Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Print MFSDokument28 SeitenPrint MFSvijaybharvadNoch keine Bewertungen

- Print MFSDokument28 SeitenPrint MFSvijaybharvadNoch keine Bewertungen

- Print MFSDokument28 SeitenPrint MFSvijaybharvadNoch keine Bewertungen

- MFS PPT FinalDokument18 SeitenMFS PPT FinalvijaybharvadNoch keine Bewertungen

- MFS PPT FinalDokument18 SeitenMFS PPT FinalvijaybharvadNoch keine Bewertungen

- Payal 111Dokument1 SeitePayal 111vijaybharvadNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Enron ScandalDokument9 SeitenEnron ScandalRohith MohanNoch keine Bewertungen

- RCC Title IIDokument19 SeitenRCC Title IITanya Mia PerezNoch keine Bewertungen

- Assignment 1 BriefDokument5 SeitenAssignment 1 BriefViet NguyenNoch keine Bewertungen

- Causes and Effects Into Reasons For The Decline of Wood Cable Reels Production in The CompanyDokument7 SeitenCauses and Effects Into Reasons For The Decline of Wood Cable Reels Production in The CompanyQueryy DavidNoch keine Bewertungen

- FORM Job Safety AnalysisDokument3 SeitenFORM Job Safety AnalysisMyra CahyatiNoch keine Bewertungen

- Annex 5 - RCRD - CabarambananDokument4 SeitenAnnex 5 - RCRD - CabarambananLikey PromiseNoch keine Bewertungen

- War22e Ch13Dokument77 SeitenWar22e Ch13tamparddNoch keine Bewertungen

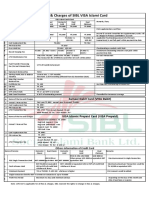

- Fees and Charges of SIBL Islami CardDokument1 SeiteFees and Charges of SIBL Islami CardMd YusufNoch keine Bewertungen

- Review of Related Literature FinalDokument6 SeitenReview of Related Literature Finalmacrisa caraganNoch keine Bewertungen

- An Introduction To Integrated Marketing CommunicationsDokument42 SeitenAn Introduction To Integrated Marketing CommunicationsShuvroNoch keine Bewertungen

- Business Options and Business Plan in Haldwani and KathgodamDokument17 SeitenBusiness Options and Business Plan in Haldwani and KathgodamShivam ShardaNoch keine Bewertungen

- Internal Quality Management System Audit Checklist (ISO/TS 16949:2009)Dokument48 SeitenInternal Quality Management System Audit Checklist (ISO/TS 16949:2009)sharif1974Noch keine Bewertungen

- Kal Atm Software Trends and Analysis 2014 PDFDokument61 SeitenKal Atm Software Trends and Analysis 2014 PDFlcarrionNoch keine Bewertungen

- Strategic Management 2nd Edition Rothaermel Solutions ManualDokument25 SeitenStrategic Management 2nd Edition Rothaermel Solutions ManualTracySnydereigtc100% (38)

- This Study Resource Was: Joyce Ann Clarize GalangDokument6 SeitenThis Study Resource Was: Joyce Ann Clarize GalangYamna HasanNoch keine Bewertungen

- BKSL Ar2020Dokument250 SeitenBKSL Ar2020ᴅᴡɴᴋᴍɴʀʏNoch keine Bewertungen

- Loris ResumeDokument3 SeitenLoris Resumeapi-219457720Noch keine Bewertungen

- Solution Manual For Introduction To Finance Markets Investments and Financial Management 16th EditionDokument18 SeitenSolution Manual For Introduction To Finance Markets Investments and Financial Management 16th EditionDawn Steward100% (40)

- Start Up Latin America 2016Dokument144 SeitenStart Up Latin America 2016DAVE1778Noch keine Bewertungen

- West Teleservice: Case QuestionsDokument1 SeiteWest Teleservice: Case QuestionsAlejandro García AcostaNoch keine Bewertungen

- Performance Health CheckDokument2 SeitenPerformance Health CheckRavi Theja SolletiNoch keine Bewertungen

- JPMorgan - M&A BibleDokument146 SeitenJPMorgan - M&A BibleXie Zheyuan100% (2)

- Director VP Marketing in Boston MA Resume Jeffrey LawsonDokument2 SeitenDirector VP Marketing in Boston MA Resume Jeffrey LawsonJeffreyLawsonNoch keine Bewertungen

- The Relationship Between Corporate Social Responsibility and Financial Performance of Listed Isurance Firms in KenyaDokument3 SeitenThe Relationship Between Corporate Social Responsibility and Financial Performance of Listed Isurance Firms in Kenyajohn MandagoNoch keine Bewertungen

- Business Analytics - Science of Data Driven Decision Making (Live Online Programme)Dokument3 SeitenBusiness Analytics - Science of Data Driven Decision Making (Live Online Programme)KRITIKA NIGAMNoch keine Bewertungen

- 10.4324 9781315796789 PreviewpdfDokument124 Seiten10.4324 9781315796789 Previewpdftranminhquan08102003Noch keine Bewertungen

- Help FileDokument92 SeitenHelp FileAnirudh NarlaNoch keine Bewertungen

- Angel OneDokument139 SeitenAngel OneReTHINK INDIANoch keine Bewertungen

- ThesisDokument104 SeitenThesisJerry B CruzNoch keine Bewertungen