenSanction Letter FAST7651617444854859 371328176989144hm7072302Noch keine Bewertungen

- Axis Bank Young Banker Programme Internship Diary: Suneet Kumar SinghDokument9 SeitenAxis Bank Young Banker Programme Internship Diary: Suneet Kumar Singhsrinivas4949Noch keine Bewertungen

- BOARD RESOLUTION TABLE 2017 FinalDokument13 SeitenBOARD RESOLUTION TABLE 2017 FinalHoney MedinaNoch keine Bewertungen

- GB PDFDokument359 SeitenGB PDFUlaganathanNoch keine Bewertungen

- 21-03-23 - Kikori Forest DepartmentDokument1 Seite21-03-23 - Kikori Forest DepartmentPaul KeruaNoch keine Bewertungen

- Accounting Processes For Remittance To PLIsDokument12 SeitenAccounting Processes For Remittance To PLIsjojeNoch keine Bewertungen

- Interbank Giro Credit CardDokument1 SeiteInterbank Giro Credit CardJulius Putra Tanu SetiajiNoch keine Bewertungen

- AsdfghjklDokument2 SeitenAsdfghjklAdventurous FreakNoch keine Bewertungen

- Saqib Ahmad MirDokument18 SeitenSaqib Ahmad Mirsaqib mirNoch keine Bewertungen

- N26 - OverviewDokument25 SeitenN26 - OverviewGajendra AudichyaNoch keine Bewertungen

- Mobile Services: Your Account Summary This Month'S ChargesDokument5 SeitenMobile Services: Your Account Summary This Month'S ChargesParvatiNoch keine Bewertungen

- Barclays Bank UPDATEDokument32 SeitenBarclays Bank UPDATEAbdul wahidNoch keine Bewertungen