Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Black Book Stock Market in MumbaiDokument60 SeitenBlack Book Stock Market in MumbaiAnand YadavNoch keine Bewertungen

- FEDEX - Stock & Performance Analysis: Group MembersDokument15 SeitenFEDEX - Stock & Performance Analysis: Group MembersWebCutPasteNoch keine Bewertungen

- De La Salle Araneta UniversityDokument7 SeitenDe La Salle Araneta UniversityBryent GawNoch keine Bewertungen

- Accounts Question Paper 2022Dokument12 SeitenAccounts Question Paper 2022chgokulsinghNoch keine Bewertungen

- A Study On Investors Perception Towards Initial Public Offering in MumbaiDokument13 SeitenA Study On Investors Perception Towards Initial Public Offering in MumbaiRushabh JariwalaNoch keine Bewertungen

- Technical Analysis FundamentalsDokument15 SeitenTechnical Analysis FundamentalsAbuzafar AbdullahNoch keine Bewertungen

- Annual Report 2014 enDokument310 SeitenAnnual Report 2014 enMohammad AldehneeNoch keine Bewertungen

- Depreciation Expense Cost - Salvage Value / Useful LifeDokument2 SeitenDepreciation Expense Cost - Salvage Value / Useful LifeGarp BarrocaNoch keine Bewertungen

- Suspension Balance SheetDokument2 SeitenSuspension Balance SheetNadia Syamira SaaidiNoch keine Bewertungen

- Chapter 16Dokument2 SeitenChapter 16Faizan Ch100% (1)

- ACCA F9 Notes by Seah Chooi KhengDokument75 SeitenACCA F9 Notes by Seah Chooi KhengHuzaifa Ahmed100% (2)

- Investment Banking Strategies and Key Issues: Kaan Sarıaydın 23 November 2009, Bilgi UniversityDokument57 SeitenInvestment Banking Strategies and Key Issues: Kaan Sarıaydın 23 November 2009, Bilgi UniversityAshish SharmaNoch keine Bewertungen

- FM Chapter 2 - Study TextDokument14 SeitenFM Chapter 2 - Study Textirmaya.safitraNoch keine Bewertungen

- For December 31 20x1 The Balance Sheet of Baxter Corporation Was As FollowsDokument4 SeitenFor December 31 20x1 The Balance Sheet of Baxter Corporation Was As Followslaale dijaanNoch keine Bewertungen

- MAS-Reviewer 1Dokument13 SeitenMAS-Reviewer 1Raven BermalNoch keine Bewertungen

- BCG Global Asset Management 2023 May 2023Dokument28 SeitenBCG Global Asset Management 2023 May 2023VickoNoch keine Bewertungen

- True or FalseDokument8 SeitenTrue or FalseKim OlimbaNoch keine Bewertungen

- CASHDokument6 SeitenCASHCyril DE LA VEGANoch keine Bewertungen

- Chapter 7 - Cash Flow AnalysisDokument18 SeitenChapter 7 - Cash Flow AnalysisulfaNoch keine Bewertungen

- ABC Analysis - Method of Inventory Control and ManagementDokument12 SeitenABC Analysis - Method of Inventory Control and Managementdevesh rathNoch keine Bewertungen

- MTN FinancialsDokument200 SeitenMTN FinancialsIshaan SharmaNoch keine Bewertungen

- Vanguard FTSE Canada All Cap Index ETF VCN: December 31, 2019Dokument2 SeitenVanguard FTSE Canada All Cap Index ETF VCN: December 31, 2019ChrisNoch keine Bewertungen

- Cost of Capital Lecture Slides in PDF FormatDokument18 SeitenCost of Capital Lecture Slides in PDF FormatLucy UnNoch keine Bewertungen

- IFRS 2 Share Based PaymentsDokument14 SeitenIFRS 2 Share Based Paymentsjaydeep joshiNoch keine Bewertungen

- Credit Default Swaps and Their Application: DR Ewelina Sokołowska, DR Justyna Łapi SkaDokument7 SeitenCredit Default Swaps and Their Application: DR Ewelina Sokołowska, DR Justyna Łapi SkaSimon AltkornNoch keine Bewertungen

- Exercises On Bond Portfolio StrategiesDokument7 SeitenExercises On Bond Portfolio Strategiesmuzi jiNoch keine Bewertungen

- Introduction-to-Acctg 1 2Dokument27 SeitenIntroduction-to-Acctg 1 2Aenna Carmille TangubNoch keine Bewertungen

- Internal Rate of Return (IRR) CalculationDokument7 SeitenInternal Rate of Return (IRR) Calculationiram juttNoch keine Bewertungen

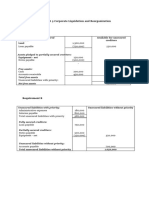

- CHAPTER 5 Corporate Liquidation and Reorganization Problem 5 Requirement ADokument6 SeitenCHAPTER 5 Corporate Liquidation and Reorganization Problem 5 Requirement AArtisanNoch keine Bewertungen

- Initiating Coverage on Divi's Laboratories with a Buy RatingDokument7 SeitenInitiating Coverage on Divi's Laboratories with a Buy Ratingvigneshnv77Noch keine Bewertungen