Das könnte Ihnen auch gefallen

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsVon EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNoch keine Bewertungen

- ACCT3500 (Fall 20) Answers To Tutorial 3Dokument7 SeitenACCT3500 (Fall 20) Answers To Tutorial 3Mohammad ShabirNoch keine Bewertungen

- Cost Management: A Case for Business Process Re-engineeringVon EverandCost Management: A Case for Business Process Re-engineeringNoch keine Bewertungen

- Management Accounting 1 Group Assignment FIRST SEMESTER 2022 - 2121910004301Dokument12 SeitenManagement Accounting 1 Group Assignment FIRST SEMESTER 2022 - 2121910004301Quế Phương NguyễnNoch keine Bewertungen

- Another Solved Example of Cost DirivesDokument4 SeitenAnother Solved Example of Cost DirivesMazhar JamNoch keine Bewertungen

- University of Finance and MarketingDokument8 SeitenUniversity of Finance and MarketingQuế Phương NguyễnNoch keine Bewertungen

- Activity Based Costing: Presented By: Anurag Garg Himanshu Sumit Garg AnjliDokument17 SeitenActivity Based Costing: Presented By: Anurag Garg Himanshu Sumit Garg AnjliSumit GargNoch keine Bewertungen

- ABC Costing Autumn 19Dokument15 SeitenABC Costing Autumn 19Tory IslamNoch keine Bewertungen

- Activity Based CostingDokument50 SeitenActivity Based CostingParamjit Sharma97% (65)

- Chapter 5. Activity Based CostingDokument28 SeitenChapter 5. Activity Based CostingbellaNoch keine Bewertungen

- 6e ch06Dokument53 Seiten6e ch06Cholifah Husti LailaNoch keine Bewertungen

- ABC Hansen & Mowen ch4 P ('t':'3', 'I':'669594619') D '' Var B Location Settimeout (Function ( If (Typeof Window - Iframe 'Undefined') ( B.href B.href ) ), 15000)Dokument22 SeitenABC Hansen & Mowen ch4 P ('t':'3', 'I':'669594619') D '' Var B Location Settimeout (Function ( If (Typeof Window - Iframe 'Undefined') ( B.href B.href ) ), 15000)Aziza AmranNoch keine Bewertungen

- Tahmina Ahmed Instructor Cost AccountingDokument19 SeitenTahmina Ahmed Instructor Cost Accountingfaraazxbox1Noch keine Bewertungen

- Chapter 5Dokument9 SeitenChapter 5Dishantely SamboNoch keine Bewertungen

- Lecture 6 - ABC Costing RevisedDokument22 SeitenLecture 6 - ABC Costing RevisedMJ jNoch keine Bewertungen

- Activity Based CostingDokument49 SeitenActivity Based CostingEdson EdwardNoch keine Bewertungen

- B01 AbcDokument21 SeitenB01 AbcAcca BooksNoch keine Bewertungen

- QuantumTM Case Study-Team 2Dokument26 SeitenQuantumTM Case Study-Team 2RavNeet KaUr100% (1)

- PPC Ch. 4Dokument20 SeitenPPC Ch. 4Mulugeta WoldeNoch keine Bewertungen

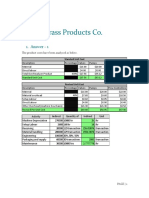

- Documents - MX - Destin Brass Products Co 55f065486abf6 PDFDokument9 SeitenDocuments - MX - Destin Brass Products Co 55f065486abf6 PDFNikhil WadhwaniNoch keine Bewertungen

- City Buildings Business PowerPoint TemplateDokument15 SeitenCity Buildings Business PowerPoint TemplateSalman SajidNoch keine Bewertungen

- Activity-Based Costing: Mcgraw-Hill/IrwinDokument17 SeitenActivity-Based Costing: Mcgraw-Hill/IrwinImran KhanNoch keine Bewertungen

- HBS SolutionDokument6 SeitenHBS Solutionabdulazeem_cfeNoch keine Bewertungen

- Ch04 Activity Based CostingDokument52 SeitenCh04 Activity Based CostingDaniel John Cañares LegaspiNoch keine Bewertungen

- ACC60181H619 Managerial AccountingDokument9 SeitenACC60181H619 Managerial AccountingaksNoch keine Bewertungen

- Chapter 6 - Process CostingDokument53 SeitenChapter 6 - Process CostingHARYATI SETYORININoch keine Bewertungen

- Activity Based Costing: By: Kasahun N. (M.SC.)Dokument20 SeitenActivity Based Costing: By: Kasahun N. (M.SC.)Mulugeta WoldeNoch keine Bewertungen

- ABC Costing Lecture1Dokument12 SeitenABC Costing Lecture1Nusrat JahanNoch keine Bewertungen

- Sanders CompanyDokument6 SeitenSanders CompanyculadiNoch keine Bewertungen

- Chapter 5 ABC - ABM PDFDokument31 SeitenChapter 5 ABC - ABM PDFdiky supriadiNoch keine Bewertungen

- Exercise 6.6 To 6.9Dokument6 SeitenExercise 6.6 To 6.9sajjadNoch keine Bewertungen

- Activity Based CostingDokument49 SeitenActivity Based CostingAries Gonzales CaraganNoch keine Bewertungen

- 1415j M Sesi 03 04 Akuntansi Manajemen Biaya AktivitasDokument54 Seiten1415j M Sesi 03 04 Akuntansi Manajemen Biaya AktivitasAnonymous yMOMM9bsNoch keine Bewertungen

- Chapter 4Dokument14 SeitenChapter 4mikeNoch keine Bewertungen

- Tugas CMA Soal 8-45 Dan 8-46 Richard Andrew - 8312419003 Fix PDFDokument12 SeitenTugas CMA Soal 8-45 Dan 8-46 Richard Andrew - 8312419003 Fix PDFsNoch keine Bewertungen

- Test-Bank-2 CostDokument8 SeitenTest-Bank-2 CostRaneNoch keine Bewertungen

- Ch06 Guan CM AiseDokument53 SeitenCh06 Guan CM AiseFlorensia RestianNoch keine Bewertungen

- Charles AKMENDokument11 SeitenCharles AKMENCharles GohNoch keine Bewertungen

- Assignment Question AccDokument5 SeitenAssignment Question AccruqayyahqaisaraNoch keine Bewertungen

- Cost Accounting Tutorial 10 - ProblemDokument2 SeitenCost Accounting Tutorial 10 - ProblemHadila Franciska StevanyNoch keine Bewertungen

- Activity-Based Costing: Activity-Based Costing Is The Best Functional-Based Costing Is Good For UsDokument32 SeitenActivity-Based Costing: Activity-Based Costing Is The Best Functional-Based Costing Is Good For UsRichardNoch keine Bewertungen

- Tijuana Bronze MachiningDokument19 SeitenTijuana Bronze MachiningYoong YingNoch keine Bewertungen

- Group 7 - Excel - Destin BrassDokument9 SeitenGroup 7 - Excel - Destin BrassSaumya SahaNoch keine Bewertungen

- WP Assignment Week 5 AMLDokument8 SeitenWP Assignment Week 5 AMLIndahna SulfaNoch keine Bewertungen

- Strategic ManagementDokument10 SeitenStrategic Managementstk2796Noch keine Bewertungen

- Problem-2.28 - & - 3.32 HMDokument8 SeitenProblem-2.28 - & - 3.32 HMCorry MargarethaNoch keine Bewertungen

- Process CostingDokument66 SeitenProcess Costingarshad mNoch keine Bewertungen

- Sesi 9 Process CostDokument76 SeitenSesi 9 Process CostAnggrainiNoch keine Bewertungen

- ACCA F5 Course NotesDokument273 SeitenACCA F5 Course NotesLinkon Peter50% (2)

- ABC Model For A UniversityDokument20 SeitenABC Model For A UniversityrahulNoch keine Bewertungen

- Process CostingDokument16 SeitenProcess CostingvijayNoch keine Bewertungen

- Chapter 2 Activity Based Costing: 1. ObjectivesDokument13 SeitenChapter 2 Activity Based Costing: 1. ObjectivesNilda CorpuzNoch keine Bewertungen

- 5-31 Original Activity-Based Costing, Activity-Based ManagementDokument12 Seiten5-31 Original Activity-Based Costing, Activity-Based ManagementJim ChaNoch keine Bewertungen

- Total Machine Hours:: Suggested Solution Maf451 (June 2016) QUESTION 1: AnswerDokument8 SeitenTotal Machine Hours:: Suggested Solution Maf451 (June 2016) QUESTION 1: Answeranis izzatiNoch keine Bewertungen

- Final Managerial 2016 SolutionDokument10 SeitenFinal Managerial 2016 SolutionRanim HfaidhiaNoch keine Bewertungen

- Managerial Accounting Homework 1.3Dokument5 SeitenManagerial Accounting Homework 1.3OvidiaNoch keine Bewertungen

- Destin Brass Products Co.: 1. Answer - 1Dokument5 SeitenDestin Brass Products Co.: 1. Answer - 1Chetan DasguptaNoch keine Bewertungen

- ManaktugasDokument7 SeitenManaktugasNimas KartikaNoch keine Bewertungen

- Getting Started - Bullet Journal PDFDokument17 SeitenGetting Started - Bullet Journal PDFi1153315100% (4)

- Project List: Work Home Social OtherDokument5 SeitenProject List: Work Home Social Otheri1153315Noch keine Bewertungen

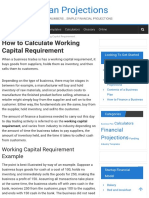

- How To Calculate Working Capital Requirement - Plan ProjectionsDokument7 SeitenHow To Calculate Working Capital Requirement - Plan Projectionsi1153315Noch keine Bewertungen

- Daily-To-Do-List-Template Variant 1Dokument1 SeiteDaily-To-Do-List-Template Variant 1i1153315Noch keine Bewertungen

- Status Priority Due Date Project / Task To Be Done: Daily To Do ListDokument2 SeitenStatus Priority Due Date Project / Task To Be Done: Daily To Do Listi1153315Noch keine Bewertungen

- Daily-To-Do-List-Template Variant 2Dokument4 SeitenDaily-To-Do-List-Template Variant 2i1153315Noch keine Bewertungen

- Loan Amortization ScheduleDokument4 SeitenLoan Amortization ScheduleBlasius Aditya Putra PermanaNoch keine Bewertungen

- Rate Changes - NatWest International 20150731Dokument1 SeiteRate Changes - NatWest International 20150731i1153315Noch keine Bewertungen

- Rate Changes - NatWest International 20171102Dokument1 SeiteRate Changes - NatWest International 20171102i1153315Noch keine Bewertungen

- General Data Protection Regulation (GDPR) - Final Text Neatly ArrangedDokument6 SeitenGeneral Data Protection Regulation (GDPR) - Final Text Neatly Arrangedi1153315Noch keine Bewertungen

- Rate Changes - NatWest International 20150731Dokument1 SeiteRate Changes - NatWest International 20150731i1153315Noch keine Bewertungen

- EU General Data Protection Regulation Training GDPRDokument2 SeitenEU General Data Protection Regulation Training GDPRi1153315Noch keine Bewertungen

- ZA Palisade Conference Mining Rehab ModellingDokument30 SeitenZA Palisade Conference Mining Rehab Modellingi1153315Noch keine Bewertungen

- Modeling With @risk: A Tutorial GuideDokument31 SeitenModeling With @risk: A Tutorial Guidei1153315Noch keine Bewertungen

- TIME MANAGEMENT WITH OUTLOOK Download PDFDokument45 SeitenTIME MANAGEMENT WITH OUTLOOK Download PDFi1153315Noch keine Bewertungen

- What Are The Chances of That Quantification With Monte Carlo Simulation, Doug Oldfield, PalisadeDokument21 SeitenWhat Are The Chances of That Quantification With Monte Carlo Simulation, Doug Oldfield, Palisadei1153315Noch keine Bewertungen

- Using Risk With Invest For ExcelDokument9 SeitenUsing Risk With Invest For Exceli1153315Noch keine Bewertungen

- Optimization of S S Periodic Review Inventory ModeDokument15 SeitenOptimization of S S Periodic Review Inventory Modei1153315Noch keine Bewertungen

- Manifest Destiny - WikipediaDokument28 SeitenManifest Destiny - Wikipediai1153315Noch keine Bewertungen

- VPN GitHub - Diafygi Webrtc-Ips Demo Https Diafygi - GithubDokument2 SeitenVPN GitHub - Diafygi Webrtc-Ips Demo Https Diafygi - Githubi1153315Noch keine Bewertungen

- Upadhyayaetal TrueliqtrigcurveDokument14 SeitenUpadhyayaetal TrueliqtrigcurveVetriselvan ArumugamNoch keine Bewertungen

- Invoice ApprovalDokument54 SeitenInvoice ApprovalHamada Asmr AladhamNoch keine Bewertungen

- PC Engines APU2 Series System BoardDokument11 SeitenPC Engines APU2 Series System Boardpdy2Noch keine Bewertungen

- LP MAPEH 10 1st Quarter Printing Final.Dokument29 SeitenLP MAPEH 10 1st Quarter Printing Final.tatineeesamonteNoch keine Bewertungen

- Work Permits New Guideline Amendments 2021 23.11.2021Dokument7 SeitenWork Permits New Guideline Amendments 2021 23.11.2021Sabrina BrathwaiteNoch keine Bewertungen

- ARTS10 Q2 ModuleDokument12 SeitenARTS10 Q2 ModuleDen Mark GacumaNoch keine Bewertungen

- Adsorption ExperimentDokument5 SeitenAdsorption ExperimentNauman KhalidNoch keine Bewertungen

- Quiz 2 I - Prefix and Suffix TestDokument10 SeitenQuiz 2 I - Prefix and Suffix Testguait9Noch keine Bewertungen

- 1 - DIASS Trisha Ma-WPS OfficeDokument2 Seiten1 - DIASS Trisha Ma-WPS OfficeMae ZelNoch keine Bewertungen

- Service Letter Service Letter Service Letter Service Letter: Commercial Aviation ServicesDokument3 SeitenService Letter Service Letter Service Letter Service Letter: Commercial Aviation ServicesSamarNoch keine Bewertungen

- Visual Inspection ReportDokument45 SeitenVisual Inspection ReportKhoirul AnamNoch keine Bewertungen

- Southern California International Gateway Final Environmental Impact ReportDokument40 SeitenSouthern California International Gateway Final Environmental Impact ReportLong Beach PostNoch keine Bewertungen

- Model No. TH-65JX850M/MF Chassis. 9K56T: LED TelevisionDokument53 SeitenModel No. TH-65JX850M/MF Chassis. 9K56T: LED TelevisionRavi ChandranNoch keine Bewertungen

- Programming MillDokument81 SeitenProgramming MillEddy ZalieNoch keine Bewertungen

- Translations Telugu To English A ClassifDokument111 SeitenTranslations Telugu To English A ClassifGummadi Vijaya KumarNoch keine Bewertungen

- Hauling AgreementDokument2 SeitenHauling AgreementE.A. Francisco Trucking100% (3)

- Model DPR & Application Form For Integrated RAS PDFDokument17 SeitenModel DPR & Application Form For Integrated RAS PDFAnbu BalaNoch keine Bewertungen

- Under Suitable Conditions, Butane, C: © OCR 2022. You May Photocopy ThisDokument13 SeitenUnder Suitable Conditions, Butane, C: © OCR 2022. You May Photocopy ThisMahmud RahmanNoch keine Bewertungen

- Analysis of MMDR Amendment ActDokument5 SeitenAnalysis of MMDR Amendment ActArunabh BhattacharyaNoch keine Bewertungen

- Earth and Life Science, Grade 11Dokument6 SeitenEarth and Life Science, Grade 11Gregorio RizaldyNoch keine Bewertungen

- White Cataract What To AssesDokument2 SeitenWhite Cataract What To Assesalif andraNoch keine Bewertungen

- HG32High-Frequency Welded Pipe Mill Line - Pakistan 210224Dokument14 SeitenHG32High-Frequency Welded Pipe Mill Line - Pakistan 210224Arslan AbbasNoch keine Bewertungen

- Category (7) - Installation and Maintenance of Instrumentation and Control SystemsDokument3 SeitenCategory (7) - Installation and Maintenance of Instrumentation and Control Systemstafseerahmed86Noch keine Bewertungen

- Iit-Jam Mathematics Test: Modern Algebra Time: 60 Minutes Date: 08-10-2017 M.M.: 45Dokument6 SeitenIit-Jam Mathematics Test: Modern Algebra Time: 60 Minutes Date: 08-10-2017 M.M.: 45Lappy TopNoch keine Bewertungen

- The Chulalongkorn Centenary ParkDokument6 SeitenThe Chulalongkorn Centenary ParkJack FooNoch keine Bewertungen

- Categories of Cargo and Types of ShipsDokument14 SeitenCategories of Cargo and Types of ShipsVibhav Kumar100% (1)

- Aqa Ms Ss1a W QP Jun13Dokument20 SeitenAqa Ms Ss1a W QP Jun13prsara1975Noch keine Bewertungen

- Performance Evaluation of The KVM Hypervisor Running On Arm-Based Single-Board ComputersDokument18 SeitenPerformance Evaluation of The KVM Hypervisor Running On Arm-Based Single-Board ComputersAIRCC - IJCNCNoch keine Bewertungen

- PPT-QC AcDokument34 SeitenPPT-QC AcAmlan Chakrabarti Calcutta UniversityNoch keine Bewertungen

- 2008 Kershaw CatalogDokument38 Seiten2008 Kershaw CatalogDANILA MARECHEKNoch keine Bewertungen